Investment Story Is Shifting With New Data And Valuation Cuts")

Make better investment decisions with Simply Wall St’s easy, visual tools that give you a competitive edge.

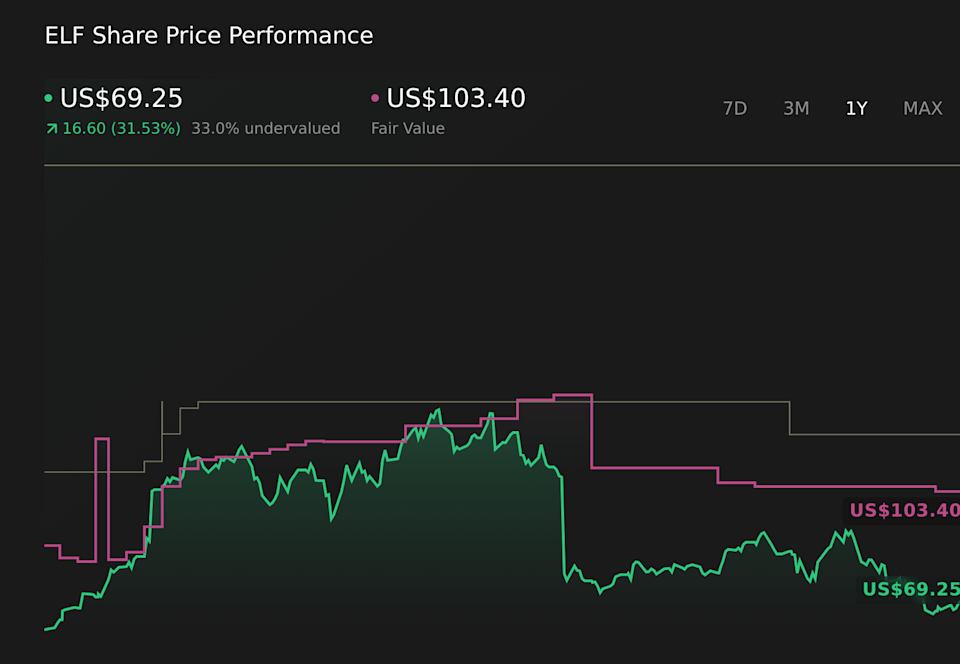

e.l.f. Beauty is under fresh scrutiny as the updated fair value estimate has shifted from US$111.71 to US$103.40, a reduction of about 7% that resets expectations around the stock. This change reflects a mix of more cautious price targets, including cuts of US$10 to US$32 in recent reports, alongside more upbeat views that point to revised February data and steady category trends. As you read on, you will see how these conflicting takes shape the evolving analyst narrative and what to watch next.

Piper Sandler points to corrected February data showing Elf consumption at 6% through February 22 and Q4 to date at 7%, which it views as broadly in line with the prior quarter, and keeps a Neutral stance rather than moving to a more negative view.

Piper Sandler also highlights that the U.S. mass cosmetics market was up low single digit in February, with Q4 to date slightly ahead of the prior quarter, which supports the idea that Elf is operating in a category with steady demand.

Several firms, including JPMorgan, Citi, BofA, UBS, Deutsche Bank, Canaccord, and TD Cowen, have recently cut Elf Beauty price targets, with reductions ranging from US$10 to US$32, which has filtered through into a lower aggregated fair value estimate.

Piper Sandler flags that February consumption data slowed to flat versus January and that volume moved to roughly a 10% decline, and it indicates that an acceleration from low single digit growth in the core business is important for the stock.

Evercore ISI and Piper Sandler are both sitting at Neutral, which signals a more cautious stance on execution and growth at current valuation levels compared with earlier bullish initiations from firms such as Citi.

Do your thoughts align with the Bull or Bear Analysts? Perhaps you think there’s more to the story. Head to the Simply Wall St Community to discover more perspectives!

NYSE:ELF 1-Year Stock Price Chart

NYSE:ELF 1-Year Stock Price Chart

We’ve flagged 1 risk for e.l.f. Beauty. See which could impact your investment.

e.l.f. Beauty raised its fiscal 2026 net sales guidance to a range of US$1.6b to US$1.612b, compared with prior guidance of US$1.55b to US$1.57b. This was framed as a 22% to 23% year over year increase versus a previously expected 18% to 20% increase.

From October 1, 2025 to December 31, 2025, the company repurchased 626,049 shares for US$49.98m, described as 1.05% of shares outstanding.

Under the August 27, 2024 buyback authorization, e.l.f. Beauty has repurchased a total of 1,587,303 shares for US$100.53m, or 2.76% of shares, and has completed that program.

Story Continues

The fair value estimate moved from US$111.71 to US$103.40, a reduction of about 7%.

The long-term revenue growth assumption shifted from 12.76% to 12.68%.

The assumed net profit margin was adjusted from 9.36% to 9.38%.

The future P/E multiple moved from 46.10x to 43.03x.

The discount rate changed from 7.38% to 7.69%.

Narratives connect a company’s business story to specific forecasts and a fair value estimate, so you can see how assumptions line up with the numbers. They update as new guidance, deals, and risks come through.

Head over to the Simply Wall St Community and follow the Narrative on e.l.f. Beauty to stay up to date on:

How international expansion, including 30% international net sales growth and a broader Sephora rollout, is shaping the growth story and geographic mix.

What the Rhode acquisition and e.l.f. Beauty’s use of influencer marketing, social media, and new product launches could mean for future brand reach and margins.

Key risks around heavy reliance on Chinese manufacturing, tariff exposure, elevated marketing and SG&A, and rising competition in affordable, clean beauty.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include ELF.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com