Is Up 7.4% After Deutsche Bank Resumes Coverage With Positive Rating")

In early 2026, Deutsche Bank resumed coverage of retail stocks and issued a positive rating on Ulta Beauty, citing solid top-line momentum, improved consumer conditions, and easing policy headwinds as key supports for the sector. This renewed endorsement underscores how Ulta Beauty is being grouped with retailers seen as relatively resilient, particularly where pricing and margin conditions appear more favorable. We’ll now examine how Deutsche Bank’s constructive stance on Ulta Beauty and the broader retail sector may influence the company’s investment narrative.

Find companies with promising cash flow potential yet trading below their fair value.

Ulta Beauty Investment Narrative Recap

For Ulta Beauty, the core belief is that beauty spending and loyalty driven retail can support earnings even as competition and costs rise. Deutsche Bank’s positive stance on retail reinforces confidence in Ulta’s near term demand backdrop, but it does not materially change the key near term catalyst of wellness and assortment expansion or the biggest risk around rising operating costs and store economics as consumer behavior shifts online.

The most relevant recent development here is Ulta’s raised full year 2025 guidance to around US$12.3 billion in net sales, which the market has treated as a sign of resilience and execution. That update sits squarely against Deutsche Bank’s constructive view on the sector and ties back to the main catalysts investors are watching, including assortment expansion, loyalty driven repeat spend, and the ability of higher sales to offset growing cost pressures.

Yet behind the upbeat sentiment, investors still need to watch how rising store and wage costs could affect…

Read the full narrative on Ulta Beauty (it’s free!)

Ulta Beauty’s narrative projects $13.8 billion revenue and $1.3 billion earnings by 2028. This requires 5.9% yearly revenue growth and an earnings increase of about $0.1 billion from $1.2 billion today.

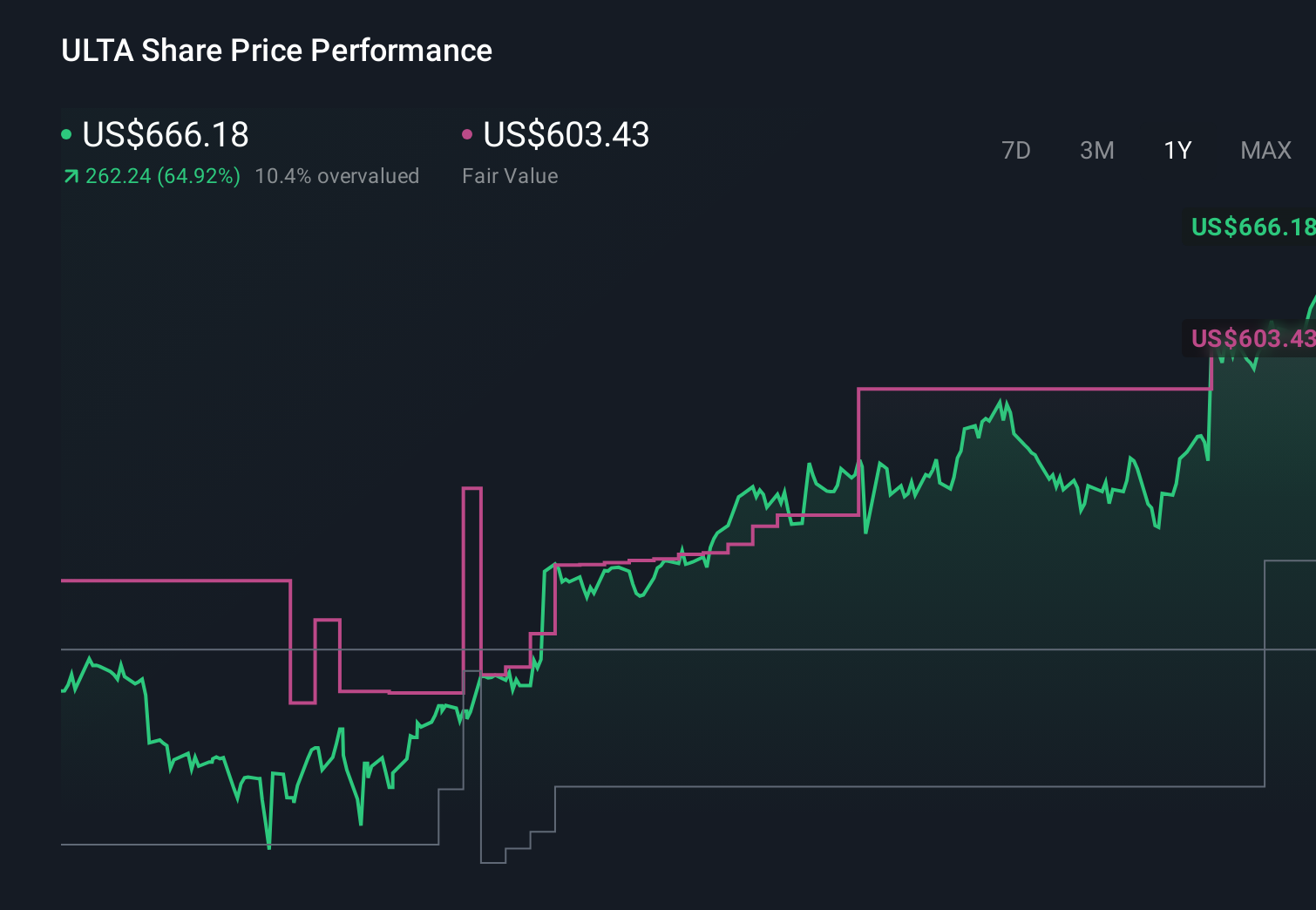

Uncover how Ulta Beauty’s forecasts yield a $603.43 fair value, a 9% downside to its current price.

Exploring Other Perspectives ULTA 1-Year Stock Price Chart

ULTA 1-Year Stock Price Chart

Nine fair value estimates from the Simply Wall St Community span roughly US$380 to US$603 per share, showing how far apart individual views can be. Set against that spread, Ulta’s higher 2025 sales guidance and Deutsche Bank’s constructive sector view both raise questions about how much top line resilience can offset long term cost and competitive pressures, so it is worth weighing several perspectives before forming your own view.

Explore 9 other fair value estimates on Ulta Beauty – why the stock might be worth 43% less than the current price!

Build Your Own Ulta Beauty Narrative

Disagree with existing narratives? Create your own in under 3 minutes – extraordinary investment returns rarely come from following the herd.

A great starting point for your Ulta Beauty research is our analysis highlighting 1 key reward that could impact your investment decision.Our free Ulta Beauty research report provides a comprehensive fundamental analysis summarized in a single visual – the Snowflake – making it easy to evaluate Ulta Beauty’s overall financial health at a glance.Seeking Other Investments?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com