Expanded Pet Insurance Partnerships Redefine Its Health and Wellness Financing Narrative?")

Earlier this month, Synchrony announced a partnership with Figo Pet Insurance that lets policyholders pay vet bills with CareCredit and have approved Figo reimbursements automatically credited back to their CareCredit accounts, simplifying how pet owners handle upfront veterinary expenses.

By adding Figo to an ecosystem that already includes Pets Best and Pumpkin, Synchrony extends this seamless pet insurance reimbursement experience to more than 1.20 million insured policyholders and deepens its reach in pet health financing.

Next, we’ll examine how this expanded pet health reimbursement ecosystem could influence Synchrony’s investment narrative around health and wellness financing.

Capitalize on the AI infrastructure supercycle with our selection of the 35 best ‘picks and shovels’ of the AI gold rush converting record-breaking demand into massive cash flow.

To own Synchrony, you generally need to believe its card and financing platforms can stay relevant as spending habits, regulation, and digital payments evolve. Near term, the key catalyst is how loan growth and credit performance show up in upcoming results, while major partner concentration and regulatory changes remain central risks. The Figo partnership strengthens Synchrony’s health and wellness financing footprint, but does not materially change those higher level drivers on its own.

The new Figo Pet Insurance integration ties directly into Synchrony’s push into health, wellness, and pet financing, building on earlier deals with Pets Best and Pumpkin. This matters because it broadens where CareCredit can be used and deepens embedded finance across veterinary care, an area Synchrony has been expanding alongside its larger retail, e commerce, and BNPL relationships that many investors watch as core growth catalysts.

Yet, while this added convenience is appealing, investors should still be aware of how concentrated Synchrony remains in a handful of large retail partners and what happens if any of them…

Read the full narrative on Synchrony Financial (it’s free!)

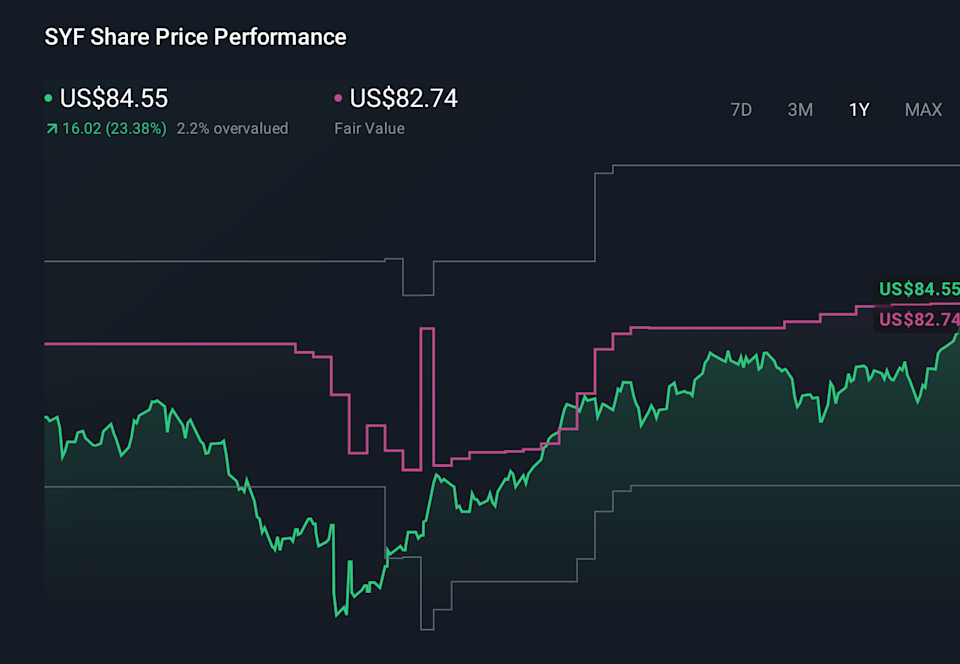

Synchrony Financial’s narrative projects $16.5 billion revenue and $3.3 billion earnings by 2028. This requires 21.7% yearly revenue growth and about a $0.1 billion earnings increase from $3.2 billion today.

Uncover how Synchrony Financial’s forecasts yield a $90.26 fair value, a 38% upside to its current price.

SYF 1-Year Stock Price Chart

SYF 1-Year Stock Price Chart

Some of the lowest ranked analysts take a much harsher view, assuming revenue of about US$15.9 billion with flat US$2.9 billion earnings, so if you worry about weaker purchase volumes and margin pressure, it is worth comparing those expectations with how new pet health partnerships might eventually influence the story.

Explore 8 other fair value estimates on Synchrony Financial – why the stock might be worth just $74.31!

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

Don’t miss your shot at the next 10-bagger. Our latest stock picks just dropped:

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include SYF.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com