Valuation After Recent Share Price Pullback And Mixed Momentum")

What Ulta Beauty’s Recent Returns Say About the Stock Now

Ulta Beauty (ULTA) has seen mixed share performance recently, with a 0.8% gain over the past day, a 3.2% decline over the past week, and a 6.2% decline over the past month.

See our latest analysis for Ulta Beauty.

Looking past the recent pullback, Ulta Beauty’s 90 day share price return of 7.8% and strong 1 year total shareholder return of 88.9% suggest earlier momentum has cooled, while longer term holders remain well rewarded.

If Ulta’s run has you thinking about where growth could show up next, it may be worth scanning our list of 20 top founder-led companies as potential new ideas.

With Ulta shares around $647 and analysts’ average target near $699, while intrinsic value estimates sit higher again, the real question is whether you are looking at a genuine opportunity or a market that is already pricing in future growth.

Most Popular Narrative: 51.4% Overvalued

According to the most followed narrative, Ulta Beauty’s fair value sits at $427.41, well below the recent $647 share price, which sets up a clear valuation gap for investors to weigh.

Ulta, the other company I was thinking of cutting, has a surprisingly favorable relative valuation in the beauty retail space. It has decent margins and actually is able to direct decent amounts of buybacks. Beauty products in particular make a lot of sense to be sold alongside salon services in a storefront so you can actually suss out the high-end products in person. They have numerous private label brands and partnerships that attract customers, providing a small buffer to their expanding loyalty program. They are at their lowest ever P/E ratio right now at only 13, but with a high P/S and book ratio of 7, which is odd to me. They have a strong Return on Capital Employed (ROCE) and are free from debt. However, being a pure-play storefront with little room to grow aside from the untested waters of abroad leaves this company with a likely case of declining margins and earnings before only being able to grow modestly in the future. It is certainly a giant that can grow bigger, but the execution risk amid growing competition from e-commerce and other legacy storefronts in the US may take away their market share in areas that are already saturated with stores. Perceived undervaluation is mostly tangible under assumed multiple expansion, which doesn’t leave a whole lot of room for an edge. Morningstar has the following to say: “We believe it carries more products and brands in the major beauty categories of makeup, hair care, skin care, fragrance, bath, and accessories than any other US specialty beauty retailer. According to the National Retail Federation, Ulta and wide-moat LVMH’s Sephora are the only two specialty beauty retailers among America’s 100 largest retail companies. Although Ulta faces significant and increasing competition, we believe it has a unique market position and loyal customers. As evidence of its competitive edge, its adjusted return on invested capital, including goodwill, has consistently been above our 9% estimated weighted average cost of capital. We estimate Ulta”s adjusted ROIC, including goodwill ROIC, will average 27% over the next decade… We view Ulta”s ability to thrive in a very crowded marketplace as evidence of a competitive edge…We view Ulta”s strong margins as evidence of its competitive edge…We think Ulta”s salon services with 8,000 stylists provide a competitive advantage. The $60 billion (IBISWorld estimate) US hair salon industry is very fragmented, as national chains (such as those franchised by Regis) have less than 10% share…We believe Ulta has opportunities for store growth despite its large base. The chain has expanded rapidly, having added about 1,000 locations since the end of 2008. As Ulta now has stores in all 50 states and all major metropolitan areas, we believe its store openings will slow. Unlike some competitors (including Sephora), Ulta has no stores outside the US. The firm had planned to enter Canada in 2021, but this expansion was put on indefinite hold. Instead, Ulta”s first international expansion will be into Mexico through a partnership with Grupo Axo… Due to the ease of launching products online and marketing them through platforms like Instagram, it has never been easier to launch new beauty products. Many of them fail, but some of them have found success. Ulta has been proactive in seeking new brands and offering them in its stores…We estimate Ulta will achieve 4% compound average sales growth over the next 10 years, well below its 16% average annual sales growth over the past decade. We forecast 4% yearly same-store sales growth in the long term.”

Curious how a company with double digit margins, buybacks and high returns on capital still lands below $450 in this narrative? The fair value hinges on slower revenue expansion, steady profitability and a future earnings multiple that looks very different from today’s share price. The full narrative lays out the exact growth, margin and valuation swing that need to line up for that number to make sense.

Result: Fair Value of $427.41 (OVERVALUED)

Have a read of the narrative in full and understand what’s behind the forecasts.

However, this view could be challenged if Ulta’s 5.7% annual revenue growth and 5.2% net income growth persist, or if market sentiment shifts around its earnings multiple.

Find out about the key risks to this Ulta Beauty narrative.

Another Take Using Market Ratios

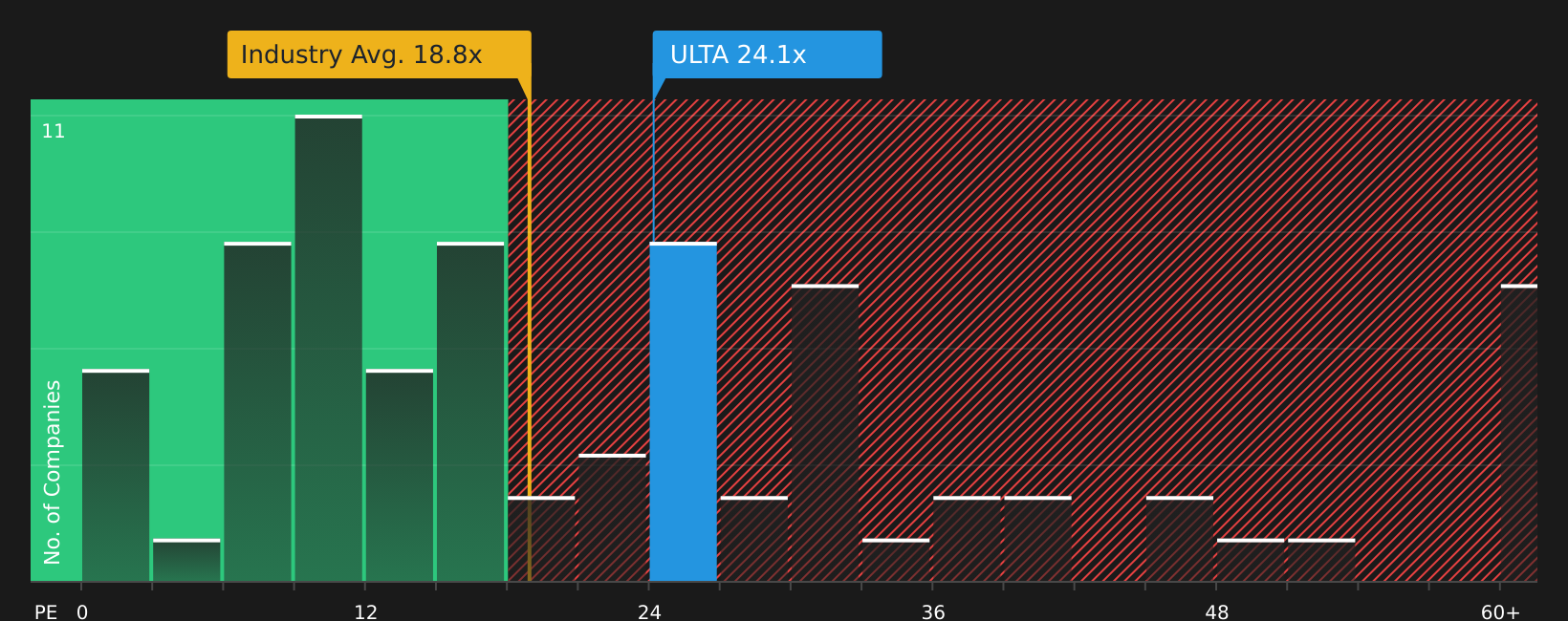

The narrative fair value of $427.41 paints Ulta as 51.4% overvalued, but current market ratios tell a more mixed story. At a 24.1x P/E, Ulta trades above the US Specialty Retail average of 19x, yet below its peer group average of 33.1x, so the premium is not one sided.

Our fair ratio of 18.1x sits well under today’s 24.1x, which implies the market is paying up for earnings relative to where that ratio could move. For you as an investor, the question is whether Ulta’s quality and track record justify paying above that fair ratio, or if patience makes more sense.

See what the numbers say about this price — find out in our valuation breakdown.

NasdaqGS:ULTA P/E Ratio as at Mar 2026Next Steps

NasdaqGS:ULTA P/E Ratio as at Mar 2026Next Steps

If the mixed signals here leave you on the fence, now is a good time to examine the underlying data yourself and stress test your assumptions. To see what the market is currently optimistic about, take a closer look at the 1 key reward.

Looking for more investment ideas?

If Ulta has sharpened your thinking, do not stop here. Broaden your watchlist with other carefully filtered opportunities before the next wave of ideas moves without you.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Spring Makeup Products to Shop")