Make better investment decisions with Simply Wall St’s easy, visual tools that give you a competitive edge.

Danone (ENXTPA:BN) is dealing with a one off impact from an infant formula recall that is expected to affect its first quarter 2026 sales.

The CEO has reiterated confidence in product safety and indicated that operations in the affected regions are expected to normalize by March.

Danone, known for dairy, plant based products, waters and specialized nutrition, is drawing extra attention to its infant formula segment as the recall works through the system. Infant nutrition can be a sensitive category for consumers and regulators, so any disruption in this part of the portfolio tends to attract close scrutiny. For investors, the focus is on how contained the issue remains and how customer relationships respond over time.

Management guidance that the impact is one off and that conditions could normalize by March provides a rough time frame for when the immediate disruption might ease. As more detail emerges around the operational hit in early 2026, you can watch for updates on volumes in affected regions, brand perception and any shifts in how Danone allocates resources across its product lines.

Stay updated on the most important news stories for Danone by adding it to your watchlist or portfolio. Alternatively, explore our Community to discover new perspectives on Danone.

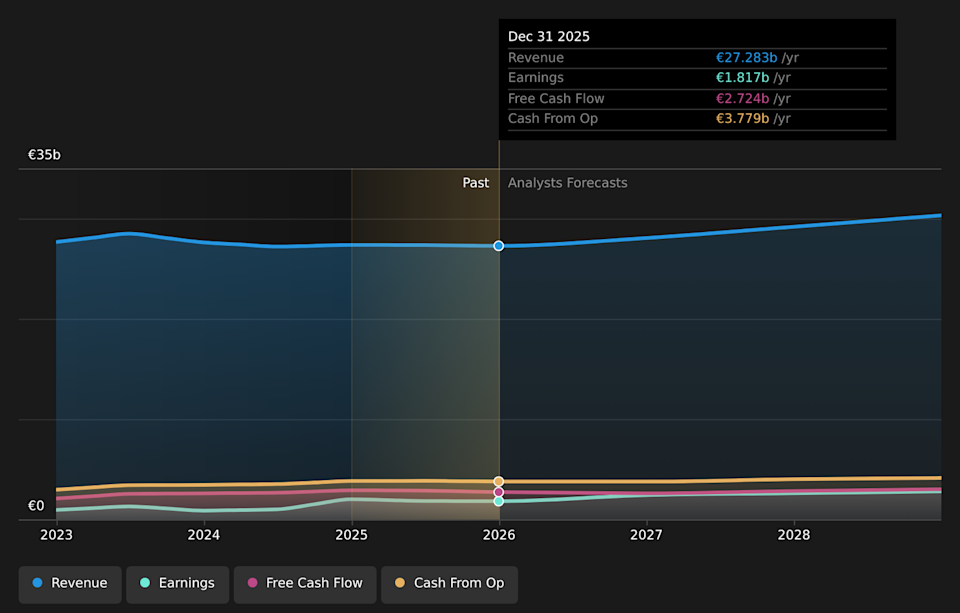

ENXTPA:BN Earnings & Revenue Growth as at Feb 2026

ENXTPA:BN Earnings & Revenue Growth as at Feb 2026

We’ve flagged 2 risks for Danone. See which could impact your investment.

The recall comes just after Danone reported 2025 sales of €27.283b and net income of €1.825b, with earnings per share from continuing operations of €2.82. Management is framing the infant-formula withdrawal as a one off event, with an estimated 0.5% to 1% impact on net sales in the first quarter of 2026 and an expectation that affected regions should normalize by March. For you, the key question is whether this disruption stays ring fenced or spills over into longer term brand trust and shelf space in infant nutrition, a category where players like Nestlé and Reckitt also compete heavily.

The recall response and CEO emphasis on product safety sit alongside Danone’s focus on health driven products and specialized nutrition, which the narrative highlights as central to its position in premium nutrition categories.

At the same time, any operational hiccup in infant formula could challenge the narrative’s assumption of smoother execution in high value nutrition segments, especially if regulators or retailers become more cautious.

The specific short term sales impact of 0.5% to 1% in early 2026, and the operational work needed to maintain trust with healthcare channels, are not directly reflected in the broader narrative around portfolio mix and channel expansion.

Knowing what a company is worth starts with understanding its story. Check out one of the top narratives in the Simply Wall St Community for Danone to help decide what it’s worth to you.

⚠️ Execution risk around recalls and quality assurances in sensitive categories like infant nutrition, where any misstep can affect brand perception and regulator confidence.

⚠️ Earnings already reflect pressure, with 2025 net income and EPS from continuing operations lower than the prior year, so additional one off items can complicate your read on underlying performance.

🎁 Management signals that the recall impact is one off and expects conditions to normalize by March. If that happens, ongoing disruption to sales and operations would likely be more limited.

🎁 Danone’s guidance for 2026 points to like for like sales growth between 3% and 5% with recurring operating income growing faster than sales, and the Board plans to propose a 4.7% higher dividend of €2.25 per share for 2025.

From here, you may want to track how first quarter 2026 results line up with the estimated 0.5% to 1% sales impact, and whether management reiterates that the issue has been contained. Watch commentary on infant nutrition volumes in Europe and the Middle East versus unaffected regions like China, plus any references to healthcare professional feedback or shelf positioning against rivals such as Nestlé and Reckitt. It is also worth following how firmly Danone maintains its 2026 guidance and dividend proposal in light of the recall, as that will give you a sense of how confident management is in the broader portfolio and Renew program.

To ensure you’re always in the loop on how the latest news impacts the investment narrative for Danone, head to the community page for Danone to never miss an update on the top community narratives.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include BN.PA.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com