After The Recent Share Price Slide")

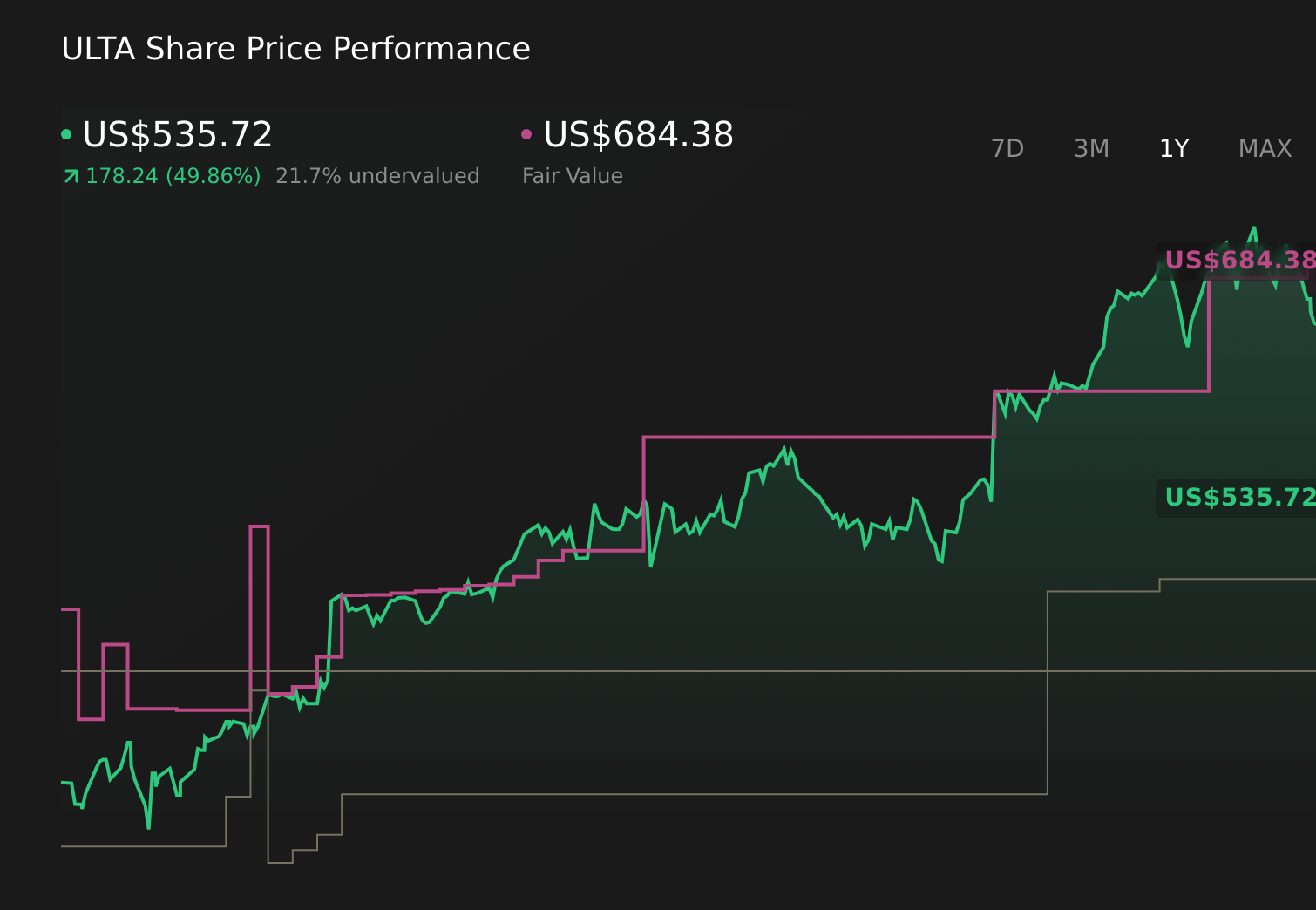

If you are wondering whether Ulta Beauty’s share price still makes sense after its recent swings, this article will walk through what the current market tag might be telling you about the stock’s value. The shares most recently closed at US$535.72, after a 17.1% decline over the last 7 days and a 21.6% decline over the last 30 days, set against a 49.9% return over the past year. Recent price moves have come alongside ongoing attention on Ulta Beauty’s position in the US specialty retail space, including how it competes within prestige and mass beauty categories and its footprint inside major retailers. These themes together frame how investors are thinking about the balance between long term growth potential and short term risk. Ulta Beauty currently has a valuation score of 2 out of 6, which reflects the number of checks where it screens as undervalued. Next, we will break that down across different valuation methods and finish with a way to look beyond the headline multiples to the fuller story.

Ulta Beauty scores just 2/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Ulta Beauty Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model looks at the cash Ulta Beauty is expected to generate in the future and then discounts those projected dollars back to today to estimate what the business might be worth now.

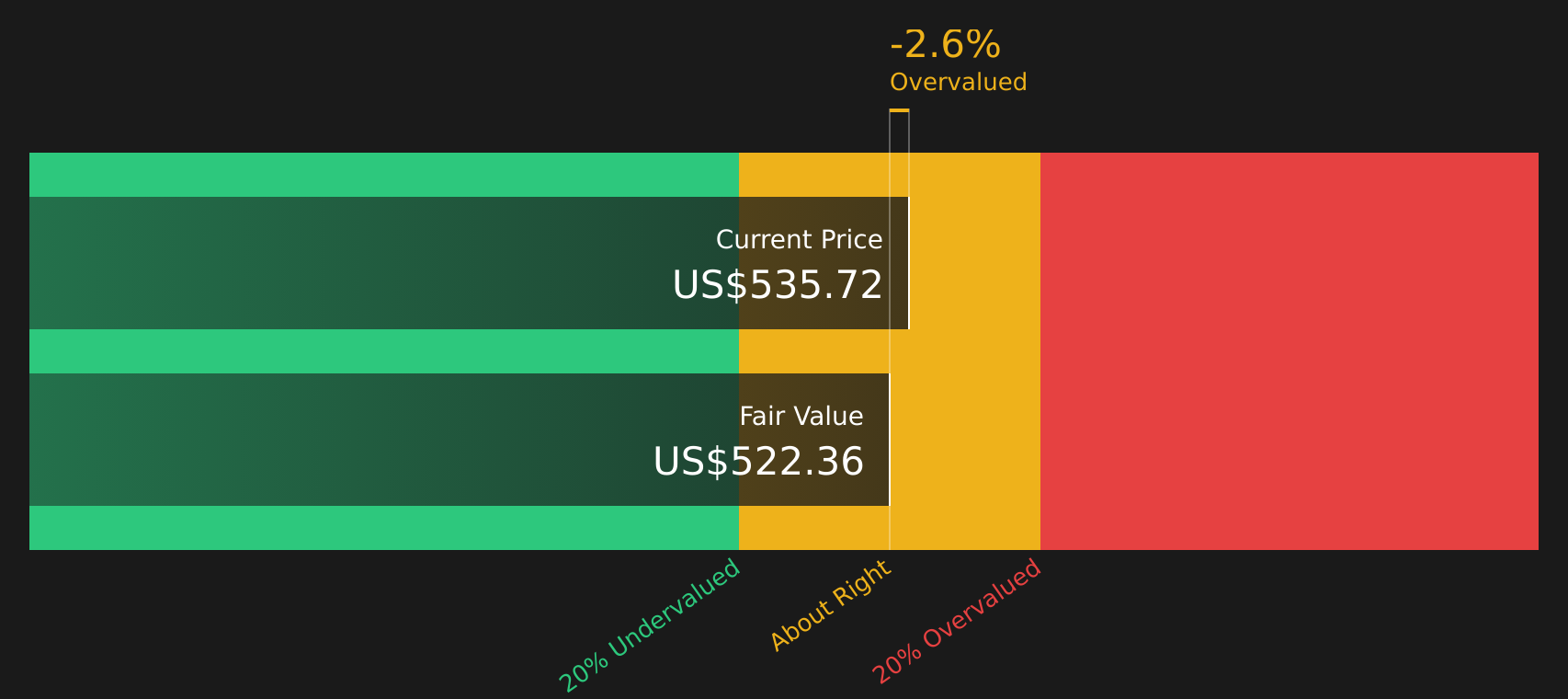

Ulta Beauty’s last twelve months Free Cash Flow is about $1.06b. Analysts and extrapolated estimates point to Free Cash Flow of $1.27b in the year to 2030, based on a two stage Free Cash Flow to Equity model that uses both analyst inputs and Simply Wall St’s own extensions beyond the typical five year forecast window.

When all of those projected cash flows are discounted back to today, the model arrives at an estimated intrinsic value of about $522.35 per share. Compared with the recent share price of US$535.72, the DCF suggests the stock is about 2.6% overvalued. This is a relatively small gap and falls within a range where the market price and model value are broadly aligned.

Result: ABOUT RIGHT

Ulta Beauty is fairly valued according to our Discounted Cash Flow (DCF), but this can change at a moment’s notice. Track the value in your watchlist or portfolio and be alerted on when to act.

ULTA Discounted Cash Flow as at Mar 2026

ULTA Discounted Cash Flow as at Mar 2026

Approach 2: Ulta Beauty Price vs Earnings

For a profitable business like Ulta Beauty, the P/E ratio is a straightforward way to think about what you are paying for each dollar of current earnings. Investors generally accept that higher expected growth or lower perceived risk can support a higher P/E, while slower growth or higher risk usually call for a lower, more conservative P/E.

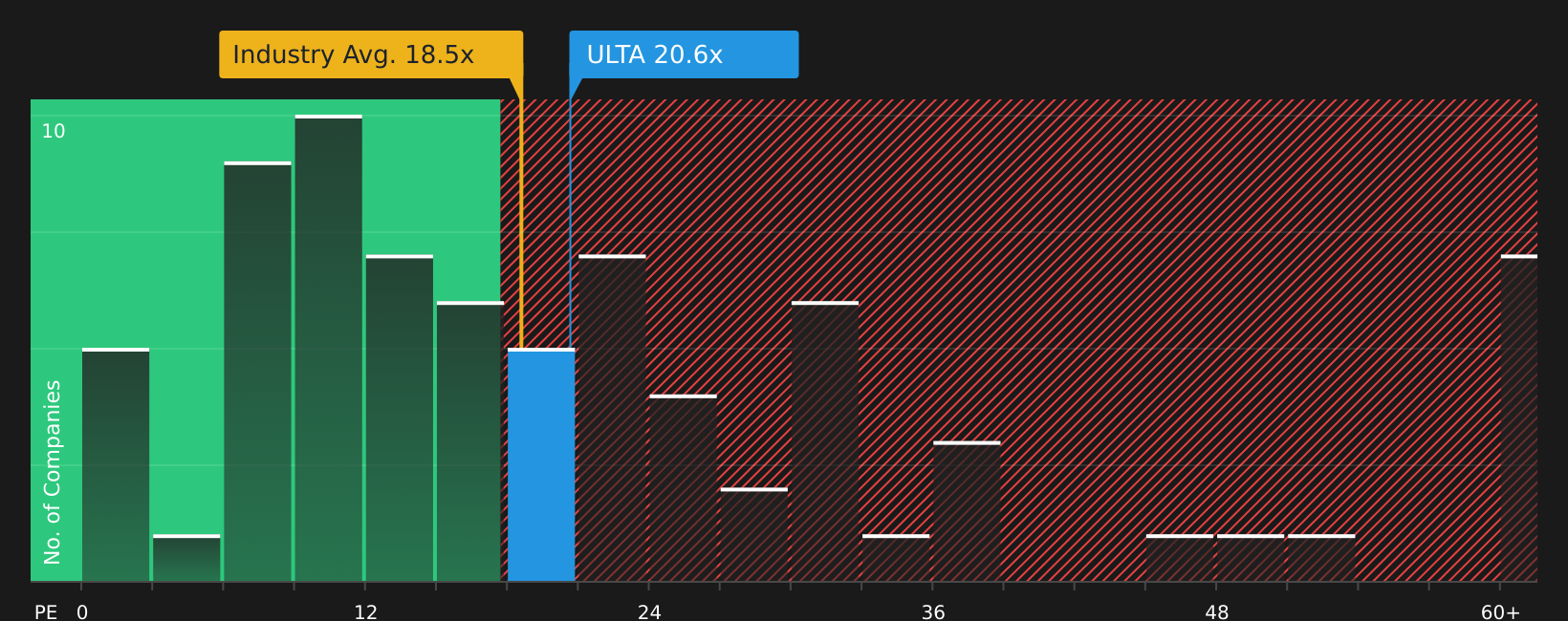

Ulta Beauty currently trades on a P/E of 20.60x. That sits above the Specialty Retail industry average of 18.49x, yet below the peer group average of 32.98x, so the stock is priced somewhere between the broader sector and higher rated peers. Simply Wall St’s Fair Ratio for Ulta Beauty is 18.26x. This Fair Ratio is a proprietary estimate of what the P/E might be given the company’s earnings growth profile, industry, profit margins, market value and risk factors.

Compared with simple peer or industry comparisons, the Fair Ratio aims to be more tailored, because it folds in both company specific and sector level characteristics instead of assuming one size fits all. Setting Ulta Beauty’s current P/E of 20.60x against the Fair Ratio of 18.26x points to the shares trading at a premium to that model based view.

Result: OVERVALUED

NasdaqGS:ULTA P/E Ratio as at Mar 2026

NasdaqGS:ULTA P/E Ratio as at Mar 2026

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 18 top founder-led companies.

Upgrade Your Decision Making: Choose your Ulta Beauty Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives, which are simply your story about a company linked directly to a set of numbers like revenue, earnings, margins and a fair value that you can compare with today’s price.

On Simply Wall St’s Community page, Narratives are an accessible tool that lets you connect Ulta Beauty’s business story to a financial forecast and a fair value estimate. You can then see how that fair value stacks up against the current share price to help you decide whether you see room to buy, trim or simply watch.

Because Narratives update when fresh information such as earnings, guidance or news is added, they do not stay static. You can see a wide range of views, from one Ulta Beauty Narrative that arrives at a fair value of about US$427 per share to another that points closer to US$790, reflecting very different expectations about future growth, profitability and the multiple investors might be willing to pay.

For Ulta Beauty, here are previews of two leading Ulta Beauty Narratives:

Fair value in this narrative: about US$684.38 per share

Implied pricing: about 21.7% below this fair value level based on the recent close

Revenue growth assumption: 6.36% a year

Analysts see wellness, exclusive brands, and a curated marketplace as important drivers of higher sales and potentially stronger margins over time. Digital tools, store based fulfillment, and a large loyalty base of 45.8 million members are viewed as key supports for repeat spending and earnings resilience. International expansion into the UK, Ireland, Mexico, and the Middle East adds new revenue streams, although it also brings execution and cost risk that is built into the forecasts.

Fair value in this narrative: about US$427.41 per share

Implied pricing: about 25.4% above this fair value level based on the recent close

Revenue growth assumption: 4.5% a year

This view highlights Ulta’s strong margins, high return on capital, and lack of debt, but questions how much growth is left for a largely US focused store network. The author expects pressure from e commerce and other retailers, with a risk that margins and earnings soften before settling into more modest long term growth. Perceived undervaluation in this narrative is tied mainly to multiple expansion, so the author sees limited edge if sales growth stays closer to 4% a year and competition remains intense.

Together, these Narratives frame a wide valuation range and different expectations for Ulta Beauty’s future. If you want to see how other investors connect their stories to the numbers, you can browse the full set of Narratives on the company’s Community page and compare them with your own assumptions before making any decision.

Do you think there’s more to the story for Ulta Beauty? Head over to our Community to see what others are saying!

NasdaqGS:ULTA 1-Year Stock Price Chart

NasdaqGS:ULTA 1-Year Stock Price Chart

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com