Find winning stocks in any market cycle. Join 7 million investors using Simply Wall St’s investing ideas for FREE.

Danone (ENXTPA:BN) is reportedly weighing an acquisition of infant-formula producer Mead Johnson.

The discussions follow Danone’s recently agreed purchase of plant-based nutrition brand Huel.

Together, the potential Mead Johnson deal and the Huel acquisition would broaden Danone’s presence in specialized nutrition.

Danone’s share price currently stands at €69.18, with a value score of 3 and a 5 year return of 37.2%. For readers tracking larger consumer staples groups, ENXTPA:BN is positioning itself across both plant-based and infant nutrition, areas that are closely linked to long term consumer consumption patterns.

If Danone proceeds with a bid for Mead Johnson, this would reflect a company leaning further into branded nutrition categories rather than purely traditional dairy. Future updates on deal terms, integration plans with Huel and any comments on capital allocation will be important checkpoints for assessing how this affects the balance of risk and opportunity for shareholders.

Stay updated on the most important news stories for Danone by adding it to your watchlist or portfolio. Alternatively, explore our Community to discover new perspectives on Danone.

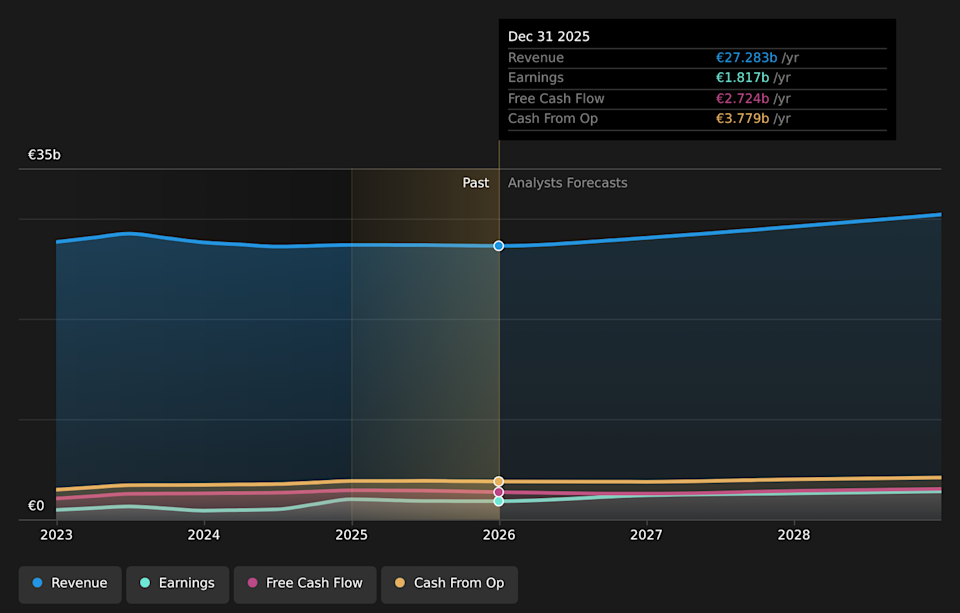

ENXTPA:BN Earnings & Revenue Growth as at Apr 2026

ENXTPA:BN Earnings & Revenue Growth as at Apr 2026

We’ve flagged 2 risks for Danone. See which could impact your investment.

The potential Mead Johnson acquisition would sit alongside Huel and Danone’s existing specialized-nutrition portfolio, giving the group a broader reach across infant, medical, and plant-based nutrition. For readers, the key question is whether the extra scale and brand depth in infant formula, particularly in the US, would compensate for the legal and regulatory issues that have followed Mead Johnson under Reckitt’s ownership. Recent fixed-income offerings of €700 million, €500 million and about £350 million show that Danone is active in term funding, which could support larger deals but also adds to future interest commitments. Compared with peers like Nestlé and Abbott in infant and medical nutrition, and Unilever in broader consumer staples, this move would signal a clearer tilt toward branded nutrition categories rather than commodity dairy and water. The payoff would depend on the price paid, how Danone handles Mead Johnson’s litigation exposure, and whether management can integrate Huel, Mead Johnson and existing assets without distraction from ongoing efficiency and portfolio work.

The reported interest in Mead Johnson and the Huel deal lines up with the narrative of building out health-driven and specialized-nutrition categories that can support premium products and resilience.

Layering another large acquisition on top of recent deals could increase integration complexity and execution risk, which the narrative already flags as a potential drag on margins if not managed carefully.

The specific litigation and regulatory issues around Mead Johnson, especially in infant formula, do not feature directly in the existing narrative and could be an extra factor for investors to weigh.

Knowing what a company is worth starts with understanding its story. Check out one of the top narratives in the Simply Wall St Community for Danone to help decide what it’s worth to you.

⚠️ Taking on Mead Johnson could introduce higher legal and regulatory risk linked to historic issues in the infant-formula segment.

⚠️ Additional debt-funded deals on top of recent bond issues may leave Danone with less flexibility if trading conditions or integration progress become challenging.

🎁 A broader footprint in infant and complete nutrition could deepen Danone’s presence in categories where brand strength and specialized products often support pricing power.

🎁 Combining Huel, existing medical-nutrition assets and a possible Mead Johnson acquisition could create cross-selling and product-extension opportunities across multiple channels.

Investors will want to track whether Danone confirms formal negotiations with Reckitt, the headline valuation for any Mead Johnson deal, and how management plans to fund it given the recent bond issues. Clear disclosure on Mead Johnson’s litigation profile and any indemnities from Reckitt would be important for assessing downside risk. Updates on integration plans for Huel and how these acquisitions sit alongside Danone’s yogurt and dairy priorities will also matter, especially versus competitors like Nestlé, Abbott and Unilever. If management provides medium term financial targets that incorporate potential M&A, that could help you judge whether the group’s growing focus on specialized nutrition aligns with your own expectations for risk and return.

To ensure you’re always in the loop on how the latest news impacts the investment narrative for Danone, head to the community page for Danone to never miss an update on the top community narratives.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include BN.PA.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com