Valuation Check As Mexico Expansion With Impulso Gym Targets Underpenetrated Markets")

Planet Fitness (PLNT) has put its Mexico expansion back in focus after signing a new franchise agreement with Impulso Gym to open clubs in Tijuana and Mexicali, targeting regions with relatively low gym membership penetration.

See our latest analysis for Planet Fitness.

Planet Fitness shares trade at US$90.65, with recent Mexico expansion news and a new independent director arriving after a period of weaker momentum. This includes a 30 day share price return decline of 4.04% and a 1 year total shareholder return loss of 6.44%. However, 3 and 5 year total shareholder returns of 12.47% and 5.30% present a more mixed longer term picture.

If this gym expansion story has you thinking about where growth might come from next, it could be worth scanning 22 top founder-led companies as a fresh source of ideas.

With Planet Fitness trading at US$90.65, annual revenue of US$1.2b and net income of about US$205.8m, plus a modest 4.46% intrinsic discount, you have to ask: is there real upside left here, or is the market already pricing in future growth?

Most Popular Narrative: 30.3% Undervalued

With Planet Fitness last closing at $90.65 against a widely followed fair value view of about $130, the current Mexico headlines sit inside a much bigger growth and margin story.

Ongoing format optimization, with more strength equipment, redesigned layouts, and attention to user preference, is increasing club utilization and member satisfaction, which should improve retention and provide opportunities for pricing power, positively impacting both revenue and net margins.

Curious what kind of revenue climb and margin profile need to line up to reach that fair value? The most followed narrative leans on specific growth, profitability and future P/E assumptions that go well beyond a simple gym expansion story. The details behind those moving parts might change how you see that $130 figure.

Result: Fair Value of $130 (UNDERVALUED)

Have a read of the narrative in full and understand what’s behind the forecasts.

However, you also need to factor in risks such as higher member churn from easier online cancellations and the possibility that expansion puts pressure on franchisee economics.

Find out about the key risks to this Planet Fitness narrative.

Another Way To Look At Valuation

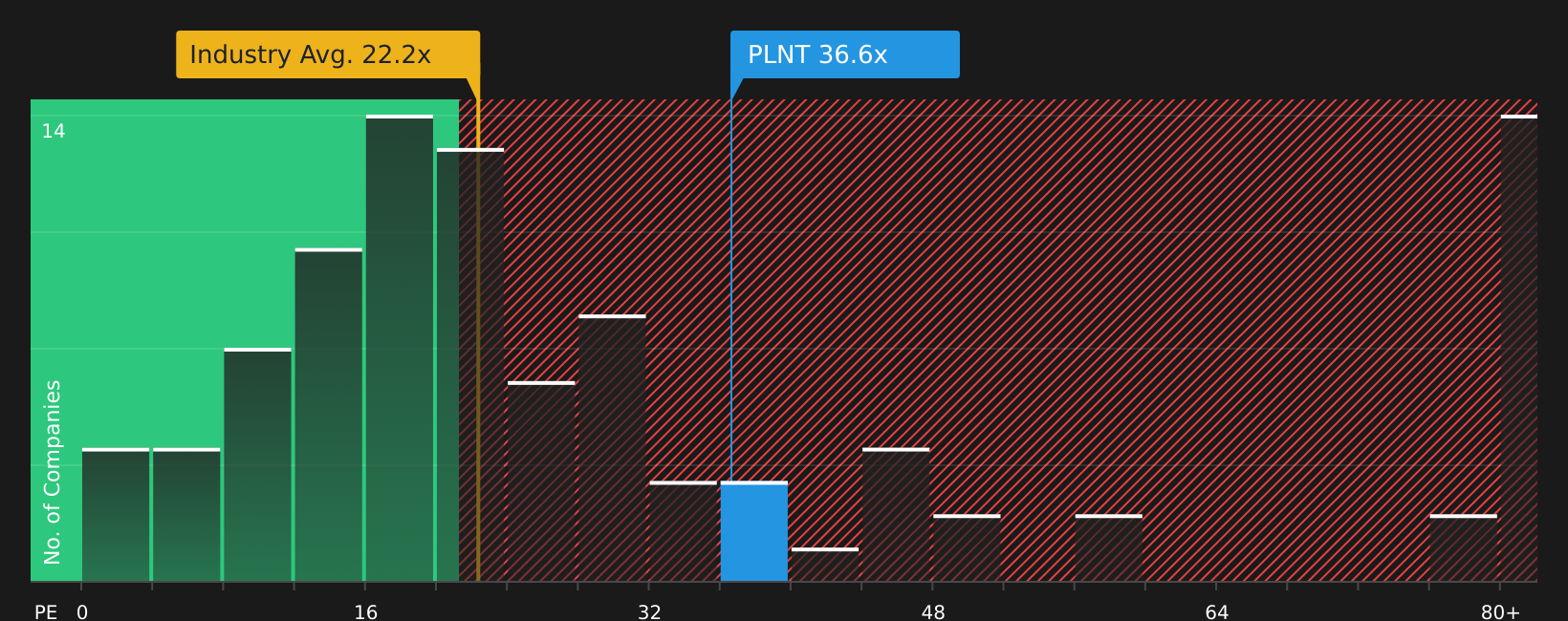

The earlier fair value of $130 leans on growth and margin forecasts, but the current P/E of 36.6x tells a different story. That is well above the US Hospitality average of 22.2x, the peer average of 16.5x, and even the 23.9x fair ratio that the market could drift toward over time. If sentiment cools, does that premium multiple leave less room for error than the discounted cash flow suggests?

See what the numbers say about this price — find out in our valuation breakdown.

NYSE:PLNT P/E Ratio as at Feb 2026Next Steps

NYSE:PLNT P/E Ratio as at Feb 2026Next Steps

If this feels like a mix of upside potential and real questions, consider moving from reading to testing the numbers yourself by checking 4 key rewards and 2 important warning signs.

Looking for more investment ideas?

If this story has sharpened your thinking, do not stop here, there are plenty of other businesses worth putting through the same kind of scrutiny.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We’ve created the ultimate portfolio companion for stock investors, and it’s free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

")