Valuation After 2025 Beat And Cautious 2026 Outlook")

Planet Fitness (PLNT) is back in focus after its fourth quarter and full year 2025 results, where higher revenue and net income met a cautious 2026 outlook and triggered a sharp shift in investor sentiment.

See our latest analysis for Planet Fitness.

That cautious 2026 outlook and the legal overhang have weighed on sentiment, with a 1 day share price return decline of 1.93% and a 90 day share price return decline of 24.48%. Meanwhile, the 3 year total shareholder return is roughly flat, suggesting recent momentum has faded despite longer term value holding up better.

If Planet Fitness’s recent drop has you reassessing your watchlist, this could be a good time to widen the lens and check out 19 top founder-led companies.

With revenue and earnings moving higher but the share price sliding and the stock trading below some analyst targets, investors may wonder whether Planet Fitness is now undervalued or whether the market is already pricing in its future growth.

Most Popular Narrative: 36.8% Undervalued

Planet Fitness’s most followed narrative pegs fair value around $130, well above the last close at $82.15, which frames a wide valuation gap for investors to weigh.

Analysts are assuming Planet Fitness’s revenue will grow by 11.6% annually over the next 3 years.

Analysts assume that profit margins will increase from 16.2% today to 19.3% in 3 years time.

Want to see what sits behind that optimism on revenue growth and margin expansion? The narrative leans on rising earnings, expanding membership, and a premium future P/E that assumes investors keep paying up for the model.

At the core of this widely followed view is a detailed earnings path, supported by specific assumptions on revenue growth, margin improvement and the valuation multiple applied to those future profits.

Result: Fair Value of $130 (UNDERVALUED)

Have a read of the narrative in full and understand what’s behind the forecasts.

However, the click to cancel rollout and heavier reliance on opening new clubs could pressure membership growth and margins if churn or franchise appetite weakens.

Find out about the key risks to this Planet Fitness narrative.

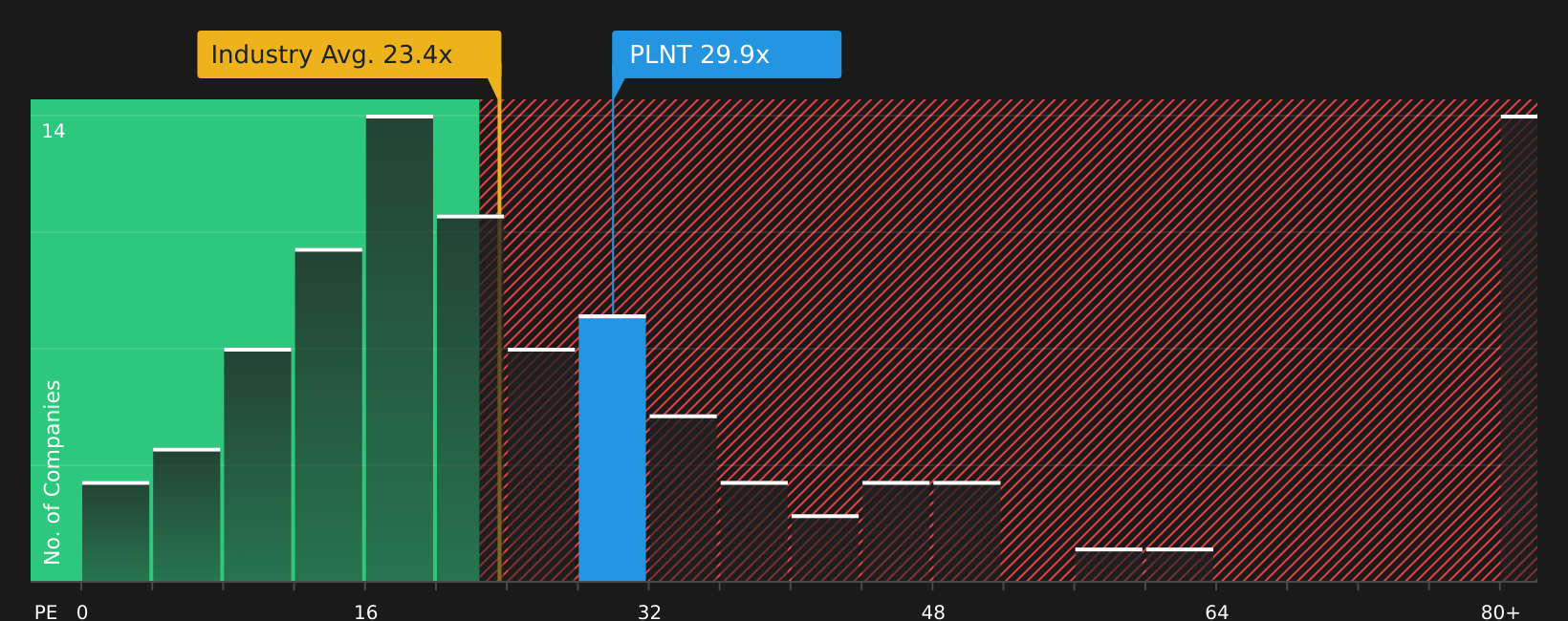

Another View: Rich P/E Puts The Brakes On

Those fair value models present Planet Fitness as undervalued, but the current P/E of 29.9x tells a tighter story. It stands above the US Hospitality industry at 23.4x, the peer average at 21.2x, and even the 24.3x fair ratio. That premium could limit upside if sentiment stays cautious.

See what the numbers say about this price — find out in our valuation breakdown.

NYSE:PLNT P/E Ratio as at Mar 2026Next Steps

NYSE:PLNT P/E Ratio as at Mar 2026Next Steps

With sentiment clearly split, do you want to rely on others or test the story yourself and move quickly while the market debates it? Our data already highlights 3 key rewards and 2 important warning signs so you can weigh the concerns against the potential upsides for yourself.

Looking for more investment ideas?

If Planet Fitness has sharpened your thinking, do not stop there. Use the Simply Wall St screener to uncover other ideas that match your style before markets move on.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We’ve created the ultimate portfolio companion for stock investors, and it’s free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com