Ulta Beauty (NasdaqGS:ULTA) has kicked off its annual 21 Days of Beauty sale event, one of its largest recurring promotions. The company is moving ahead with international expansion, including its first store in the UAE. Ulta recently entered the UK and Ireland by acquiring Space NK and is also pursuing growth in Mexico and the broader Middle East.

Ulta Beauty enters this phase of expansion with its shares at $652.65 and a 1 year return of 98.2%, alongside a 5 year return of 104.6%. The stock has been more mixed over shorter periods, with a 6.3% decline over the past 30 days and a 1.3% decline over the past week, while still up 5.3% year to date.

For investors, the combination of a large, recurring US sales event and international moves across Europe and the Middle East presents Ulta as a business balancing domestic engagement with overseas initiatives. The key question is how effectively Ulta can integrate Space NK, execute in new markets such as the UAE and Mexico, and maintain the appeal of campaigns such as 21 Days of Beauty at the same time.

Stay updated on the most important news stories for Ulta Beauty by adding it to your watchlist or portfolio. Alternatively, explore our Community to discover new perspectives on Ulta Beauty.

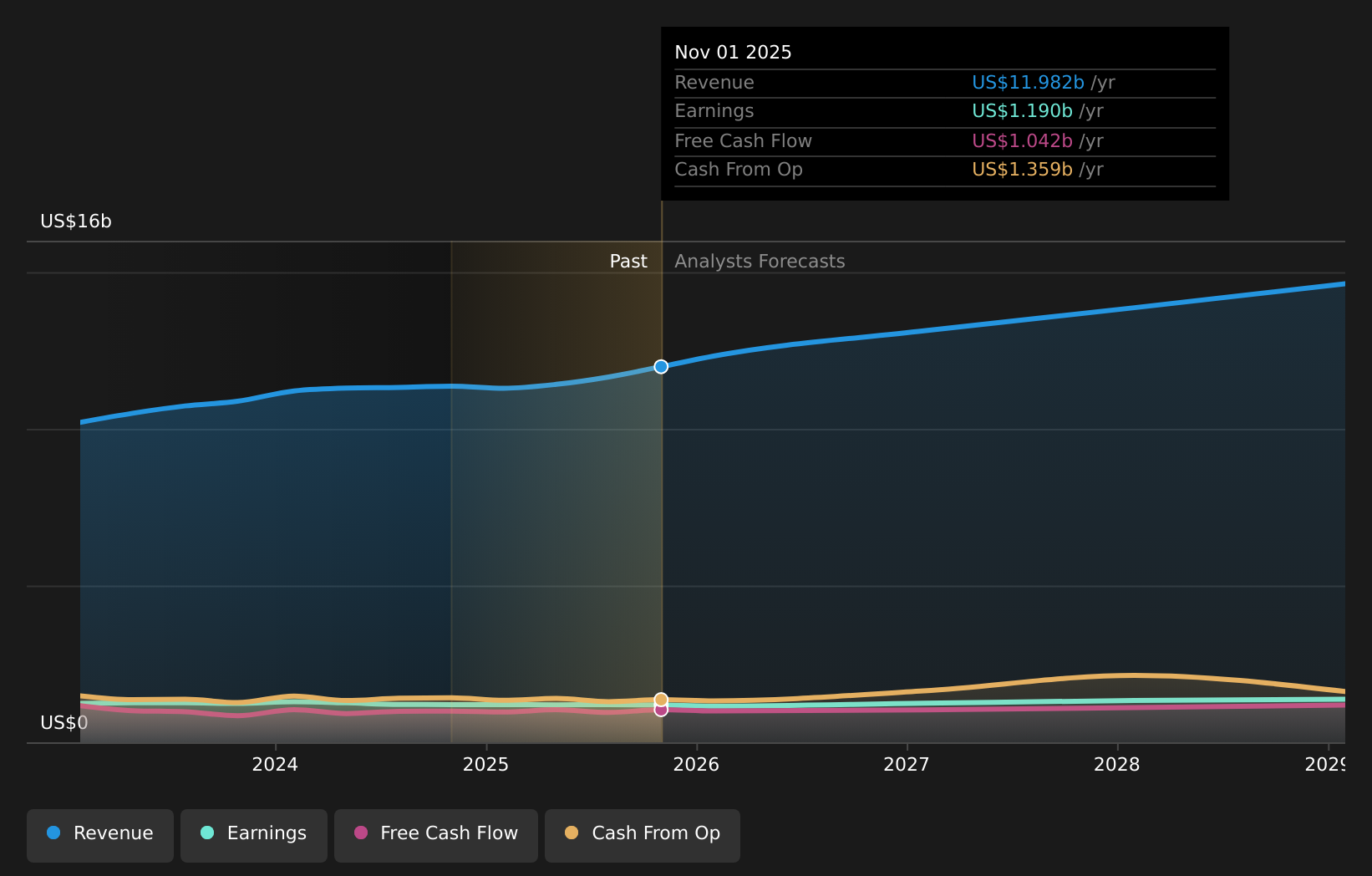

NasdaqGS:ULTA Earnings & Revenue Growth as at Mar 2026

NasdaqGS:ULTA Earnings & Revenue Growth as at Mar 2026

Ulta’s 21 Days of Beauty sale and push into the UK, Ireland, Mexico, and the Middle East sit at the intersection of near term traffic and longer term repositioning. The sale event concentrates promotions around prestige brands and loyalty perks, which can pull forward demand but also test how much discounting is needed to keep customers engaged as competition from Sephora, department stores, and direct to consumer brands stays intense. At the same time, the Space NK acquisition and first UAE store give Ulta access to new beauty markets where consumer preferences, pricing, and store economics may differ from the US. With Q4 results due on March 12 and the market looking for 9.7% year on year revenue growth after a 1.9% decline in the comparable quarter last year, investors will be watching whether these initiatives are starting to show up in sales trends, margins, and guidance, or whether they are still primarily an investment phase that adds to costs before scale benefits emerge.

How This Fits Into The Ulta Beauty Narrative The UK and Middle East expansion aligns with the community narrative that sees Ulta broadening its reach through wellness, exclusive brands, and new geographies to support revenue growth over time. Heavier promotions around 21 Days of Beauty and upfront spending on Space NK and UAE stores echo the narrative’s concern that higher store, payroll, and investment costs could pressure operating margins. The specific impact of the Space NK acquisition and the first UAE locations on customer mix, loyalty engagement, and store productivity is not fully captured in the narrative, which focuses more on the overall concept of international growth than on deal level execution.

Knowing what a company is worth starts with understanding its story.

Check out one of the top narratives in the Simply Wall St Community for Ulta Beauty to help decide what it is worth to you.

The Risks and Rewards Investors Should Consider ⚠️ Integration and execution risk around Space NK, Mexico, and the UAE, where consumer behavior, store economics, and competition may differ meaningfully from the US. ⚠️ Reliance on major promotional events such as 21 Days of Beauty, which can strain margins if discounting becomes a regular requirement to sustain traffic against peers such as Sephora or department store beauty counters. 🎁 The 21 Days of Beauty event can reinforce Ulta’s loyalty ecosystem, encouraging repeat purchases and higher basket sizes, especially with rewards tiers and shipping benefits. 🎁 Expanding into established beauty hubs such as the UK and the Gulf region opens new store and omnichannel revenue streams that are not tied solely to the US specialty retail market. What To Watch Going Forward

From here, you may want to track how Ulta links its large US promotions and overseas rollout to hard numbers in the upcoming Q4 earnings report and fiscal 2026 outlook. Attention will likely fall on comparable sales, gross margin, and any commentary on early results from Space NK and new international partners, as well as how promotional intensity trends over the year. Competitive responses from Sephora, Boots, and direct to consumer brands will also help indicate how much room Ulta has to differentiate its model outside the US.

To ensure you are always in the loop on how the latest news impacts the investment narrative for Ulta Beauty, head to the

community page for Ulta Beauty to stay updated on the top community narratives.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com