Ulta’s stock price fell after issuing a cautious full-year earnings guidance, citing concerns that the conflict in the Middle East may put pressure on consumer spending.

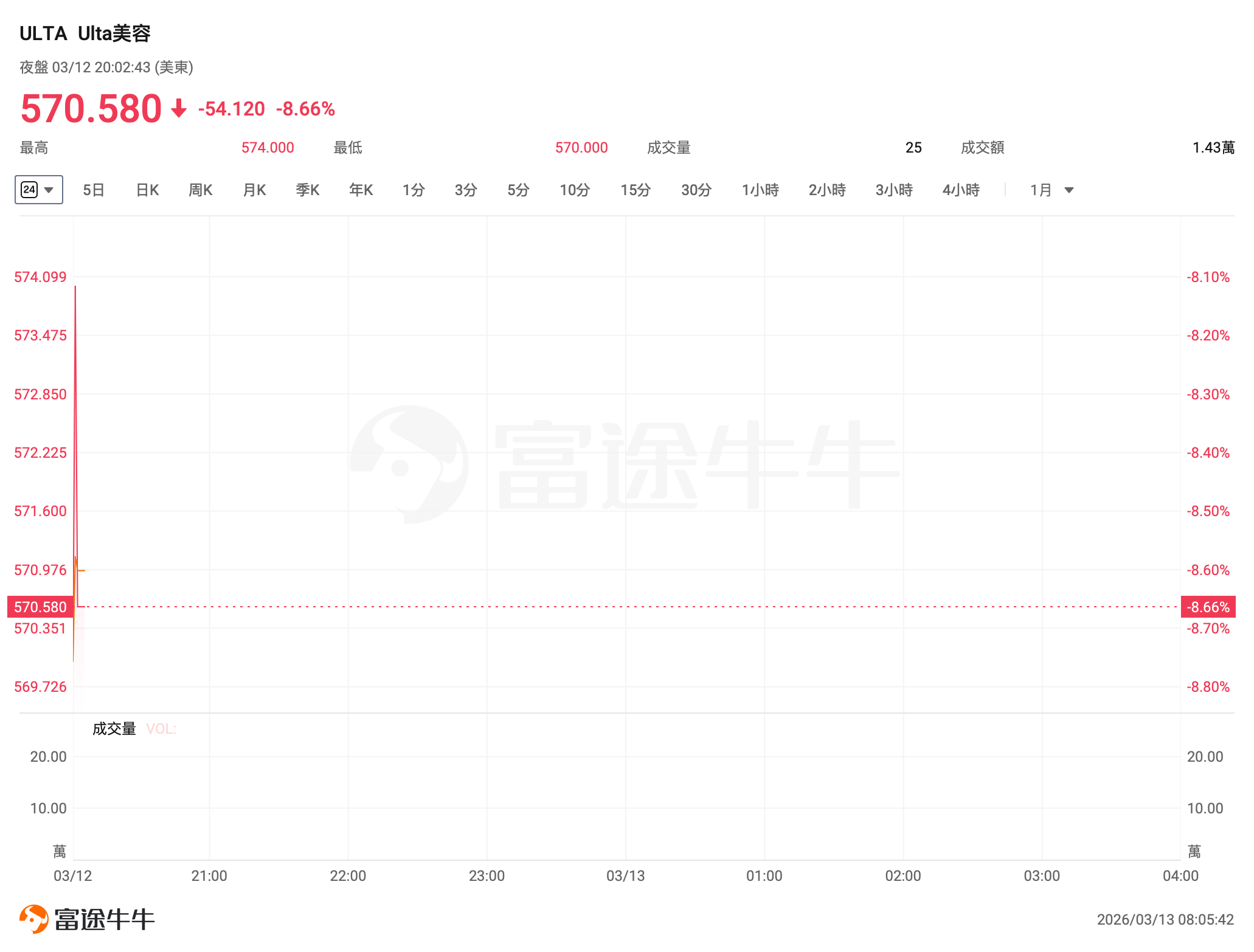

Cosmetics retailer $Ulta Beauty (ULTA.US)$ continues to maintain robust same-store sales growth and better-than-expected net sales. However, weaker-than-expected fourth-quarter profits and a soft earnings outlook for fiscal year 2026 disappointed investors. As of this writing, the stock fell more than 8% in after-hours trading.

In the fourth quarter, revenue performance remained outstanding due to the success of its Beauty Unleashed strategy, growth in same-store sales, and the acquisition of Space NK. Fourth-quarter net sales increased by 11.8% to $3.9 billion, surpassing consensus expectations, while same-store sales grew by 5.8%, higher than the 1.5% increase in Q4 2024 and above the expected growth of 4.25%. However, earnings per share (EPS) were $8.01, down from $8.46 in the same period last year and 2 cents below Wall Street’s expectations.

The company’s annual guidance announced was below Wall Street’s expectations. According to the company’s statement, same-store sales (a measure of revenue from online and physical stores that have been open for at least a year) are expected to grow between 2.5% and 3.5% this year, with the midpoint being lower than the average analyst forecast of 3.5%. The midpoint of EPS is also slightly below the average expectation—forecasted to be between $28.05 and $28.55, with a midpoint of $28.30, which is lower than the consensus expectation of $28.58.

The company’s annual guidance announced was below Wall Street’s expectations. According to the company’s statement, same-store sales (a measure of revenue from online and physical stores that have been open for at least a year) are expected to grow between 2.5% and 3.5% this year, with the midpoint being lower than the average analyst forecast of 3.5%. The midpoint of EPS is also slightly below the average expectation—forecasted to be between $28.05 and $28.55, with a midpoint of $28.30, which is lower than the consensus expectation of $28.58.

The company stated that its gross profit as a percentage of net sales slightly declined due to reduced fixed costs and revenue, but this was offset by lower inventory shrinkage and improved supply chain efficiency. Gross profit as a percentage of sales dropped by 10 basis points to 38.1%, while its operating margin decreased from 14.8% a year ago to 12.2%.

Under the leadership of CEO Kecia Steelman, this cosmetics chain achieved robust revenue growth and expanded into regions such as the Middle East. However, the outlook indicates that Ulta is adopting a cautious stance amid escalating geopolitical instability and persistent cost pressures.

In the U.S., demand for cosmetics remains strong. Ulta’s extensive product portfolio, ranging from mass-market to premium offerings, has attracted a wide range of consumers. To appeal to younger and more affluent customers, Ulta relies on celebrity-owned premium brands, such as Beyoncé’s Cecred hair care line and Rihanna’s Fenty Skin Body, while also launching holiday campaigns featuring Khloé Kardashian and Paris Hilton.

However, the market is filled with uncertainty. Escalating tensions in the Middle East have led to surging energy prices and disrupted global shipping, raising concerns about economic pressure on consumers. American consumers are already grappling with inflation. Particularly, middle- and low-income consumers have been cutting discretionary spending, allocating more of their strained budgets to daily necessities such as groceries.

Last month, Estee Lauder (EL.US) forecasted that its annual profit would fall below expectations due to weak demand in the Americas market and ongoing reforms under its new CEO, who is focusing on increasing investment and marketing efforts for higher-priced products.

Ulta also faces fierce competition from $Target (TGT.US)$ 、 $Walmart (WMT.US)$ — these large retailers are expanding their beauty product lines and capitalizing on the surging demand for Korean beauty products.

Ethan Feller, equity strategist at Zacks Investment Research, stated: ‘Ulta Beauty’s position as a leading specialty beauty retailer is undeniable. However, Sephora, Amazon, and an increasing number of direct-to-consumer brands are competing for the same consumer wallets. Even in a leadership position, when valuations are too high relative to growth prospects, repeated stock price declines cannot be avoided.’