The form factor boom layers beauty onto health &

wellness, and it’s going to challenge VMS

operators

You wake up, drink your AG1, chew your multivitamin gummy, and

swallow your BPC-157 and TB-4 oral peptide supplements.

If you haven’t heard of the latter combination, it’s

known as the “Wolverine stack”—so-called for its

rapid healing properties (“wounds close faster, tendons knit

together” extolls one retailer)—and it is not approved

by the FDA or for human use. Regardless, it is a top seller on

e-commerce supplement sites and through social media, sought out by

self-informed consumers in the body-building world or those in

pain.

We see the spike in adoption of the Wolverine stack as a trend

for the beauty, health, and wellness industry, which is being

disrupted by medical-adjacent treatment plans. Consumers are

embedding supplementation into their lives as part of a more

holistic, results-based approach to wellbeing, beauty, and

achievement. The AlixPartners Professional VMS Survey finds

shifting loyalties among a curious population looking to optimize.

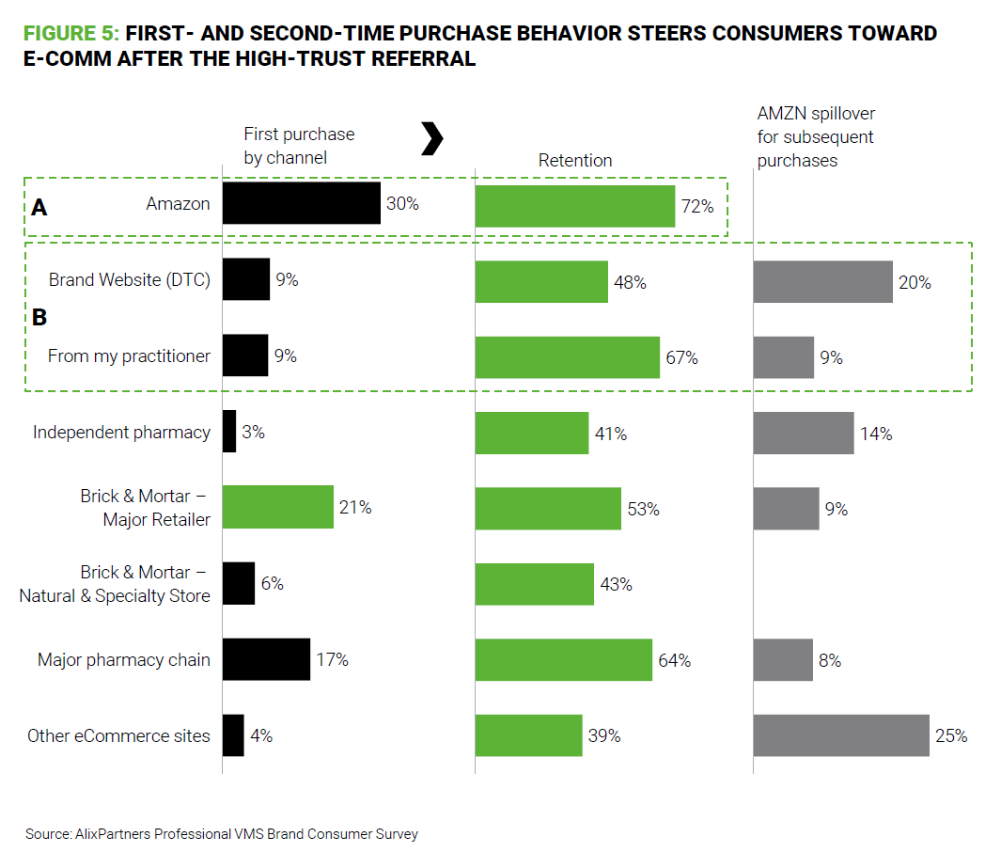

Consumers are increasingly looking to practitioners for their

initial recommendations, education, and even purchases before

switching to Amazon for continuing buys (brand websites see only

48% retention on the second buy). Vitamins, minerals, and

supplements (VMS) are on the rise both in areas where there is

sufficient research, and in new and emerging areas where product

claims overshadow quality, safety, and efficacy.

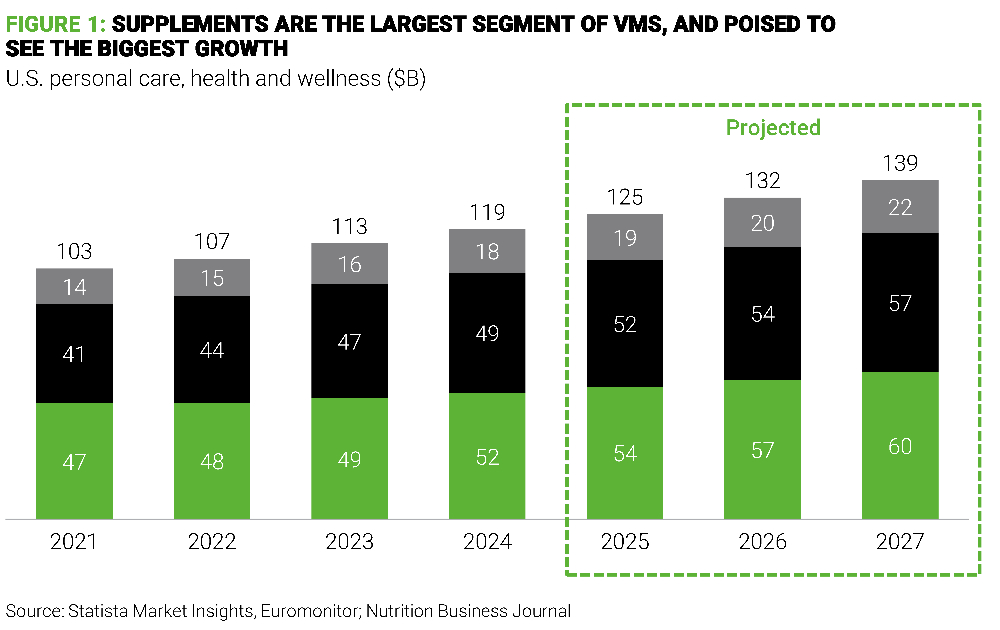

The U.S. VMS market topped $125 billion in 2025, per

Euromonitor. Active nutrition is projected to grow 11% through

2027.From changing diets to the rise of longevity

programs/products, and a deterioration in access to healthcare, a

host of conditions have combined to attack the old paradigm.

Legacy beauty and upstart producers alike will have to adapt to

the new use-case. Manufacturers and retailers will want to

capitalize on the VMS gold rush but need to adhere to the quality

and safety standards that helped overcome the previous industry

reputation of someone mixing ingredients in their garage.

Regulators may have an appetite to loosen restrictions on peptides,

which would open the door to greater adoption and growth.

More, more, and more: Why the VMS industry is changing

From the availability of consumer-level healthtech to a more

informed consumer and a blurring of the beauty/health/wellness

categories, there are a few major trends driving change in this

space.

The rise of continuous monitoring and growth of

self-directed healthcare: From Apple Watches, Whoop, and

the Oura ring to consumer-level glucose monitors from companies

like Abbott and Dexcom, healthtech has grown with the consumer desire

to be informed about their health at all times.

The growing reliance on data to make health decisions, or

self-diagnose conditions, has occurred as healthcare services have

become more expensive and harder to access—average wait times

to see a general practitioner in the U.S. are up ~20% in some cases in urban metro areas to

30 or more days, per AMN Healthcare—and have been passed over

for alternative voices. Accordingly, we’ve seen a rise in

self-treatment or doctor-directed treatment with VMS. This

isn’t limited to men or women. Both appear to have an appetite

to spend in the VMS category, although they may be targeted

differently.

Beauty and nutrition have become inextricably

linked: We keep hearing “beauty from the inside

out,” in reference to dietary impact on physical appearance

and health. VMS has capitalized on this, with companies like

Nutrafol offering capsules to treat hair loss treatment for men and

women, Thorne offering diagnostic testing complemented with

matching supplements for internal and external needs, and people

drinking lemon water and olive oil to “tighten up” and to

maintain their youthful glow.

“Beauty from the outside-in” is also fully in play as

cosmetic companies incorporate traditionally ingestible

supplements. AlixPartners research found that 85% of consumers buying holistic beauty products

want detailed ingredient information. How many skincare

routines include peptides, collagen, vitamin C, or a nutrient

additive? Go to your local Sephora or browse the shampoo aisle at

the grocery store. The secret additive that drives your desired

outcome is in everything.

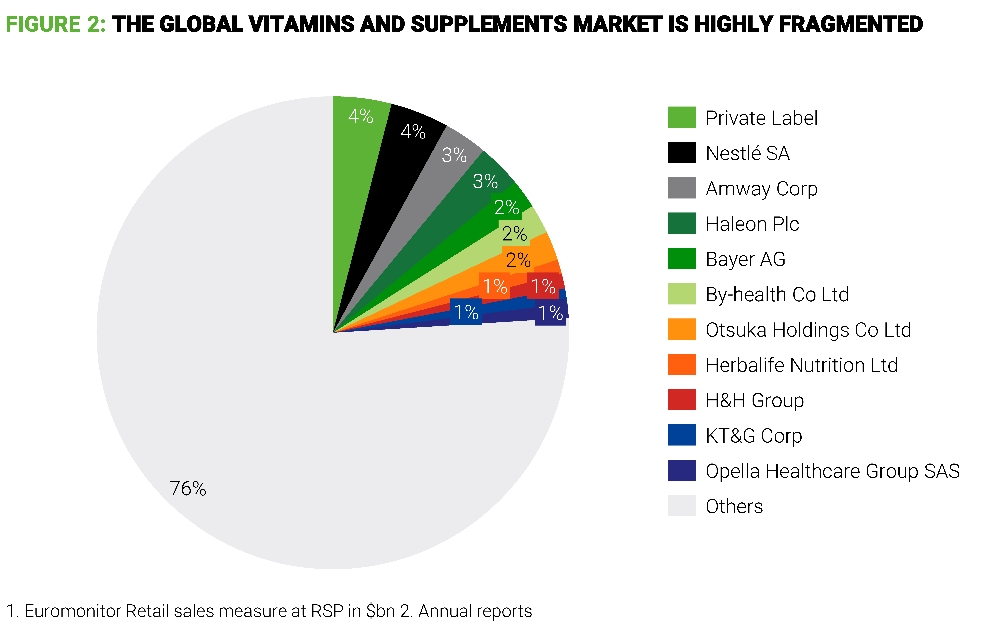

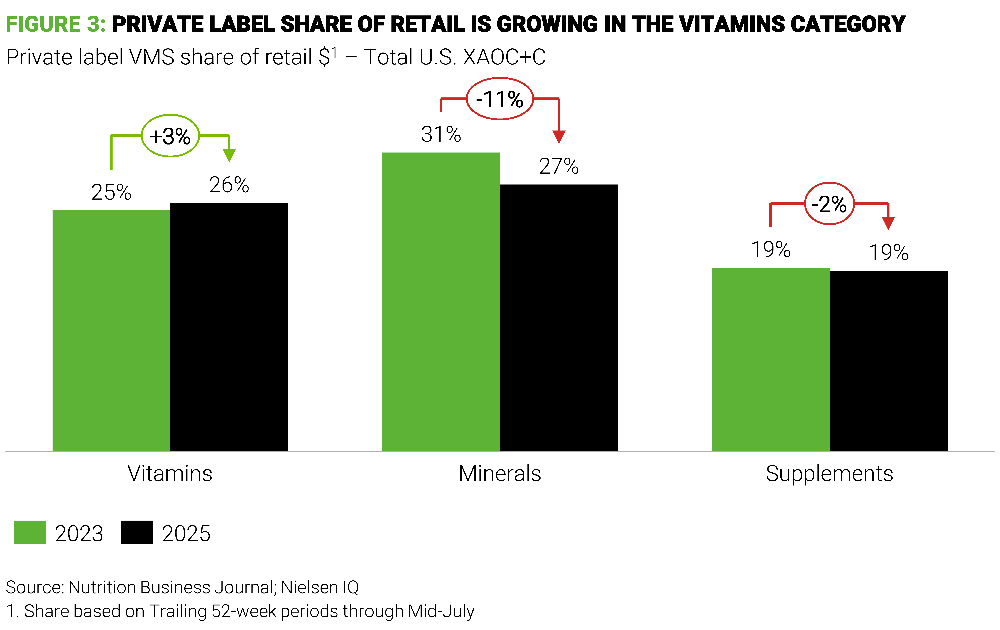

Private label is showing strength as consumers seek out

specific ingredients: As with beauty, marketing and sales

are the growth drivers in VMS. Where R&D lies and how much

spend should be allocated is more company dependent, but consumers

are always looking for a next-level product, and private label

products have more share than the largest branded products. No

company has more than a 5% share. Once booming brands that are in

decline or stagnating continue to show up in the beauty space and

private label is playing a greater role in retailers’

assortment. As small players in beauty and wellness look for

manufacturing partners, the opportunity for private label remains

huge.

Despite the appearance of endless products and brands, as the

VMS market grows, private label is responsible for a large portion

of the footprint, though it is very fragmented.

The all-in-one experience: Med spas, gyms,

wellness centers and retreats have exploded in growth. Walking around cities, it

seems like there is a consumer treatment center on every corner.

Although many specialize, there are some that look to become a

one-stop shop, from doing blood tests and writing prescriptions to

tailoring your diet and providing physical manipulation.

The retail footprint is massive. Direct-to-consumer and Amazon

are the preferred method of purchase for recurring vitamin and

supplement purchases. However, the retail footprint is massive.

Going to a location—whether a doctor or a different provider

for initial learnings—has a lot of power. Generationally,

this is huge with Gen Z, more likely to bond and socialize with

wellness activities in a sauna for R&R than spend a night out

drinking. In retail, it looks to be only a matter of time before we

see VMS products in beauty retailers and beauty products in VMS

retailers. Ulta has already started with products like Mary

Ruth.

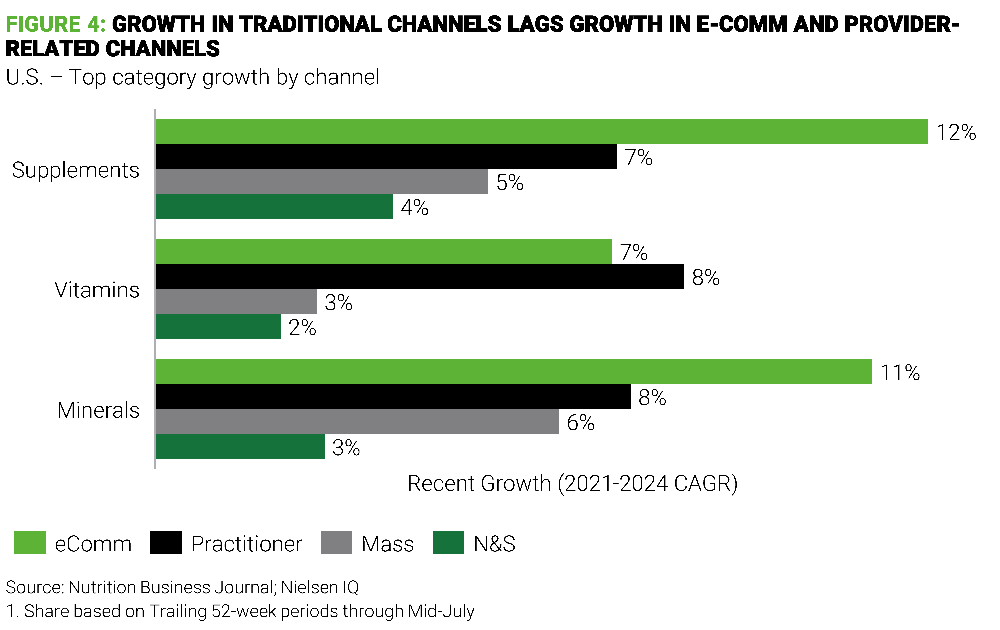

Discovery comes from providers and e-commerce

So, how can VMS manufacturers and retailers reach this

burgeoning market?

All channels are showing growth, but practitioner-related

referrals and e-commerce lead the way. As we’ve discussed,

growth in this space is driven by a desire for information about

personal health that can be put in action to fuel

self-improvement—the AlixPartners Consumer Sentiment Index

found that med spas/salons and doctors’ officers now rank #4

and #5 for specialty beauty destinations. Thus, providers’

recommendations or one of the many strains of influence (yes, even Reddit) are what convert consumers into

users of a product.

Even among consumers who receive a recommendation for a specific

VMS regimen from a healthcare provider, 92% still conduct

additional research, per AlixPartners’ professional VMS survey,

and women are twice as likely as men to continue to investigate

benefits and uses.

Once consumers have tried a product, 9% of those referred by a

provider switch to Amazon, and around 20% of those who originally

purchased via a DTC channel look to buy it from the e-commerce

giant, according to VMS survey data. There could be many drivers of

this behavior, whether it be cost, convenience, or an indication

that few brands offer the full suite of VMS products that comprise

consumers’ tailored regimens.

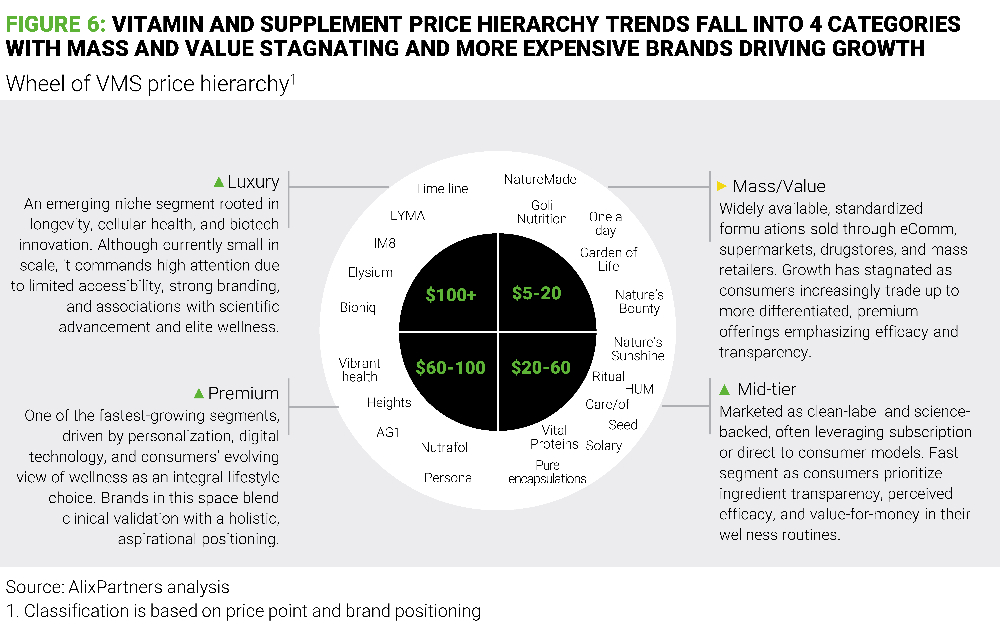

Higher-priced brands are leading the way for branded

products

To win, companies need to have the right marketing, the right

channels, the right products, and a differentiator. Across the

value chain, luxury is outperforming mass and value, due in part,

we believe, to the associations with biotech innovation,

associations with scientific advancement, and elite fan bases.

The opportunity is huge, but the product has to work

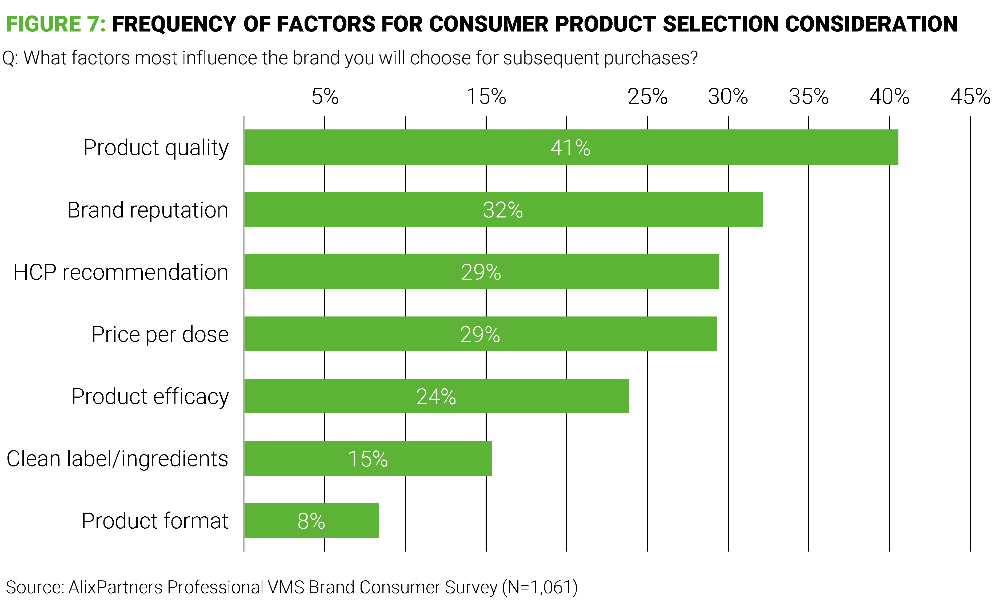

Even among consumers who are purchasing VMS products after a

recommendation from a healthcare provider, product quality and

brand reputation are the most frequently important purchase

factors. Pricing (per dose, not just per bottle) is also an

important factor for nearly a third of consumers.

As the VMS boom plays out, consumers will have a growing

opportunity to test and switch products. The winners will be the

companies selling science-backed products that provide results and

win trust.

The consumer looking for the right “stack” won’t

take their physician or trainer at their word—they will weigh

the effect of the product against pricing and brand identity.

Companies looking to outperform the competition need to:

Be deliberate and intentional in building brand, consumer,

customer and product strategies, knowing the consumer piece is

driven increasingly by practitioners and influencers.

Drive customer and consumer education, leveraging

science-backed research and maximizing value of certifications and

quality.

Optimize portfolio and make sure investments are aligned with

trends and growing brands, products, and regions.

Build efficient and quality focused operations that enable

speed to market and agility, bring operations into the 21st

Century, and balance cost with operational effectiveness.

Optimize footprint and supply chain, especially with tariff

risks and impacts and the increasing power of private

label/co-manufacturers.

Like the products their consumers are taking, companies need a

serious stack of operations improvement to capitalize on the rich

potential in front of them.

AlixPartners Professional VMS Survey conducted July

2025.

Contributors: Raj Konanahalli, Michael Bronstein, Abby Sattler,

Wyatt Puscas

The content of this article is intended to provide a general

guide to the subject matter. Specialist advice should be sought

about your specific circumstances.

Partners with Superpower on Diagnostics and Supplements")