Shareholders Look For Exit As Shares Take 33% Pounding")

The Beauty Skin Corp. (KOSDAQ:406820) share price has softened a substantial 33% over the previous 30 days, handing back much of the gains the stock has made lately. Longer-term shareholders will rue the drop in the share price, since it’s now virtually flat for the year after a promising few quarters.

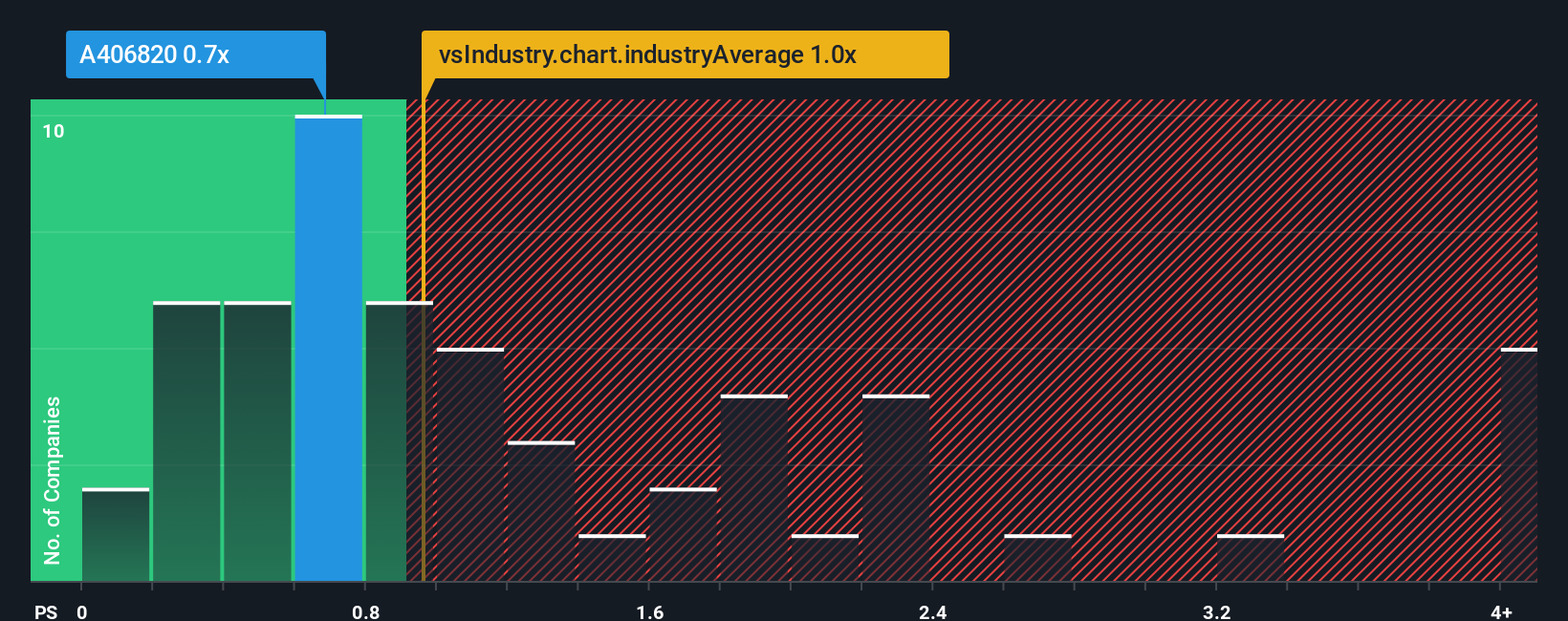

Even after such a large drop in price, there still wouldn’t be many who think Beauty Skin’s price-to-sales (or “P/S”) ratio of 0.7x is worth a mention when the median P/S in Korea’s Personal Products industry is similar at about 1x. However, investors might be overlooking a clear opportunity or potential setback if there is no rational basis for the P/S.

Check out our latest analysis for Beauty Skin

KOSDAQ:A406820 Price to Sales Ratio vs Industry January 30th 2026 How Has Beauty Skin Performed Recently?

KOSDAQ:A406820 Price to Sales Ratio vs Industry January 30th 2026 How Has Beauty Skin Performed Recently?

As an illustration, revenue has deteriorated at Beauty Skin over the last year, which is not ideal at all. Perhaps investors believe the recent revenue performance is enough to keep in line with the industry, which is keeping the P/S from dropping off. If not, then existing shareholders may be a little nervous about the viability of the share price.

Want the full picture on earnings, revenue and cash flow for the company? Then our free report on Beauty Skin will help you shine a light on its historical performance. How Is Beauty Skin’s Revenue Growth Trending?

Beauty Skin’s P/S ratio would be typical for a company that’s only expected to deliver moderate growth, and importantly, perform in line with the industry.

Retrospectively, the last year delivered a frustrating 31% decrease to the company’s top line. Unfortunately, that’s brought it right back to where it started three years ago with revenue growth being virtually non-existent overall during that time. Accordingly, shareholders probably wouldn’t have been overly satisfied with the unstable medium-term growth rates.

Comparing the recent medium-term revenue trends against the industry’s one-year growth forecast of 23% shows it’s noticeably less attractive.

With this information, we find it interesting that Beauty Skin is trading at a fairly similar P/S compared to the industry. Apparently many investors in the company are less bearish than recent times would indicate and aren’t willing to let go of their stock right now. Maintaining these prices will be difficult to achieve as a continuation of recent revenue trends is likely to weigh down the shares eventually.

The Bottom Line On Beauty Skin’s P/S

Beauty Skin’s plummeting stock price has brought its P/S back to a similar region as the rest of the industry. Using the price-to-sales ratio alone to determine if you should sell your stock isn’t sensible, however it can be a practical guide to the company’s future prospects.

We’ve established that Beauty Skin’s average P/S is a bit surprising since its recent three-year growth is lower than the wider industry forecast. When we see weak revenue with slower than industry growth, we suspect the share price is at risk of declining, bringing the P/S back in line with expectations. Unless the recent medium-term conditions improve, it’s hard to accept the current share price as fair value.

And what about other risks? Every company has them, and we’ve spotted 3 warning signs for Beauty Skin (of which 2 are a bit concerning!) you should know about.

If companies with solid past earnings growth is up your alley, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

Valuation is complex, but we’re here to simplify it.

Discover if Beauty Skin might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.