Report Overview

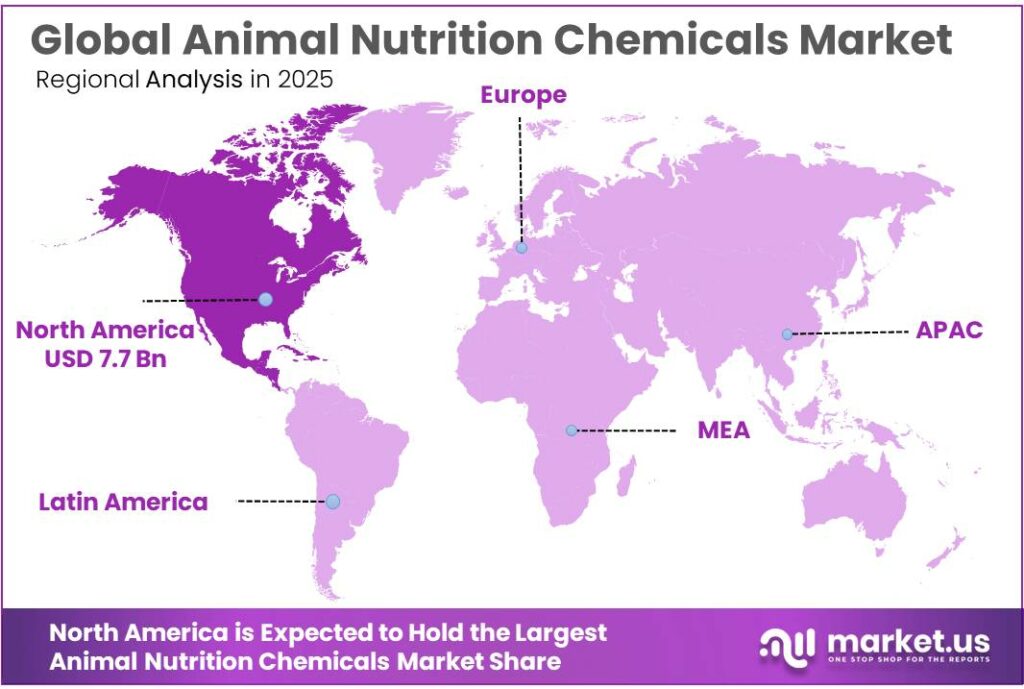

The Global Animal Nutrition Chemicals Market size is expected to be worth around USD 27.0 Billion by 2035, from USD 15.7 Billion in 2025, growing at a CAGR of 5.6% during the forecast period from 2026 to 2035. In 2025, Asia Pacific held a dominant market position, capturing more than a 49.6% share, holding USD 7.7 Billion revenue.

Animal nutrition chemicals refer to feed additives, specialty nutrients, acidifiers, amino acids, enzymes, vitamins, minerals, antioxidants and gut-health solutions used to improve feed efficiency, animal health, product quality and production economics. The industry sits at the intersection of livestock productivity, food safety and regulatory science.

Its relevance is reinforced by the scale of global feed manufacturing: the 2025 Alltech Agri-Food Outlook estimated world feed production at 1.396 billion metric tons in 2024, up 1.2% year on year, based on data from more than 28,000 feed mills across 140 countries. At the same time, FAO projected global meat production at 373 million tonnes in 2024, up 1.4% from 2023, confirming that industrial livestock systems continue to require large volumes of nutritionally optimized feed inputs.

The main driving factors are therefore clear: rising consumption of animal protein, feed-cost optimization, disease-management pressure, mycotoxin risk, and a global push to curb indiscriminate antimicrobial use. WOAH reported that antimicrobial use in animals across 71% of global animal biomass fell by 5% between 2020 and 2022, from 102 mg to 97 mg per kg of animal biomass, which strengthens the case for non-antibiotic feed additives such as enzymes, acidifiers, probiotics and phytogenics.

In parallel, the European Union continued authorisation activity under Regulation (EC) No 1831/2003, including the April 2025 renewal of L-tyrosine for all animal species after a prior 10-year authorisation, and the July 2025 authorisation of tea tree essential oil with maximum-content safeguards linked to methyleugenol.

On the government funding side, USDA-NIFA’s FY2026 AFRI Foundational and Applied Science program outlined approximately $300 million for supported programs within a broader anticipated AFRI funding level of about $407 million, signaling continuing public support for agricultural science, including nutrition-linked productivity research.

Key Takeaways

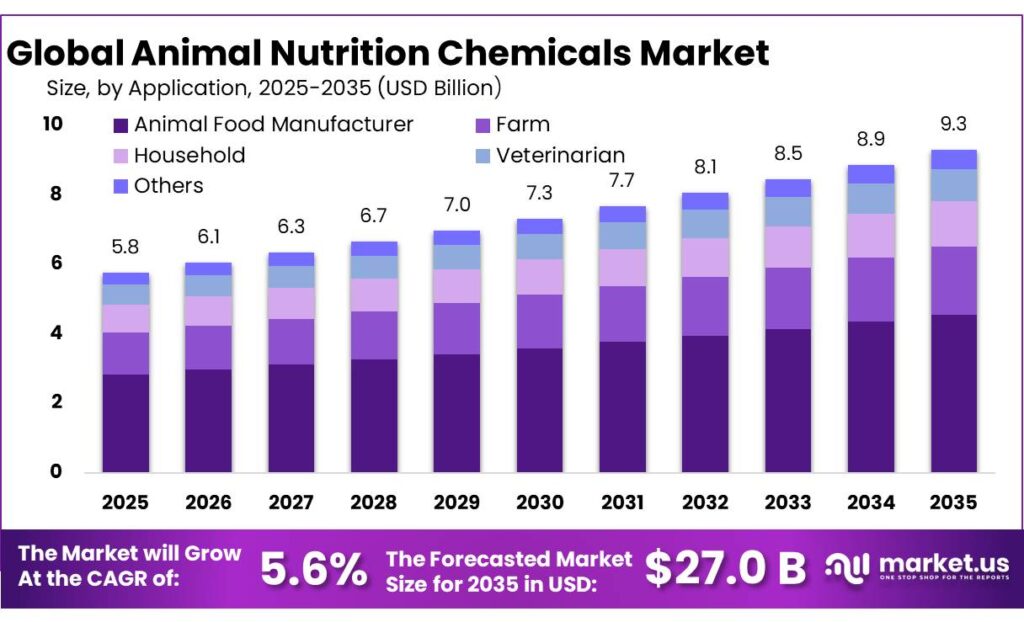

Animal Nutrition Chemicals Market size is expected to be worth around USD 27.0 Billion by 2035, from USD 15.7 Billion in 2025, growing at a CAGR of 5.6%.

Amino Acid held a dominant market position, capturing more than a 32.5% share.

Animal Food Manufacturer held a dominant market position, capturing more than a 49.1% share.

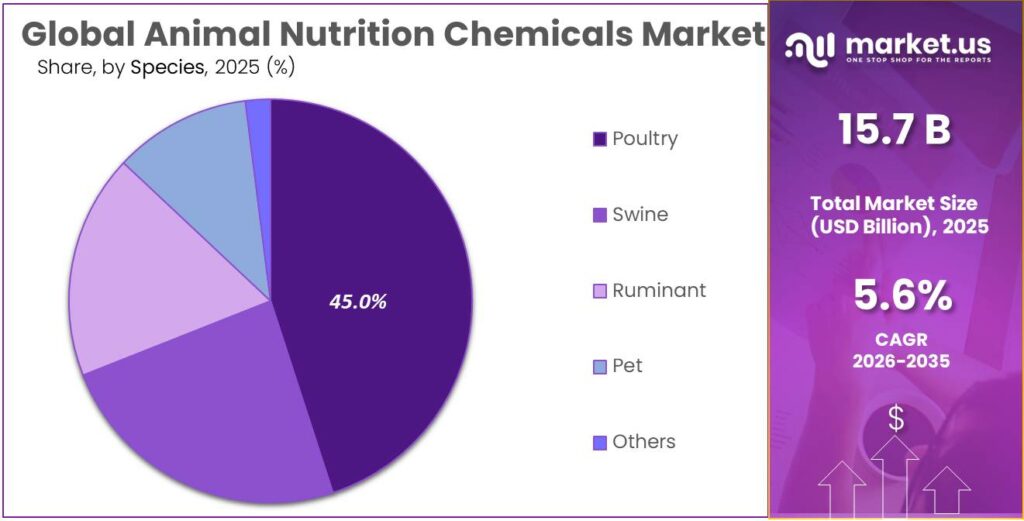

Poultry held a dominant market position, capturing more than a 45.3% share.

Asia Pacific leads the Animal Nutrition Chemicals market, accounting for a dominant 49.6% share valued at USD 7.7 Bn.

By Product Type Analysis

Amino Acid dominates with 32.5% driven by its essential role in animal growth and feed efficiency

In 2025, Amino Acid held a dominant market position, capturing more than a 32.5% share. This strong position comes from its key role in improving animal nutrition and overall productivity. Amino acids such as lysine, methionine, and threonine are widely used in animal feed to support better growth, muscle development, and feed conversion efficiency. Farmers and livestock producers rely on these nutrients to ensure animals get balanced diets, especially in poultry, swine, and aquaculture farming. The increasing demand for high-quality meat and dairy products has also pushed the use of amino acids in feed formulations.

By Application Analysis

Animal Food Manufacturer dominates with 49.1% as bulk feed production drives consistent demand

In 2025, Animal Food Manufacturer held a dominant market position, capturing more than a 49.1% share. This strong lead comes from the large-scale demand for processed and balanced animal feed across livestock, poultry, and aquaculture sectors. Feed manufacturers play a central role in integrating nutrition chemicals like amino acids, vitamins, and minerals into standardized feed products. Their ability to produce in bulk and maintain consistent quality makes them a key consumer of animal nutrition chemicals. Growing demand for high-quality meat, milk, and eggs has further pushed feed producers to use advanced nutritional inputs.

By Species Analysis

Poultry dominates with 45.3% driven by high demand for chicken and eggs worldwide

In 2025, Poultry held a dominant market position, capturing more than a 45.3% share. This strong position is mainly due to the growing global demand for chicken meat and eggs, which are considered affordable and widely consumed protein sources. Poultry farming requires well-balanced feed to ensure fast growth and better productivity, which increases the use of animal nutrition chemicals such as amino acids, vitamins, and enzymes. Farmers focus heavily on feed quality in poultry because even small improvements in nutrition can lead to better weight gain and feed efficiency.

Key Market Segments

By Product Type

Amino Acid

Vitamin

Mineral

Enzyme

Fish Oil & Lipid

Carotenoid

Eubiotics

Others

By Application

Animal Food Manufacturer

Farm

Household

Veterinarian

Others

By Species

Poultry

Swine

Ruminant

Pet

Others

Emerging Trends

Shift Toward Antibiotic-Free and Natural Feed Additives Becoming a Key Trend

One of the most important trends in the animal nutrition chemicals market is the clear move away from antibiotics and toward natural, safer feed additives. For many years, antibiotics were widely used to improve growth and prevent disease in livestock. However, growing concerns about antimicrobial resistance have changed how the industry operates. According to the Food and Agriculture Organization (FAO), global livestock antibiotic use is expected to rise by nearly 30% by 2040 if no action is taken, highlighting the seriousness of the issue.

Governments and global health bodies have started taking strict actions. The European Union completely banned the use of antibiotics as growth promoters back in 2006, and similar restrictions have been introduced in other regions as well. The World Health Organization has also recommended reducing antibiotic use in food-producing animals to protect human health. These steps are pushing producers to find safer alternatives.

Focus on Sustainable Livestock Production and Efficiency Improving Ingredient Demand

FAO data shows that improving livestock productivity can significantly reduce the need for antibiotics, with optimized systems potentially cutting usage by up to 57%, while still maintaining production levels. This highlights how better nutrition and management can directly improve both performance and sustainability.

At the same time, livestock farming has become more intensive, which increases the need for precise and balanced nutrition. Feed additives are now being used not just for growth but also to improve animal health, reduce emissions, and support better feed conversion. For example, certain feed strategies can lower methane emissions from livestock, which is becoming a key focus area for governments and environmental agencies.

Drivers

Rising Global Demand for Animal Protein Driving Feed and Nutrition Needs

One of the biggest drivers for the animal nutrition chemicals market is the steady rise in global demand for animal protein such as meat, milk, and eggs. As population grows and incomes improve, especially in developing countries, people naturally shift toward protein-rich diets. According to the Food and Agriculture Organization (FAO), annual meat consumption in developing countries is expected to increase from 25.5 kg per person to 37 kg per person by 2030, showing a clear upward trend in protein demand.

Governments and global food bodies are also encouraging higher efficiency in livestock farming to ensure food security. For example, FAO highlights that food demand could grow by 60% by 2050, pushing the need for more efficient animal production systems. This creates a strong need for nutrition chemicals that help animals grow faster, stay healthier, and convert feed more efficiently. As a result, the rising demand for animal protein is not just increasing livestock production but also driving consistent growth in the animal nutrition chemicals market.

Expansion of Livestock Farming and Productivity Focus Supporting Market Growth

Another major factor supporting growth is the rapid expansion of livestock farming across the world. To meet increasing demand, producers are not only raising more animals but also focusing on improving productivity per animal. Data shows that the global chicken population alone reached around 26.6 billion in 2022, which is a 68% increase compared to 2002, highlighting how quickly livestock farming is expanding.

At the same time, future projections also show continued growth. According to OECD-FAO outlook data, global meat consumption is expected to increase significantly, with poultry consumption alone projected to grow by around 21% by 2034. This means producers will continue investing in better feed solutions to keep up with demand.

Restraints

Rising Feed Cost and Price Volatility Limiting Profit Margins

One of the biggest restraining factors for the animal nutrition chemicals market is the continuous rise and fluctuation in feed costs. Feed is the most expensive part of livestock production, and any increase in raw material prices directly affects the use of nutrition chemicals. Studies show that feed alone accounts for up to 70% of the total cost of livestock production, making it the most critical cost component for farmers.

Global price trends also highlight this pressure. According to the FAO Food Price Index, key inputs like cereals and vegetable oils have seen noticeable increases, with vegetable oil prices rising by 3.3% in a single month and reaching their highest level since 2022. At the same time, global events have made the situation worse. FAO reported that disruptions such as geopolitical conflicts could push grain prices up by as much as 20%, which directly impacts animal feed costs.

Supply Chain Disruptions and Resource Dependency Creating Market Pressure

Another major challenge is the heavy dependency on agricultural raw materials and the supply chain issues linked to them. Animal nutrition chemicals rely on inputs like soybean meal, corn, and other crops, which are already under pressure due to global demand. In fact, soybean meal alone accounts for about 75% of all protein used in livestock feed worldwide, showing how dependent the industry is on a few key resources.

At the same time, a large portion of global agricultural resources is already tied to animal feed production. Research shows that over 30% of global cereal production and up to 40% of arable land is used for animal feed, which limits flexibility in supply. This high dependency means that any disruption—whether due to climate change, poor harvests, or trade restrictions—can quickly impact availability and prices.

Opportunity

Rising Demand for High-Efficiency and Sustainable Feed Solutions Creating Growth Opportunities

One of the biggest growth opportunities in the animal nutrition chemicals market is the increasing focus on feed efficiency and sustainable livestock production. As global demand for animal protein continues to rise, producers are under pressure to produce more with fewer resources. According to the FAO, global demand for food is expected to grow by 60% by 2050, while animal protein production is projected to increase significantly, including nearly 70% growth in meat production

This puts strong pressure on farmers to improve how animals convert feed into meat, milk, or eggs. Nutrition chemicals such as amino acids, enzymes, and feed additives play a key role in improving feed conversion ratios and reducing waste. At the same time, livestock already consumes about 6 billion tonnes of feed annually, showing the massive scale of this sector and the opportunity for efficiency improvements

Expansion of Industrial Feed Production and Livestock Scaling Supporting Market Growth

Another strong opportunity lies in the rapid expansion of industrial feed production and large-scale livestock farming. As demand for animal-based food increases, farming is becoming more organized and commercialized, which directly increases the use of standardized feed and nutrition chemicals. The FAO reports that the global feed sector produces more than 1 billion tonnes of livestock feed annually, with a commercial turnover exceeding USD 400 billion, showing how large and structured this industry has become

Recent data also indicates that global animal feed production reached around 1.29 billion metric tons in 2023, reflecting steady growth in feed demand worldwide. This growth is closely tied to the expansion of poultry, dairy, and aquaculture sectors, where consistent and high-quality feed is essential.

Regional Insights

Asia Pacific dominates the Animal Nutrition Chemicals market with 49.6% share, valued at USD 7.7 Bn

Asia Pacific leads the Animal Nutrition Chemicals market, accounting for a dominant 49.6% share valued at USD 7.7 Bn, supported by its massive livestock population and rapidly growing demand for animal-based food products. The region is home to over 40% of global livestock production, making it the largest contributor to feed and nutrition demand worldwide. Countries like China and India play a central role, driven by large-scale poultry, dairy, and aquaculture industries. For instance, China alone produced over 277 million metric tons of corn in 2023, a major raw material for feed production

The region also dominates global feed production, with Asia-Pacific contributing around 466 million tons, or 36.8% of total compound feed output, highlighting its strong manufacturing base. This large-scale feed production directly supports the demand for amino acids, vitamins, and other nutrition chemicals used to improve animal health and productivity. Additionally, rising population and urbanization are key factors, with Asia accounting for nearly 60% of the global population, increasing pressure on food supply systems.

Key Regions and Countries Insights

North America

Europe

Germany

France

The UK

Spain

Italy

Rest of Europe

Asia Pacific

China

Japan

South Korea

India

Australia

Rest of APAC

Latin America

Brazil

Mexico

Rest of Latin America

Middle East & Africa

GCC

South Africa

Rest of MEA

Key Players Analysis

Balchem Corporation is a well-established player in specialty ingredients and animal nutrition. The company reported USD 951.7 million in total revenue in 2025, with its Animal Nutrition & Health segment contributing a significant share. It operates in 70+ countries and serves a wide range of livestock markets. Balchem invests approximately 4–5% of revenue into R&D. Its encapsulation technology supports 100+ ingredient solutions, helping improve nutrient delivery and feed efficiency across dairy, poultry, and swine segments.

BASF SE is a global leader in chemicals, including animal nutrition ingredients such as vitamins and feed additives. In 2025, BASF reported total sales of around EUR 68.9 billion, with its Nutrition & Care segment contributing a key portion. The company operates in 90+ countries with production sites in over 80 locations worldwide. BASF invests heavily in innovation, with annual R&D spending exceeding EUR 2 billion. Its animal nutrition portfolio includes 50+ key ingredients, widely used in livestock and aquaculture feed.

Cargill Incorporated is one of the largest players in the animal nutrition chemicals market, with strong global operations. The company generated approximately USD 177 billion in revenue in 2025, supported by its diversified food and agriculture business. It operates in 70+ countries and employs over 160,000 people. Cargill produces animal feed in 250+ facilities worldwide, serving multiple livestock sectors. Around 30% of its business is linked to animal nutrition, with continuous investment in feed innovation and sustainable solutions.

Top Key Players Outlook

Aumgene Biosciences Pvt. Ltd.

Balchem Corporation

BASF SE

Cargill Incorporated

Evonik Industries AG (RAG-Stiftung)

Kemin Industries Inc.

Koninklijke DSM NV

Novozymes A/S

Tata Chemicals Limited.

Recent Industry Developments

In 2025, BASF SE continued to hold a strong position in the animal nutrition chemicals sector through its Nutrition & Health division, which focuses on feed additives and performance ingredients. The company reported €6,509 million in sales from its Nutrition & Care segment in 2025, showing the scale of its nutrition-related business.

In 2025, Cargill Incorporated continued to play a major role in the animal nutrition chemicals sector through its Animal Nutrition & Health business, which focuses on feed additives, premixes, and performance solutions for livestock and aquaculture. The company reported USD 154 billion in total revenue in fiscal 2025, slightly down from USD 160 billion in 2024, reflecting broader commodity market changes but still showing its massive global scale.

Report Scope