Narrative Is Shifting As Analysts Reset Expectations")

Get insights on thousands of stocks from the global community of over 7 million individual investors at Simply Wall St.

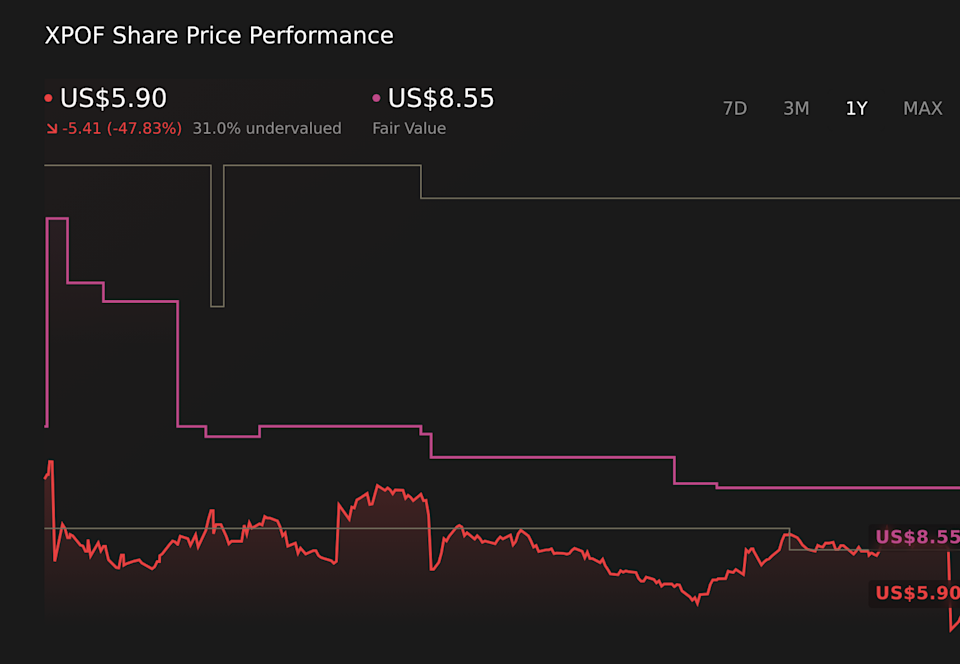

The analyst fair value estimate for Xponential Fitness has shifted from US$10.90 to US$8.55, signaling a reassessment of what the business might be worth today. That change aligns with recent research in which several firms trimmed price targets and adopted a more cautious tone after Q4 results and 2026 guidance. As you read on, you will see how bullish and bearish views are evolving and how you can track this narrative over time.

Stay updated as the Fair Value for Xponential Fitness shifts by adding it to your watchlist or portfolio. Alternatively, explore our Community to discover new perspectives on Xponential Fitness.

Guggenheim trimmed its price target to US$10 from US$12 but kept a Buy rating, pointing to what it sees as the intrinsic value of the Club Pilates brand as a key support for the equity story.

Lake Street reduced its target to US$9 from US$13 and maintained a Buy rating, indicating that sentiment could improve if Xponential Fitness can show even modest organic revenue growth in 2026.

Roth Capital moved to Neutral from Buy and cut its target to US$7 from US$10, citing weakening comps, poor free cash flow conversion, and significant balance sheet leverage, and seeing limited near term upside.

Stifel, Northland, and B. Riley each lowered price targets into a US$6 to US$7 range, with Hold, Market Perform, and Neutral ratings that reflect concerns around softer 2026 guidance and the ongoing reset plan.

Do your thoughts align with the Bull or Bear Analysts? Perhaps you think there’s more to the story. Head to the Simply Wall St Community to discover more perspectives!

NYSE:XPOF 1-Year Stock Price Chart

NYSE:XPOF 1-Year Stock Price Chart

We’ve flagged 2 risks for Xponential Fitness. See which could impact your investment.

Voss Capital issued an open letter on March 4, 2026, arguing that Xponential Fitness shares trade well below what it sees as underlying value and urging the board to hire independent financial advisors to explore options, including a potential full sale of the company overseen by independent directors.

In the same letter, Voss Capital said it believes the Club Pilates brand on its own is worth more than the current enterprise value and that a well run sale process with detailed franchise level data could attract buyers at prices above the current public market valuation for Xponential.

Xponential Fitness issued fiscal 2026 guidance calling for revenue of US$260.0 million to US$270.0 million, which the company described as a 16% decrease at the midpoint.

For the fourth quarter ended December 31, 2025, the company reported impairment of goodwill and other noncurrent assets of US$307,000, compared with US$45,957,000 in the same quarter a year earlier.

Story Continues

Fair value estimate moved from US$10.90 to US$8.55.

Revenue growth assumption shifted from 1.75% growth to a 1.52% decline.

Net profit margin expectation moved from 12.46% to 10.54%.

Future P/E multiple changed from 12.5x to 17.2x.

Discount rate in analyst models moved from 10.68% to 12.33%.

Narratives connect Xponential Fitness’s business story to analyst forecasts and fair value estimates, updating as new data, guidance, and news come through. They help you see how catalysts and risks fit together rather than looking at single headlines in isolation.

Head over to the Simply Wall St Community and follow the Narrative on Xponential Fitness to stay up to date on:

How investment in core brands such as Club Pilates, Pure Barre, YogaSix, and StretchLab, together with national marketing and digital tools, could influence unit volumes, member retention, and margins over time.

The role of international expansion, omni channel experiences, and the Fit Commerce retail partnership in shaping recurring royalty streams, overhead costs, and working capital.

Key risks around slower same store sales, delayed and closed franchise units, reduced brand diversity after divestitures, and higher leverage that may affect growth and financial flexibility.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include XPOF.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com