Margins Improve Despite Same Store Sales Decline")

Petco Health and Wellness Company (WOOF) has reported fourth quarter FY 2026 revenue of US$1.5 billion with basic EPS of roughly US$0.01 loss and net income loss of US$2.6 million, while same store sales showed a 1.6% decline. Over recent quarters, revenue has moved between US$1.5 billion and US$1.6 billion as basic EPS ranged from a loss of about US$0.06 in Q4 FY 2025 to a profit of roughly US$0.05 in Q2 FY 2026, with trailing twelve month EPS at US$0.03 on net income of US$9.1 million. That mix of modest profitability on a large sales base directs investor attention to margins and to how durable any earnings recovery might be.

See our full analysis for Petco Health and Wellness Company.

With the latest numbers on the table, the next step is to set these results against the widely held narratives around Petco to see which storylines the figures support and which they call into question.

See what the community is saying about Petco Health and Wellness Company

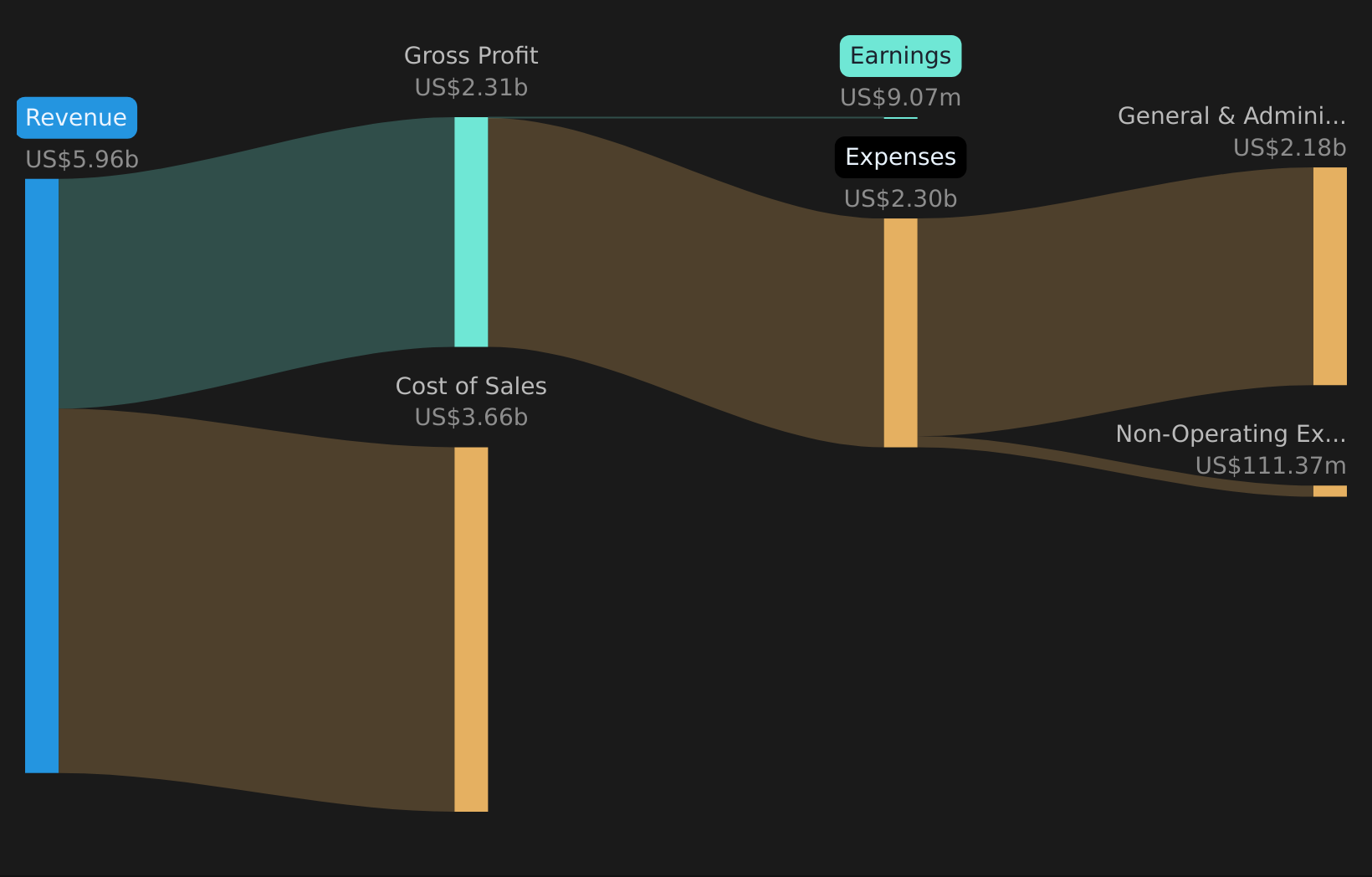

NasdaqGS:WOOF Revenue & Expenses Breakdown as at Mar 2026 Margins improving on low same store sales Trailing twelve month net income moved to a US$9.1 million profit on US$6.0b of revenue, even though same store sales in Q4 showed a 1.6% decline and comparable sales across FY 2026 quarters ranged from a 1.3% to 2.2% decline. Bulls argue Petco’s focus on higher margin services and premium products can support this kind of profit on a flat top line. However, the recent quarterly same store sales declines put pressure on that view.

NasdaqGS:WOOF Revenue & Expenses Breakdown as at Mar 2026 Margins improving on low same store sales Trailing twelve month net income moved to a US$9.1 million profit on US$6.0b of revenue, even though same store sales in Q4 showed a 1.6% decline and comparable sales across FY 2026 quarters ranged from a 1.3% to 2.2% decline. Bulls argue Petco’s focus on higher margin services and premium products can support this kind of profit on a flat top line. However, the recent quarterly same store sales declines put pressure on that view.

On the bullish side, the narrative highlights wellness services and premium assortments as potential drivers of higher margins and recurring revenue, which fits with the company being modestly profitable over the last twelve months on roughly US$6.0b of sales. At the same time, the run of negative same store sales figures in FY 2026 suggests traffic and ticket size are not yet reflecting that bullish ramp, so the margin story is working off a relatively soft sales base. Over the past year, bulls have pointed to Petco’s service mix as a profit engine, but these Q4 numbers show that earnings are being earned against declining store level volume, which makes the bullish path more dependent on mix and cost control than on broad sales growth. 🐂 Petco Health and Wellness Company Bull Case High trailing P/E versus thin earnings base With trailing EPS at US$0.03 and a current share price of US$3.23, the trailing P/E of about 100x sits well above both the US Specialty Retail industry at 18.2x and a peer average of 11.3x. Bears point to this gap and argue that even after the move into profitability, the valuation leaves little room if earnings or revenue slip.

The bearish narrative highlights ongoing sales pressure and e commerce weaknesses, and the latest quarterly data show revenue moving in a relatively tight US$1.5b to US$1.6b range with negative same store sales, which fits the concern that revenue momentum is limited. Given that TTM net income is only US$9.1 million, any setback in margins or sales mix would have a direct impact on EPS, which is what makes a P/E of around 100x a focal point for more cautious investors. If you are weighing the cautious view, the combination of a rich P/E on a small profit pool and soft store trends is exactly what skeptics are focused on right now. 🐻 Petco Health and Wellness Company Bear Case DCF fair value and modest revenue outlook The provided DCF fair value of US$5.93 sits well above the current US$3.23 share price. Revenue in the supplied forecasts is expected to grow around 0.8% per year, which is below the 10.4% forecast for the broader US market. Consensus narrative sees Petco’s wellness services, loyalty programs, and omnichannel efforts as the bridge between this modest revenue outlook and the higher DCF fair value. Yet the latest reported revenue and same store sales trends show that this bridge still relies heavily on execution.

Analysts in the provided data are looking for earnings growth of about 46.9% per year, which assumes further margin improvement off the current US$9.1 million TTM profit even though top line growth expectations are relatively low. The tension for investors is that the DCF fair value and strong earnings growth forecasts both lean on Petco turning these wellness and omnichannel initiatives into higher profitability while also managing interest expense, which the risk summary flags as not well covered by current earnings. Next Steps

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for Petco Health and Wellness Company on Simply Wall St. Add the company to your watchlist or portfolio so you’ll be alerted when the story evolves.

If this mix of bullish and cautious signals feels finely balanced, it is worth checking the full picture yourself and acting while the data is fresh. To see how the current upside and downside stack up, take a look at the 3 key rewards and 1 important warning sign that investors are watching most closely.

See What Else Is Out There

Petco’s thin US$9.1 million profit, 1.6% same store sales decline, and roughly 100x P/E all point to earnings quality and valuation pressure.

If those tight margins and a rich valuation make you uneasy, it could be worth checking out 47 high quality undervalued stocks that pair stronger earnings support with more grounded pricing.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We’ve created the ultimate portfolio companion for stock investors, and it’s free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com