Is Down 9.4% After Soft 2026 Guidance And Rising Churn Concerns")

In late February 2026, Planet Fitness reported higher fourth-quarter and full-year 2025 revenue and earnings, then issued 2026 guidance calling for approximately 9% revenue growth and 4–5% same-store sales growth, alongside plans for continued club expansion including new franchise locations in northern Mexico.

The guidance, which fell short of analysts’ prior expectations and was followed by securities-fraud investigations and commentary about choppy member trends and higher churn, has prompted fresh questions about how Planet Fitness balances membership growth, pricing, and international expansion within its franchise-heavy model.

Next, we’ll examine how the softer 2026 revenue outlook, alongside rising churn concerns, may reshape Planet Fitness’s longer-term investment narrative.

This technology could replace computers: discover 22 stocks that are working to make quantum computing a reality.

To own Planet Fitness, you need to believe its low-cost, franchise-led model can keep growing memberships and clubs while managing higher churn from easier cancellations. Right now, the key near-term catalyst is whether 2026 performance meets the 9% revenue and 4–5% same-store sales guidance. The biggest risk is that elevated attrition and “choppy” member trends linger. The latest guidance and ensuing investigations appear to make that churn risk more immediate, rather than changing it entirely.

The Mexico expansion announcement stands out here. Adding new franchise locations in Tijuana and Mexicali supports the growth story and helps diversify beyond a maturing U.S. footprint. With about 20.8 million members and nearly 2,900 clubs at year-end 2025, further international growth could offset some pressure from softer U.S. member trends, but it does not directly solve concerns about rising churn or the impact of click-to-cancel on recurring revenue.

Yet, even as Planet Fitness leans into expansion, investors should be aware that…

Read the full narrative on Planet Fitness (it’s free!)

Planet Fitness’ narrative projects $1.6 billion revenue and $312.8 million earnings by 2028.

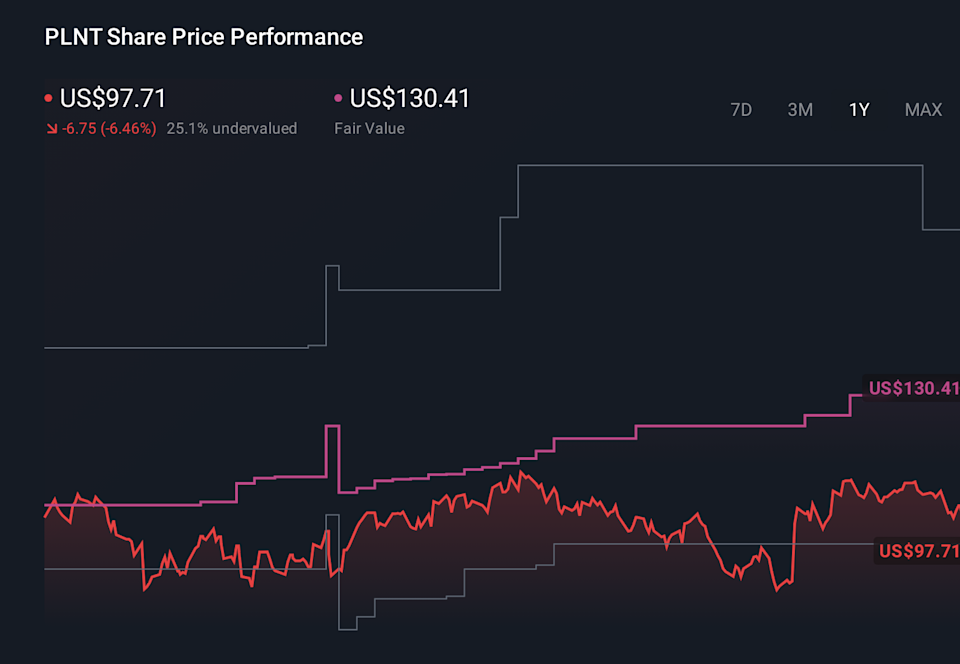

Uncover how Planet Fitness’ forecasts yield a $130.00 fair value, a 58% upside to its current price.

PLNT 1-Year Stock Price Chart

PLNT 1-Year Stock Price Chart

Before this guidance, the most pessimistic analysts were already cautious, expecting revenue of about US$1.6 billion by 2028 and needing a rich 38.2x PE, so if higher churn from easier cancellations persists after the softer 9% 2026 outlook, that more downbeat view could gain traction and you should weigh it against more optimistic membership growth stories.

Explore 3 other fair value estimates on Planet Fitness – why the stock might be worth less than half the current price!

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

The market won’t wait. These fast-moving stocks are hot now. Grab the list before they run:

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include PLNT.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Valuation After Weak Earnings And Lower 2026 Revenue Guidance")

Is Down 9.4% After Tempered 2026 Guidance Despite Strong 2025 Results")