After The Recent Share Price Surge")

This article examines whether Petco Health and Wellness Company, at around US$3.62, may represent a bargain or a value trap by exploring what the current share price might indicate about the business. The stock has recently experienced sharp moves, with returns of 52.1% over the last 7 days, 44.2% over the last 30 days, 27.0% year to date and 51.5% over the last year. However, the 3 year and 5 year returns show declines of 63.1% and 84.4%, which tells a very different story. These swings have occurred as investors continue to reassess the company after a prolonged period of weak longer term returns. While there has not been a single headline event driving this specific move based on the information provided here, the contrast between recent strength and multi year declines remains front of mind for many shareholders. Simply Wall St currently gives Petco Health and Wellness Company a valuation score of 2 out of 6, which reflects how many of its checks suggest the stock is undervalued. Next, we will look at the usual valuation approaches and then finish with a way to assess value that brings all the pieces together.

Petco Health and Wellness Company scores just 2/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Petco Health and Wellness Company Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model takes the cash a business is expected to generate in the future, then discounts those amounts back to what they might be worth in today’s dollars. It is essentially asking what the stream of future cash flows could be worth if you had them now.

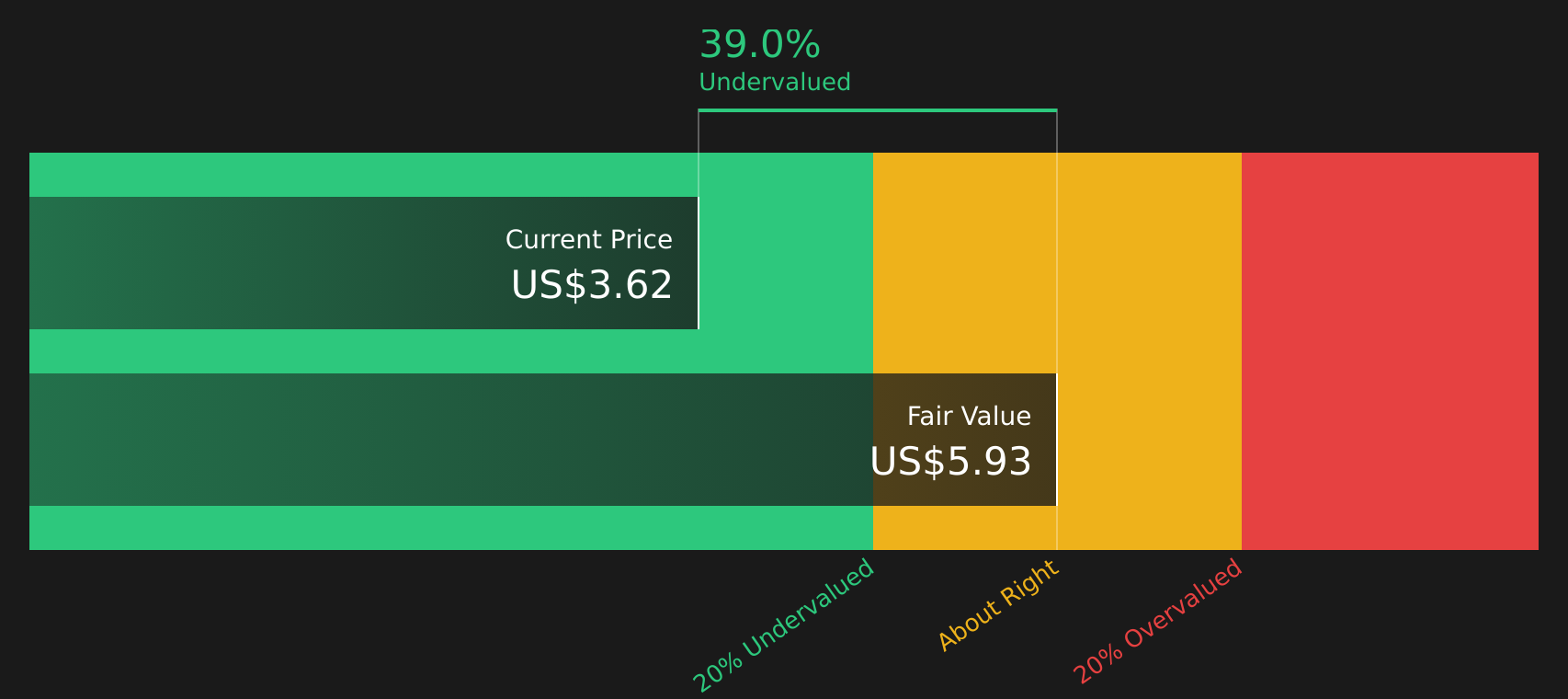

For Petco Health and Wellness Company, the model used is a 2 Stage Free Cash Flow to Equity approach, based on cash flows available to shareholders. The latest twelve month Free Cash Flow is about $157.5 million. Analysts provide explicit annual Free Cash Flow projections up to 2031, with estimates such as $191 million in 2031. Simply Wall St then extrapolates cash flows beyond the analyst horizon using modest growth assumptions.

After discounting these projected cash flows to today, the model arrives at an estimated intrinsic value of about $5.93 per share. Compared with a recent share price around $3.62, this DCF suggests the stock is trading at roughly a 39.0% discount. On this measure alone, the shares appear to be priced below the model’s estimate of intrinsic value.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Petco Health and Wellness Company is undervalued by 39.0%. Track this in your watchlist or portfolio, or discover 48 more high quality undervalued stocks.

WOOF Discounted Cash Flow as at Mar 2026

WOOF Discounted Cash Flow as at Mar 2026

Approach 2: Petco Health and Wellness Company Price vs Earnings

For companies that are generating earnings, the P/E ratio is a straightforward way to think about value, because it links what you pay for each share to the profits the business is currently producing.

In general, higher growth expectations and lower perceived risk can support a higher P/E ratio, while slower growth and higher risk usually justify a lower multiple. So what counts as a “normal” or “fair” P/E will vary across companies and industries.

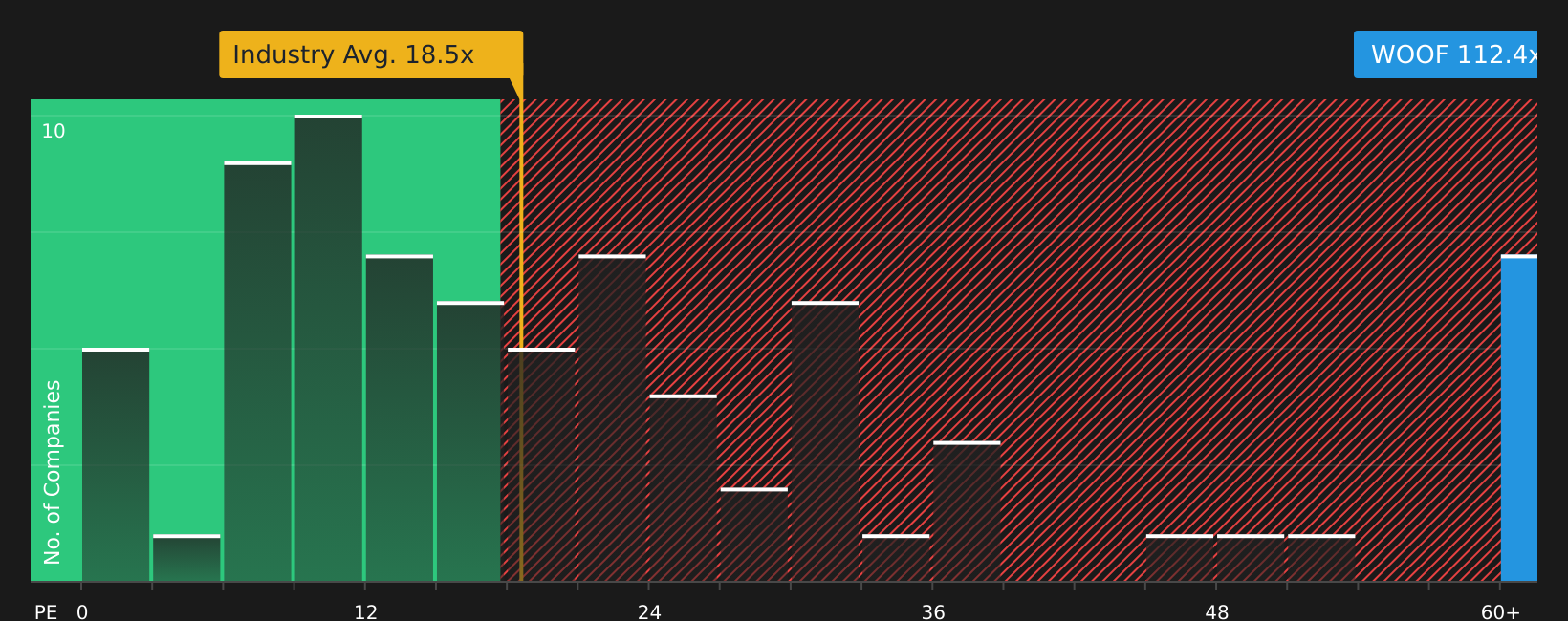

Petco Health and Wellness Company is trading on a P/E of about 112.40x, compared with a Specialty Retail industry average of about 18.49x and a peer average around 17.72x. Simply Wall St also calculates a proprietary “Fair Ratio” of 39.97x. This represents the P/E level their model suggests could be appropriate given factors such as earnings growth, industry, profit margins, market cap and risk profile.

This Fair Ratio can be more informative than a simple comparison with industry or peer averages, because it adjusts for the specific characteristics and risk factors of Petco Health and Wellness Company rather than treating all retailers as identical.

Comparing the current P/E of 112.40x with the Fair Ratio of 39.97x, the shares look expensive on this measure.

Result: OVERVALUED

NasdaqGS:WOOF P/E Ratio as at Mar 2026

NasdaqGS:WOOF P/E Ratio as at Mar 2026

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 19 top founder-led companies.

Upgrade Your Decision Making: Choose your Petco Health and Wellness Company Narrative

Earlier we mentioned that there is an even better way to think about valuation, so let us introduce you to Narratives. Narratives let you attach a clear story to the numbers by linking your view on Petco Health and Wellness Company’s future revenue, earnings and margins to a forecast and then to a fair value, all within an easy tool on Simply Wall St’s Community page. The tool updates automatically when new news or earnings arrive and helps you decide what to do by comparing your Fair Value to the current share price, whether you lean toward a cautious view closer to the US$2.72 bearish fair value or a more optimistic view nearer the US$5.14 bullish fair value.

For Petco Health and Wellness Company, however, we will make it really easy for you with previews of two leading Petco Health and Wellness Company narratives:

First up is a more optimistic take that leans into pet wellness trends and the potential for better profitability.

🐂 Petco Health and Wellness Company Bull Case

Fair value in this bullish narrative: US$4.53 per share.

Current price vs this fair value: about 20.1% below that estimate, using the simple Wall St narrative fair value.

Implied annual revenue growth used in the model: 1.90%.

Focus on integrating services like veterinary care and grooming with premium products, aiming for higher customer lifetime value and stronger margins across stores and digital. Emphasis on pet wellness, premium assortments and experiential retail, with the view that these could support ongoing earnings growth if execution stays on track. Analysts in this camp work with earnings and margin assumptions that line up with the higher end of current price targets, and they use a discount rate of 12.5% to bring those expectations back to today.

Now here is a more cautious narrative that leans on execution risk, softer sales trends and pressure from online competition.

🐻 Petco Health and Wellness Company Bear Case

Fair value in this bearish narrative: US$2.30 per share.

Current price vs this fair value: about 57.4% above that estimate, based on the bearish narrative fair value.

Implied annual revenue growth used in the model: 0.61%.

Highlights ongoing pressure on net sales and comparable sales, with concern that store traffic and e commerce execution may limit future top line progress. Points to tariff related cost pressure, elevated debt and capital heavy investments as factors that could constrain flexibility if returns on those projects fall short. Assumes a lower valuation multiple and uses slightly above 12% as a discount rate, reflecting a view that the market might be pricing in more success than these analysts are comfortable with.

Taken together, these narratives frame the current debate around Petco Health and Wellness Company, from a scenario where pet wellness and service led growth support a higher fair value to one where execution risks and softer sales argue for a lower one. Your own view on store performance, e commerce progress and future profitability will likely guide which side feels closer to how you see the stock today.

Curious how numbers become stories that shape markets? Explore Community Narratives

Do you think there’s more to the story for Petco Health and Wellness Company? Head over to our Community to see what others are saying!

NasdaqGS:WOOF 1-Year Stock Price Chart

NasdaqGS:WOOF 1-Year Stock Price Chart

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We’ve created the ultimate portfolio companion for stock investors, and it’s free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com