Jamieson Wellness (TSX:JWEL) closed out FY 2025 with Q4 revenue of $277.7 million and basic EPS of $0.88, underpinned by trailing twelve month revenue of $822.1 million and basic EPS of $1.49. Over recent periods the company has seen quarterly revenue move from $176.2 million in Q3 2024 to $244.8 million in Q4 2024 and then to $277.7 million in Q4 2025. Quarterly basic EPS shifted from $0.25 in Q3 2024 to $0.88 in Q4 2024 and $0.88 again in Q4 2025. These figures sit against a backdrop of a 7.6% net profit margin and earnings growth of 20.3% over the past year, which highlight profitability trends that are front and center for investors.

See our full analysis for Jamieson Wellness.

With the latest revenue, EPS and margin numbers on the table, the next step is to see how these results line up with the prevailing stories about Jamieson Wellness, where some popular narratives may be reinforced while others are put to the test.

Curious how numbers become stories that shape markets? Explore Community Narratives

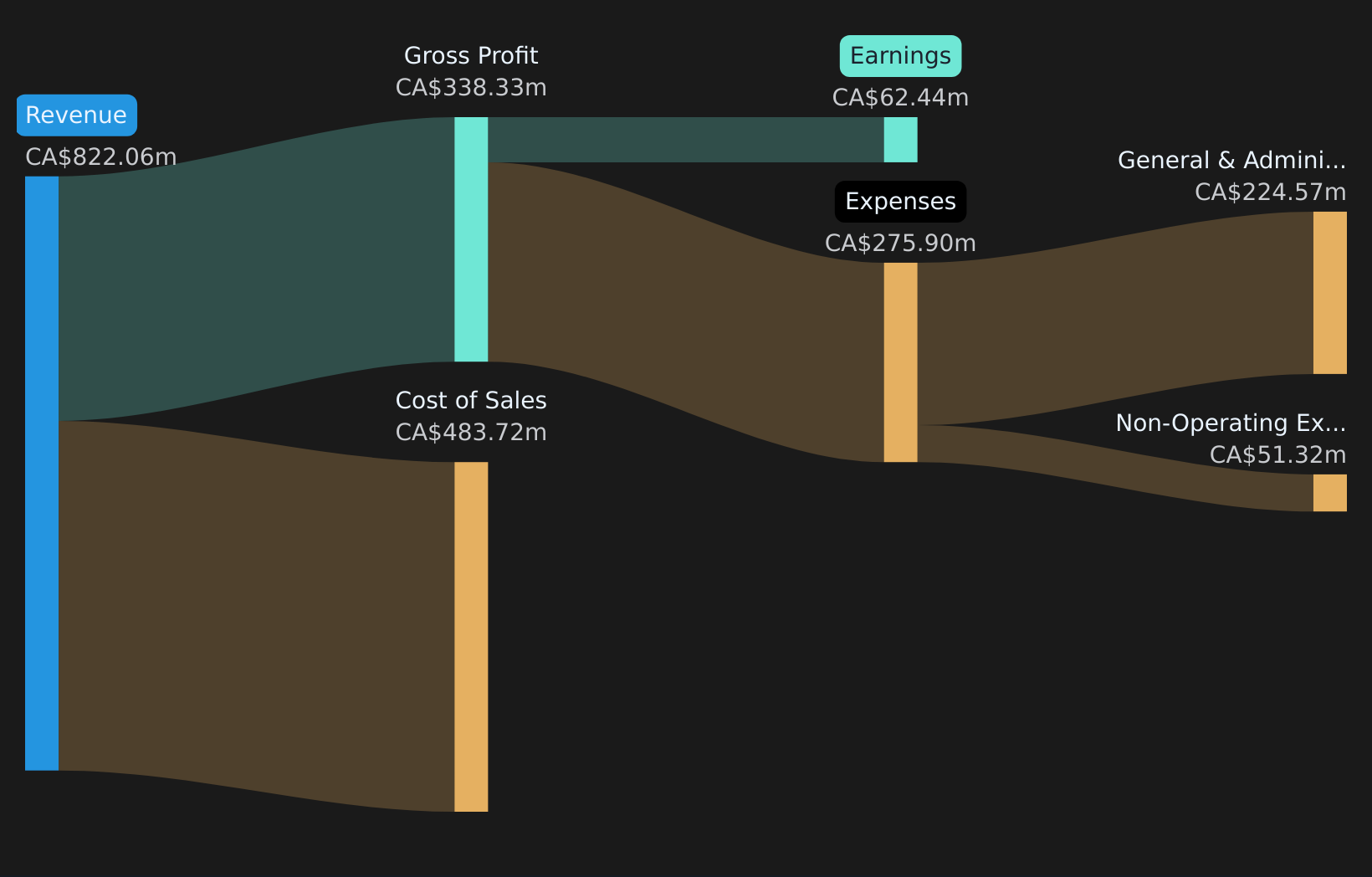

TSX:JWEL Revenue & Expenses Breakdown as at Feb 2026 20.3% earnings growth and 7.6% margin put profitability in focus Over the last 12 months, Jamieson Wellness earned CA$62.4 million of net income on CA$822.1 million of revenue, which works out to 20.3% earnings growth and a 7.6% net profit margin compared with 7.1% a year earlier. What stands out for the bullish view is that this 20.3% earnings growth is paired with that 7.6% margin. However, bulls looking for a long term “branded wellness compounder” still have to weigh that the company’s longer term earnings growth is 3.7% per year over five years, which is slower than the latest 12 month pace. P/E of 24.9x versus peers and a CA$90.19 DCF fair value The shares trade on a 24.9x P/E at a price of CA$37.71, above the 21.8x Global Personal Products industry and the 17.2x peer average, while the provided DCF fair value is CA$90.19, which is stated as around 58% above the current share price. Critics highlight the higher P/E multiple as a bearish point, yet the data also shows earnings up 20.3% over the past year and revenue forecast to grow about 8.5% per year, which creates a tension between:

TSX:JWEL Revenue & Expenses Breakdown as at Feb 2026 20.3% earnings growth and 7.6% margin put profitability in focus Over the last 12 months, Jamieson Wellness earned CA$62.4 million of net income on CA$822.1 million of revenue, which works out to 20.3% earnings growth and a 7.6% net profit margin compared with 7.1% a year earlier. What stands out for the bullish view is that this 20.3% earnings growth is paired with that 7.6% margin. However, bulls looking for a long term “branded wellness compounder” still have to weigh that the company’s longer term earnings growth is 3.7% per year over five years, which is slower than the latest 12 month pace. P/E of 24.9x versus peers and a CA$90.19 DCF fair value The shares trade on a 24.9x P/E at a price of CA$37.71, above the 21.8x Global Personal Products industry and the 17.2x peer average, while the provided DCF fair value is CA$90.19, which is stated as around 58% above the current share price. Critics highlight the higher P/E multiple as a bearish point, yet the data also shows earnings up 20.3% over the past year and revenue forecast to grow about 8.5% per year, which creates a tension between:

a bearish lens that sees 24.9x P/E as expensive versus the 17.2x peer average, and a value focused lens that points to the CA$90.19 DCF fair value and compares it to the CA$37.71 share price alongside improved net margin at 7.6%. Stay curious about how valuation, growth, and risk fit together here, and see what the wider community is saying in one place. Curious how numbers become stories that shape markets? Explore Community Narratives Debt coverage risk set against revenue forecast of about 8.5% a year The risk summary flags that debt is not well covered by operating cash flow, at the same time as the data shows revenue forecast to grow about 8.5% per year and trailing net income at CA$62.4 million on CA$822.1 million of revenue. Bears argue that limited operating cash flow coverage of debt is a key financial pressure, and this concern sits alongside the growth profile, where:

forecast revenue growth of about 8.5% per year and a 7.6% net margin frame the ability to service obligations from future operations, while the debt coverage flag reminds you that current cash generation versus debt is tight enough to be highlighted as a major risk in the data provided. Next Steps

Don’t just look at this quarter; the real story is in the long-term trend. We’ve done an in-depth analysis on Jamieson Wellness’s growth and its valuation to see if today’s price is a bargain. Add the company to your watchlist or portfolio now so you don’t miss the next big move.

Seeing both risks and rewards in this story, it makes sense to check the numbers for yourself and move quickly to your own view. To round that out, you may want to look at 3 key rewards and 1 important warning sign.

See What Else Is Out There

Jamieson Wellness pairs a 7.6% net margin with earnings growth of 20.3%, yet its higher 24.9x P/E and debt coverage risk may concern you.

If that mix of a rich earnings multiple and flagged debt coverage risk makes you cautious, take a look at 8 resilient stocks with low risk scores to quickly focus on companies with more resilient profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We’ve created the ultimate portfolio companion for stock investors, and it’s free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com