Report Overview

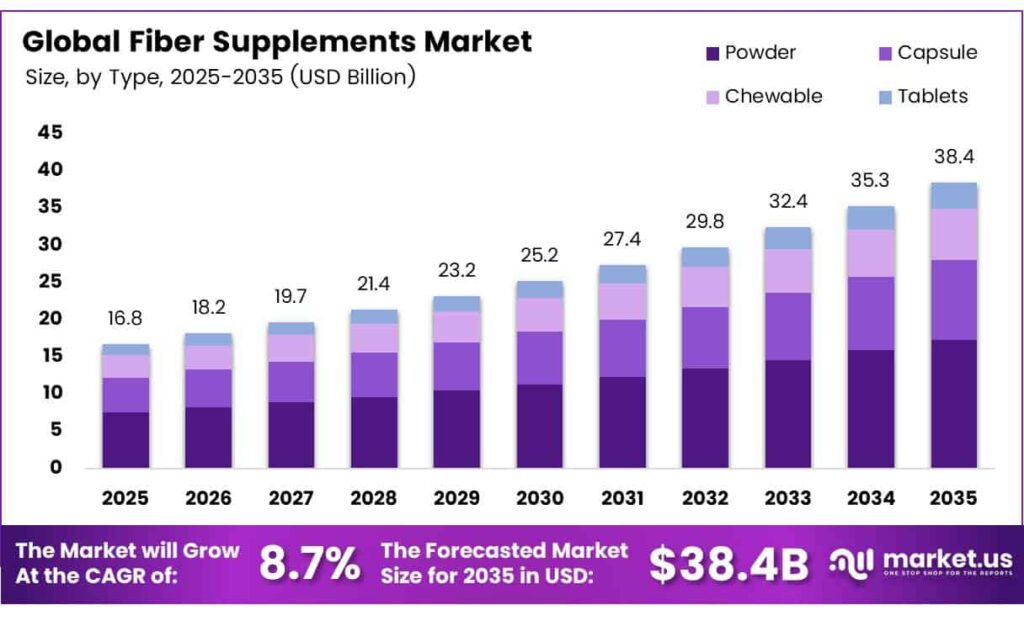

The Global Fiber Supplements Market size is expected to be worth around USD 38.4 billion by 2035 from USD 16.8 billion in 2025, growing at a CAGR of 8.7% during the forecast period 2026 to 2035.

The fiber supplements market covers dietary products that deliver soluble and insoluble fiber to consumers who do not meet daily intake needs through food alone. These products include powders, capsules, chewables, and tablets derived from sources such as legumes, psyllium husk, fruits and vegetables, and whole grains. Fiber supplements support digestive regularity, cardiovascular health, and blood sugar management.

Consumer awareness of gut microbiome health drives strong demand across all age groups. Healthcare professionals increasingly recommend fiber supplementation for patients managing metabolic disorders, obesity, and high cholesterol. Moreover, aging populations seek consistent fiber intake to maintain cardiovascular function and gastrointestinal regularity without relying solely on dietary changes.

The daily value for dietary fiber is 28 grams per day on Supplement Facts labels. This benchmark serves as the regulatory reference point for all fiber supplement brands operating in the U.S. market, directly influencing product dosage design and labeling compliance strategies.

A product claiming 20% Daily Value qualifies as “high fiber,” equating to 5.6 grams of fiber per serving. This threshold guides formulation decisions and positions premium fiber supplements as clinically relevant nutrition solutions rather than general wellness accessories.

The market benefits from growing interest in functional nutrition and preventive healthcare. Consumers shifting away from processed diets actively seek supplemental fiber to close nutritional gaps. Additionally, the rise of personalized wellness platforms and direct-to-consumer e-commerce channels accelerates product accessibility and drives repeat purchase behavior across digital-first buyers.

Key Takeaways

The Global Fiber Supplements Market is valued at USD 16.8 billion in 2025 and is projected to reach USD 38.4 billion by 2035 at a CAGR of 8.7% during the forecast period 2026 to 2035.

Powder holds the dominant share at 37.5% in 2025.

Legumes lead the segment with a 32.7% market share.

Conventional fiber supplements dominate with a 67.3% share.

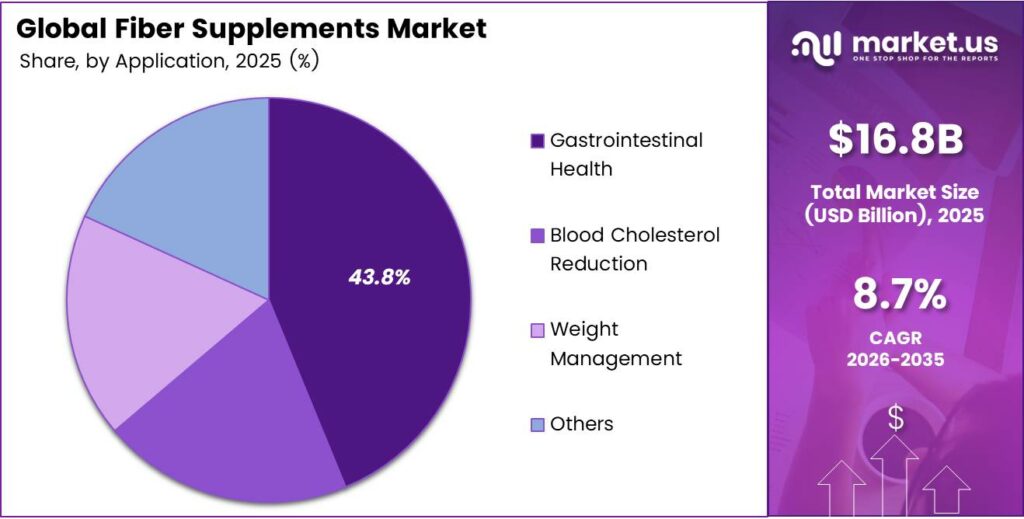

Gastrointestinal Health accounts for the largest share at 43.8%.

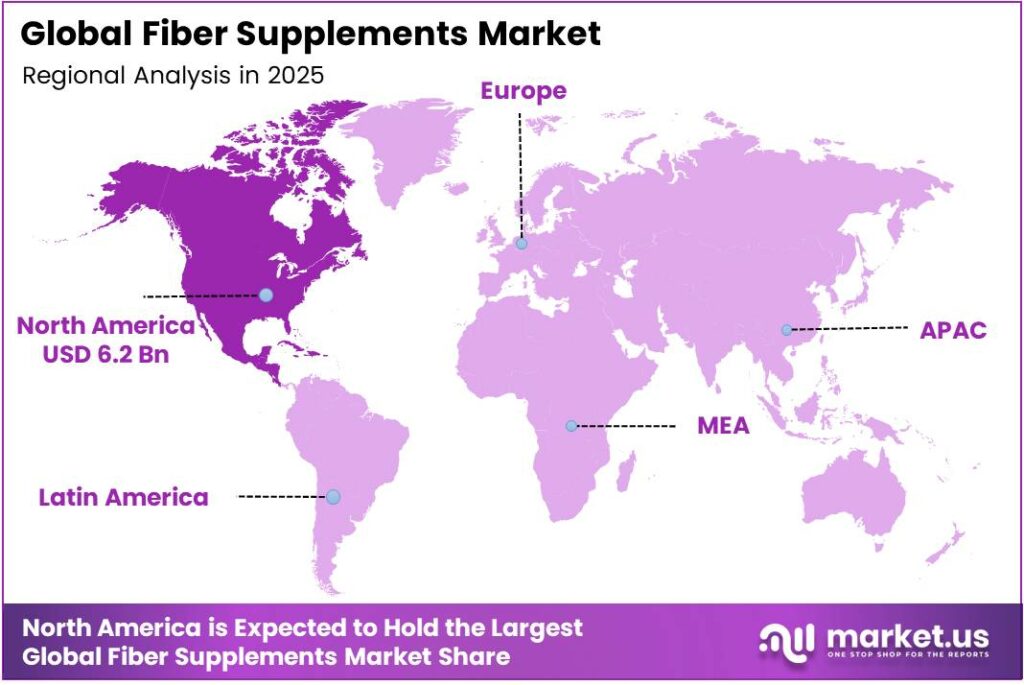

North America leads all regions with a 36.9% share, valued at USD 6.2 billion in 2025.

Type Analysis

Powder dominates with 37.5% due to ease of use, flexible dosing, and high consumer adoption across age groups.

In 2025, Powder held a dominant market position in the By Type segment of the Fiber Supplements Market, with a 37.5% share. Powder formats offer flexible dosing and easy integration into beverages and food. Moreover, consumers prefer powders for their rapid mixing convenience and wider availability across retail and e-commerce nutrition platforms.

Capsule supplements hold a significant share driven by their precise dosing, portability, and appeal to health-conscious professionals. Capsules require no preparation and suit busy lifestyles where convenience is a priority. Additionally, capsule formats reduce taste-related barriers, making them a preferred choice among consumers sensitive to fiber supplement flavors.

Chewable fiber supplements attract pediatric users, elderly consumers, and individuals who experience difficulty swallowing tablets or capsules. These formats combine palatability with functional benefit delivery. Consequently, chewables expand market access by reaching demographic groups that traditional formats have historically underserved in the dietary supplement category.

Source Analysis

Legumes dominate with 32.7% due to their high natural fiber content, wide availability, and strong nutritional credibility.

In 2025, Legumes held a dominant market position in the By Source segment of the Fiber Supplements Market, with a 32.7% share. Legume-derived fiber delivers both soluble and insoluble fiber types, addressing multiple digestive health applications. Moreover, legumes carry strong scientific backing and consumer familiarity, supporting consistent demand across health-focused product formulations.

Fruit-based fiber supplements appeal to consumers seeking naturally sweet-flavored and antioxidant-rich formulations. Fruit-derived pectin and other soluble fibers support cholesterol reduction and digestive regularity. Additionally, fruit-based variants attract clean-label buyers who prefer recognizable plant-based ingredients over synthetic or processed fiber compounds.

Vegetables serve as a credible source of insoluble fiber in supplement formulations targeting digestive transit and colon health. Vegetable-derived fiber compounds align with whole-food nutrition philosophies. Consequently, they gain traction among health-conscious consumers who seek supplemental forms that closely mirror natural dietary fiber profiles from everyday food sources.

Nature Analysis

Conventional fiber supplements dominate with 67.3% due to wider availability, lower cost, and established brand trust.

In 2025, Conventional fiber supplements held a dominant market position in the By Nature segment of the Fiber Supplements Market, with a 67.3% share. Conventional products benefit from established supply chains, lower manufacturing costs, and mass-market retail penetration. Moreover, mainstream consumers prioritize affordability and accessibility over organic certification in routine supplement purchases.

Organic fiber supplements attract premium health-conscious consumers who seek chemical-free, sustainably sourced formulations. Growing awareness of pesticide residue concerns drives demand for certified organic fiber products. Additionally, e-commerce platforms and specialty health retailers actively expand organic supplement ranges, giving this segment meaningful long-term growth potential within the broader fiber category.

Application Analysis

Gastrointestinal Health dominates with 43.8% due to widespread digestive disorder prevalence and clinical recommendation support.

In 2025, Gastrointestinal Health held a dominant market position in the By Application segment of the Fiber Supplements Market, with a 43.8% share. Rising rates of irritable bowel syndrome, constipation, and gut microbiome imbalances fuel demand for targeted fiber-based digestive solutions. Moreover, gastroenterologists and general practitioners actively recommend fiber supplements as first-line interventions for digestive irregularity.

Blood Cholesterol Reduction represents a clinically validated application supported by soluble fiber research, including beta-glucan studies. Cardiovascular health awareness among middle-aged adults drives the adoption of cholesterol-lowering fiber formulations. Additionally, regulatory bodies in the U.S. and Europe permit cholesterol-related health claims on qualifying fiber products, strengthening product positioning and consumer trust.

Weight Management applications leverage fiber’s satiety-promoting properties to support calorie reduction and appetite control. The integration of fiber supplements with GLP-1 medication programs creates a growing clinical adjacency. Consequently, weight management fiber products attract attention from healthcare practitioners managing obesity and metabolic syndrome patient populations.

Key Market Segments

By Type

Powder

Capsule

Chewable

Tablets

By Source

Legumes

Fruits

Vegetables

Whole Grains

By Nature

By Application

Gastrointestinal Health

Blood Cholesterol Reduction

Weight Management

Others

Emerging Trends

Fibermaxxing Movement Drives Gen Z Engagement with Supplement Formats

The viral fibermaxxing movement on social media platforms actively engages Gen Z wellness seekers, converting digital interest into product purchases across e-commerce channels. According to APEDA, psyllium husk accounts for 3% of India’s tracked organic export basket, confirming its status as a high-value functional digestive ingredient. Moreover, fiber-forward packaging claims and fortified functional snacks expand consumer touchpoints beyond traditional supplement aisles.

Synbiotic Blends and Gut-Brain Health Trends Reshape Product Innovation

Brands increasingly develop synbiotic prebiotic fiber blends that target advanced microbiome optimization rather than basic digestive regularity. These formulations align fiber supplementation with postbiotic innovations and holistic gut-brain health research. Consequently, product developers position next-generation fiber supplements as comprehensive wellness tools that serve both digestive and neurological health outcomes for premium-segment consumers.

Drivers

Rising Gut Health Awareness and Digestive Disorder Prevalence Fuel Demand

Escalating consumer awareness of gut microbiome health drives consistent demand for preventive digestive wellness solutions. Rising rates of lifestyle-driven digestive disorders and metabolic imbalances push consumers toward fiber supplementation as a practical daily intervention. According to the U.S. FDA, the threshold of 5% Daily Value defines low fiber and 20% Daily Value defines high fiber, establishing clear formulation guidance that brands actively use to communicate product efficacy and differentiate offerings.

Aging Populations and Functional Nutrition Shift Expand the Consumer Base

Aging populations increasingly seek fiber supplements to manage cardiovascular and metabolic health as natural dietary fiber intake declines with age. Simultaneously, modern processed diets reduce whole-food fiber consumption, creating a measurable nutritional gap that supplement brands fill. Therefore, the convergence of demographic aging and shifting dietary patterns creates durable, long-term demand for convenient fiber supplementation solutions across multiple consumer segments.

Restraints

Consumer Preference for Whole-Food Fiber Limits Supplement Adoption

Many health-conscious consumers actively prefer obtaining dietary fiber from whole foods such as legumes, fruits, and vegetables rather than supplement products. This preference reduces the addressable market among nutritionally informed buyers who associate supplements with artificial or processed alternatives. Moreover, wellness communities and registered dietitians frequently advocate food-first approaches, which can discourage routine supplement use even among fiber-deficient individuals.

Side Effects and Efficacy Skepticism Create Adoption Barriers

Adverse gastrointestinal side effects, including bloating, gas, and cramping, discourage first-time and returning users from maintaining fiber supplement routines. Additionally, widespread consumer skepticism toward health claims on supplement labels reduces purchase confidence among non-committed buyers. Consequently, brands must invest in transparent clinical communication and gradual-dosing education to reduce abandonment rates and build lasting consumer trust in their fiber formulations.

Growth Factors

GLP-1 Adjacency and Innovative Delivery Formats Unlock New Revenue Streams

Fiber supplement integration with GLP-1 medication support programs creates a significant clinical growth opportunity. Healthcare practitioners recommend fiber as a complementary tool for patients managing weight with injectable therapies. Organic psyllium husk exports to Australia reached USD 8.96 million with 2,781.58 metric tonnes in FY2024-25, demonstrating strong global institutional demand for functional fiber ingredients used in supplement manufacturing pipelines.

Plant-Based Variants and D2C Platforms Accelerate Market Penetration

Development of gluten-free and plant-based fiber variants addresses the growing intolerance-driven dietary segment, expanding product relevance beyond mainstream supplement consumers. Additionally, personalized e-commerce and direct-to-consumer nutrition platforms enable brands to reach niche audiences with targeted messaging and subscription-based retention models. Therefore, digital-first distribution strategies amplify market penetration across health-conscious millennial and Gen Z buyer segments globally.

Regional Analysis

North America Dominates the Fiber Supplements Market with a Market Share of 36.9%, Valued at USD 6.2 Billion

North America leads the global fiber supplements market with a 36.9% share, valued at USD 6.2 billion in 2025. The United States drives this dominance through high consumer health awareness, well-established retail pharmacy infrastructure, and robust regulatory frameworks governing supplement labeling and claims. Moreover, the strong prevalence of digestive disorders and metabolic conditions accelerates consistent product demand across all distribution channels.

Europe holds a substantial share of the global fiber supplements market, driven by growing preventive healthcare adoption and strong functional food culture across Germany, France, and the United Kingdom. Regulatory alignment under EFSA health claim standards supports consumer confidence in scientifically validated fiber products. Additionally, rising demand for organic and plant-based supplement variants fuels premium segment growth throughout Western European markets.

Asia Pacific represents the fastest-growing regional market for fiber supplements, supported by rising disposable incomes, expanding health awareness, and a strong ingredient supply base. India plays a significant role as a leading producer and exporter of psyllium husk, a key functional fiber raw material. Consequently, regional manufacturing advantages and growing domestic health supplement consumption collectively accelerate the Asia Pacific’s market expansion trajectory.

Latin America demonstrates steady growth in fiber supplement adoption, led by Brazil and Mexico, where rising urbanization and dietary westernization increase nutritional gap awareness. Consumers in this region increasingly seek affordable digestive health solutions available through pharmacy retail and emerging e-commerce channels. Moreover, growing middle-class health consciousness creates favorable conditions for accessible fiber supplement product introductions.

Key Regions and Countries

North America

Europe

Germany

France

The UK

Spain

Italy

Rest of Europe

Asia Pacific

China

Japan

South Korea

India

Australia

Rest of APAC

Latin America

Brazil

Mexico

Rest of Latin America

Middle East & Africa

GCC

South Africa

Rest of MEA

Key Players Analysis

Procter and Gamble Co. maintains a strong position in the fiber supplements market through its established consumer healthcare division and extensive global retail distribution network. The company leverages deep brand equity and mass-market reach to promote digestive wellness products across pharmacy, grocery, and e-commerce channels. Moreover, its investment in consumer education and clinical communication reinforces product credibility and drives repeat purchase behavior.

Nestlé Health Science approaches the fiber supplements market with a science-backed nutritional health strategy that bridges pharmaceutical-grade credibility with consumer-friendly accessibility. The company develops targeted fiber formulations addressing gastrointestinal health, weight management, and metabolic wellness. Additionally, Nestlé Health Science integrates fiber solutions into its broader medical nutrition portfolio, positioning the brand strongly within clinical recommendation channels and hospital-linked distribution pathways.

GlaxoSmithKline plc competes in the fiber supplements space through its consumer health division, combining pharmaceutical research expertise with accessible over-the-counter product development. The company’s fiber offerings benefit from strong pharmacist recommendation rates and established trust within regulated retail health environments. Consequently, GlaxoSmithKline’s clinical heritage and regulatory compliance capabilities support competitive positioning in markets where credibility in efficacy is a primary purchase driver.

Abbott Laboratories brings medical nutrition expertise and a science-first development approach to the fiber supplements market. Abbott’s portfolio integrates fiber supplementation within broader clinical nutrition solutions targeting digestive, cardiovascular, and metabolic health outcomes. Therefore, the company’s strong relationships with healthcare practitioners and hospital networks give it a differentiated distribution advantage that consumer-only supplement brands find difficult to replicate at scale.

Top Key Players in the Market

Procter and Gamble Co.

Nestlé Health Science

GlaxoSmithKline plc

Abbott Laboratories

Johnson and Johnson Consumer Inc.

The Nature’s Bounty Co.

Sanofi S.A.

Pfizer Inc.

Bristol-Myers Squibb Company

Herbalife Nutrition Ltd.

Recent Developments

In March 2025, Procter and Gamble Co. expanded its digestive wellness supplement line by introducing a new psyllium-based powder format targeting daily gut microbiome support, enhancing its fiber portfolio across North American retail pharmacy channels.

In January 2025, Nestlé Health Science launched a synbiotic fiber blend combining prebiotic soluble fiber with probiotic strains, designed to address advanced gut-brain health outcomes and positioned for premium e-commerce and direct-to-consumer distribution.

In November 2024, Abbott Laboratories reinforced its clinical nutrition strategy by integrating higher-dose fiber formulations into its metabolic health product range, targeting patients in GLP-1 weight management programs with practitioner-recommended supplementation support.

Report Scope

![Dong-A Pharmaceutical's multi-vitamin "Oso Mall". [Dong-A Pharmaceutical Co., Ltd.]](https://www.vitaminrush.com/wp-content/uploads/2026/03/1774938881_news-p.v1.20260331.7396ccc4dbd2436e93d5b63f3b746970_P1-700x515.png "Dong-A Pharmaceutical’s premium multi-vitamin “Orthomol” ranked No. 1 in sales in the domestic multi..")