Valuation After Recent Share Price Weakness")

Why Planet Fitness Stock Is On Investors’ Radar

Planet Fitness (PLNT) has been drawing attention after recent share price pressure, with the stock showing negative returns over the past month, past 3 months and year. That backdrop is prompting closer scrutiny of the gym operator’s fundamentals.

See our latest analysis for Planet Fitness.

The recent pressure on Planet Fitness’ share price, including a 2.78% one day share price return decline and a 35.84% year to date share price return decline to US$70.40, reflects fading momentum after a year in which total shareholder return also declined 27.82%.

If this pullback has you reassessing the gym space, it can help to widen the search and see what else is moving by scanning 18 top founder-led companies

With Planet Fitness shares under pressure, yet trading at what some models flag as a discount to intrinsic value and analyst targets, you have to ask: is this a reset worth considering, or is the market already pricing in future growth?

Most Popular Narrative: 37.2% Undervalued

With Planet Fitness last closing at $70.40 against a narrative fair value of about $112.06, the current share price sits well below that framework, which leans heavily on membership expansion and margin assumptions.

Ongoing format optimization, with more strength equipment, redesigned layouts, and attention to user preference, is increasing club utilization and member satisfaction. This may support improved retention and create opportunities for pricing power, which in turn could affect both revenue and net margins.

Want to see what sits behind that pricing power story? The narrative focuses on a particular mix of revenue trends, margin shifts and future earnings multiples. Curious which assumptions really move the fair value?

Result: Fair Value of $112.06 (UNDERVALUED)

Have a read of the narrative in full and understand what’s behind the forecasts.

However, that upside case runs into real friction if higher member attrition from click to cancel and tougher competition begin to affect membership and pricing assumptions.

Find out about the key risks to this Planet Fitness narrative.

Another Way To Look At Valuation

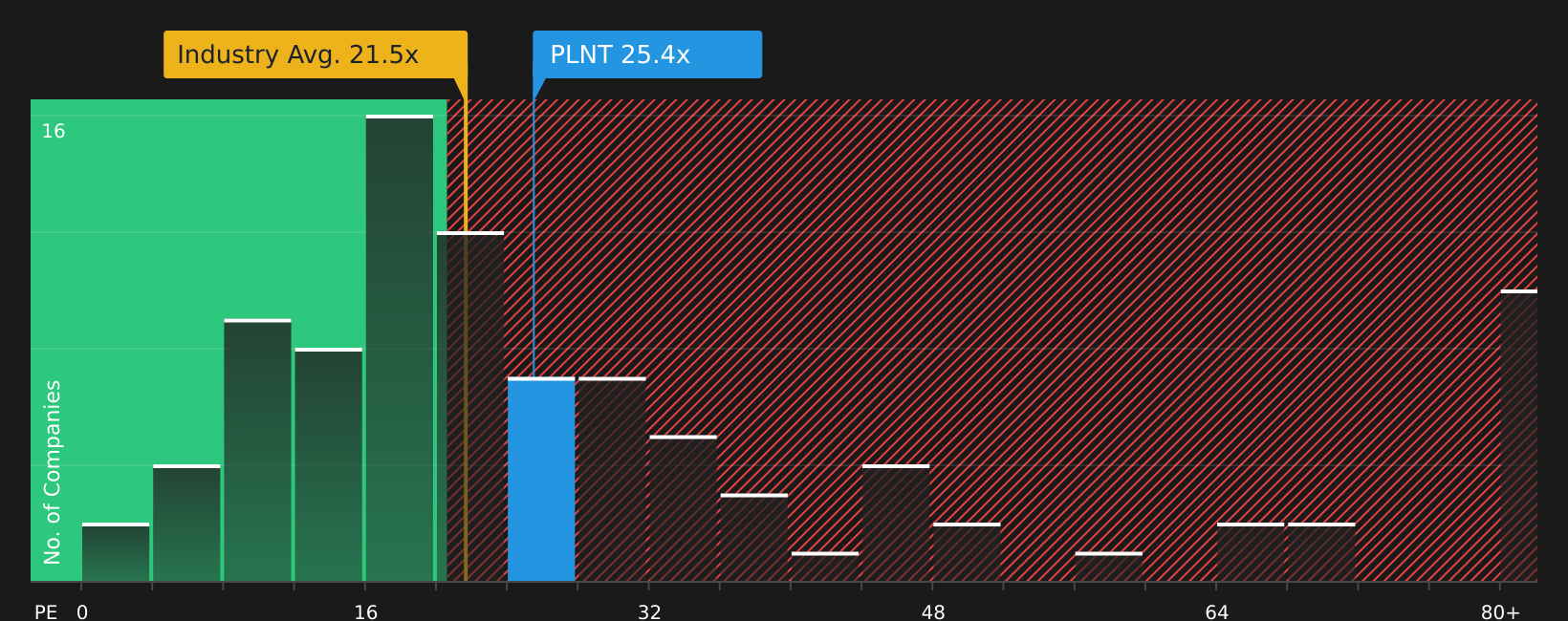

The narrative fair value of $112.06 suggests upside, but the current P/E of 25.4x sits above the US Hospitality industry at 21.5x, the peer average at 23.4x, and even an estimated fair ratio of 22.8x. That richer multiple can mean less room for error if growth expectations soften.

To see what the numbers say about this price and how that higher P/E could affect your margin of safety, See what the numbers say about this price — find out in our valuation breakdown.

NYSE:PLNT P/E Ratio as at Apr 2026Next Steps

NYSE:PLNT P/E Ratio as at Apr 2026Next Steps

With sentiment pulling in both directions, it is worth checking the data yourself and deciding where you stand before the market moves on. To get a balanced view of the potential upside and the concerns already on investors’ minds, take a closer look at the 3 key rewards and 2 important warning signs

Ready To Hunt For Your Next Idea?

If Planet Fitness has you thinking more carefully about price, quality and risk, do not stop here. Put the same discipline to work across other opportunities.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We’ve created the ultimate portfolio companion for stock investors, and it’s free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com