Unilever is combining its Foods business, including Knorr and Hellmann’s, with McCormick to create a global flavour group. The deal marks a pivot for Unilever toward beauty, wellbeing, personal care, and home care as its core focus. Alongside the Foods transaction, Unilever has acquired Grüns, a US based supplements brand, to expand its health and wellness exposure.

For investors in LSE:ULVR, this move comes as the shares trade around £43.13, with a 3.4% gain over the past week but double digit declines over the past month, year, and year to date. The combination of the Foods unit with McCormick and the purchase of Grüns significantly reshapes where Unilever’s revenues may come from over time, with less reliance on traditional pantry brands.

These portfolio changes point to a clearer focus on categories tied to beauty, wellbeing, and household products, as well as science led supplements. For investors, the key questions are how efficiently Unilever executes this shift and how the market chooses to value a more focused, premium oriented consumer business.

Stay updated on the most important news stories for Unilever by adding it to your watchlist or portfolio. Alternatively, explore our Community to discover new perspectives on Unilever.

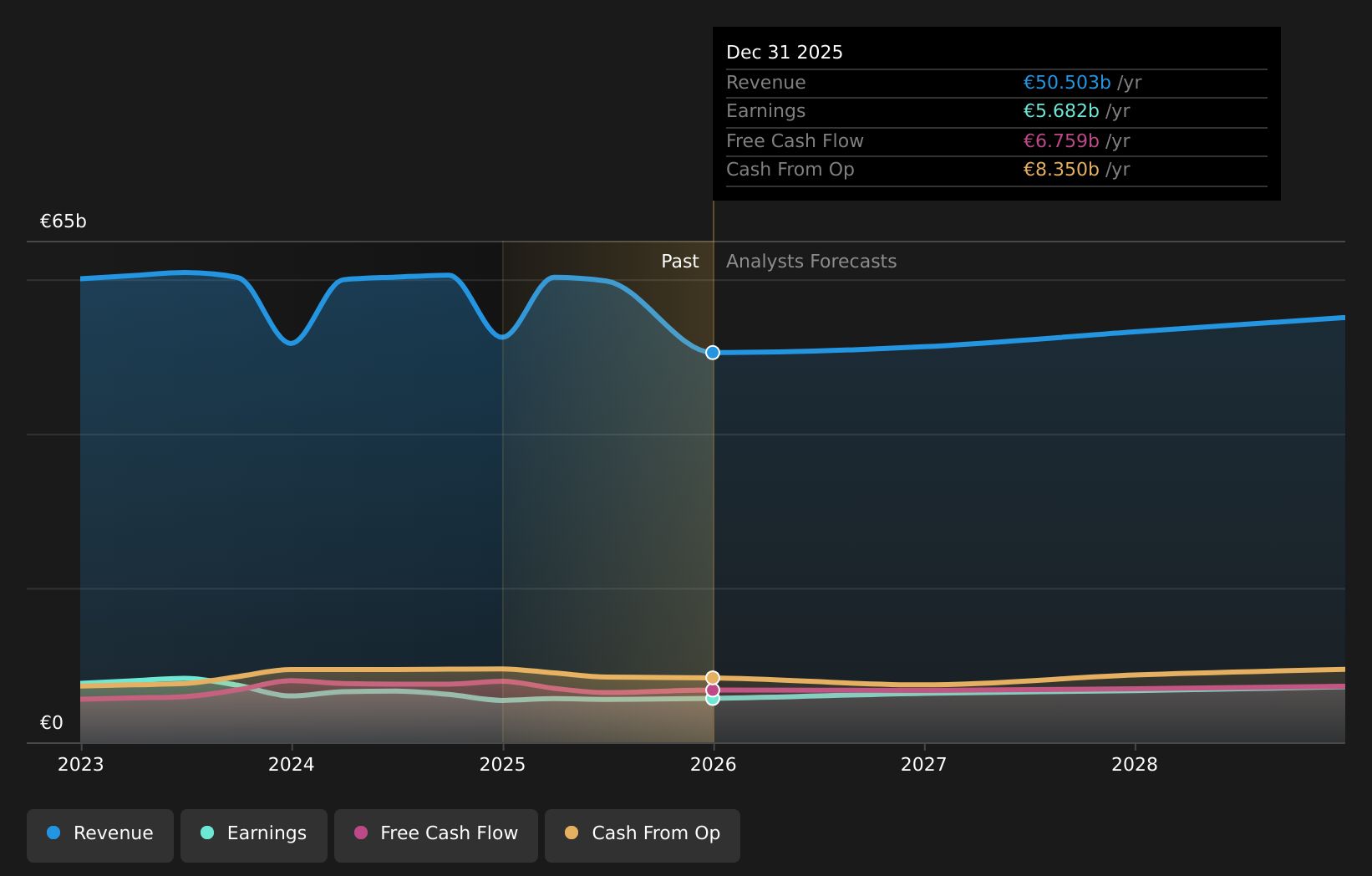

LSE:ULVR Earnings & Revenue Growth as at Apr 2026

LSE:ULVR Earnings & Revenue Growth as at Apr 2026

We’ve flagged 2 risks for Unilever. See which could impact your investment.

The McCormick combination and the Grüns purchase together give you a clearer picture of where Unilever wants its growth engines to sit. The Reverse Morris Trust deal values Unilever Foods at an EV/Sales multiple of 3.6x and 13.8x EV/EBITDA, with Unilever and its shareholders set to own 65% of the combined flavour group and receive US$15.7b in cash. Management has flagged that the cash is earmarked to cover separation costs, reduce leverage to around 2.0x net debt to EBITDA, and fund a planned €6,000m share buyback program between 2026 and 2029. At the same time, bolt on deals like Grüns and a stated focus on “super growth assets” in the US and India indicate a tilt toward premium, science led health and wellness brands. For you as an investor, the key trade off is swapping a diversified, pantry heavy portfolio for a more concentrated pure play in Beauty, Wellbeing, Personal Care and Home Care, while still retaining a sizeable equity interest in a global flavour group that competes with peers such as Nestlé and Kraft Heinz.

How This Fits Into The Unilever Narrative The Foods separation and shift toward science led supplements directly align with the narrative of focusing on premium, higher margin beauty and wellbeing categories supported by bolt on acquisitions. Relying more on health and wellness brands and emerging market premiumisation could challenge the narrative if competition from private label and local brands limits pricing power or slows expected margin improvement. The long term equity stake in the combined McCormick Foods group, and the specific US and India acquisition focus, may not be fully reflected in existing narrative assumptions about category mix and geographic exposure.

Knowing what a company is worth starts with understanding its story.

Check out one of the top narratives in the Simply Wall St Community for Unilever to help decide what it’s worth to you.

The Risks and Rewards Investors Should Consider ⚠️ Execution risk around separating a €39,000m revenue Foods business and integrating with McCormick while also reshaping the remaining portfolio could create operational disruption or cost overruns. ⚠️ A more concentrated focus on beauty, personal care and health products increases exposure to competition from players such as Procter & Gamble, L’Oréal and local digital brands, which could pressure volumes or pricing. 🎁 Retaining 65% of the combined Foods and McCormick entity and receiving US$15.7b in cash provides both ongoing exposure to a large flavour platform and financial flexibility for debt reduction and share buybacks. 🎁 Selective bolt on deals in premium, digitally native wellness and personal care brands in the US and India can deepen exposure to faster growing channels and segments that management has identified as priorities. What To Watch Going Forward

From here, keep an eye on how quickly Unilever progresses towards closing the McCormick transaction, the level and timing of the US$600m annual cost synergies targeted by year three, and any updates on regulatory approvals. It is also worth tracking how management paces the planned €6,000m buyback program and whether further US or India focused acquisitions in health and wellbeing are announced. Shareholders may want to watch for signs that the remaining pure play Home and Personal Care portfolio is gaining traction in premium and ecommerce channels, as well as how the combined flavour business performs once Unilever stops consolidating its Foods earnings.

To ensure you’re always in the loop on how the latest news impacts the investment narrative for Unilever, head to the

community page for Unilever to never miss an update on the top community narratives.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com