Report Overview

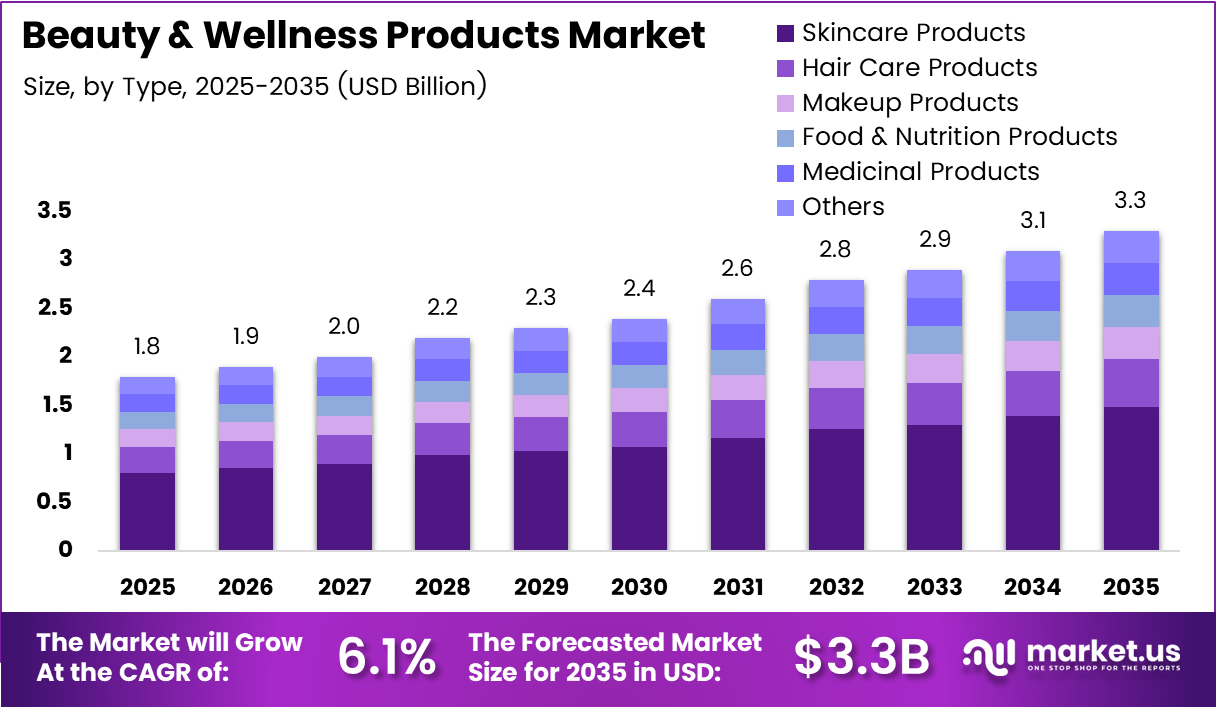

Global Beauty and Wellness Products Market size is expected to be worth around USD 3.3 Billion by 2035 from USD 1.8 Billion in 2025, growing at a CAGR of 6.1% during the forecast period 2026 to 2035.

The beauty and wellness products market covers a broad commercial ecosystem spanning skincare, hair care, makeup, food and nutrition products, medicinal formulations, and lifestyle wellness solutions. Consumer spending in this space reflects a structural behavioral shift — personal care has moved from discretionary to routine, compressing demand volatility and making this category recession-resistant.

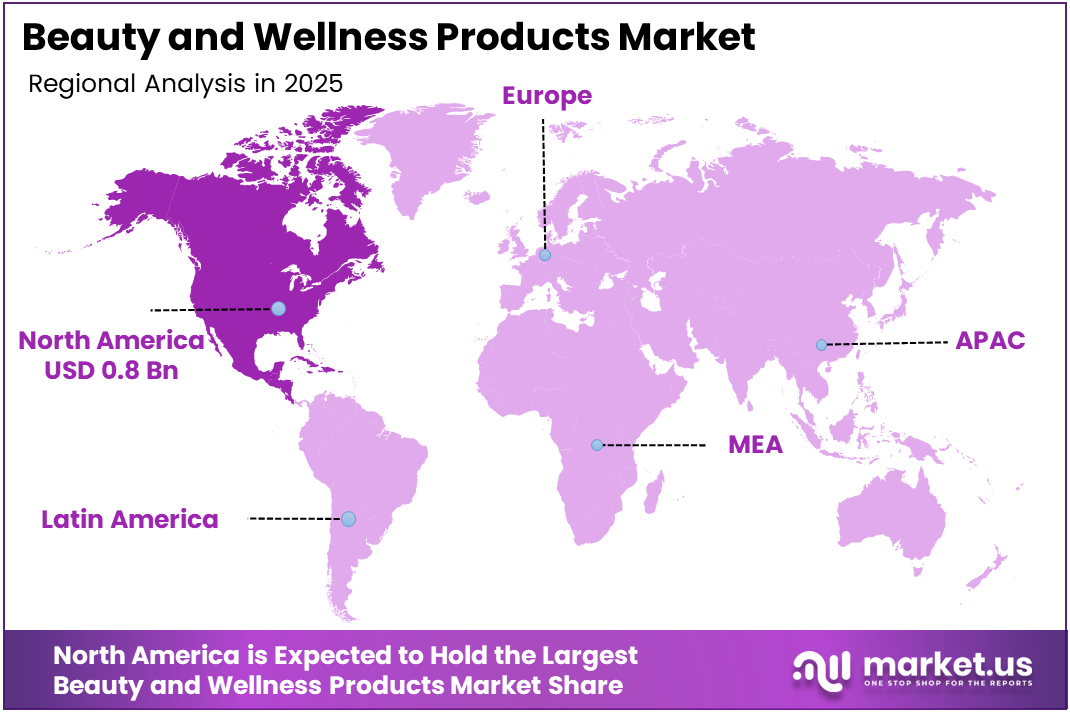

North America leads all regions with a 47.8% market share, valued at approximately USD 0.8 Billion. This dominance reflects the region’s mature retail infrastructure, high per-capita spending on personal care, and early adoption of premium wellness brands. These conditions position North America as the benchmark market from which global expansion strategies typically originate.

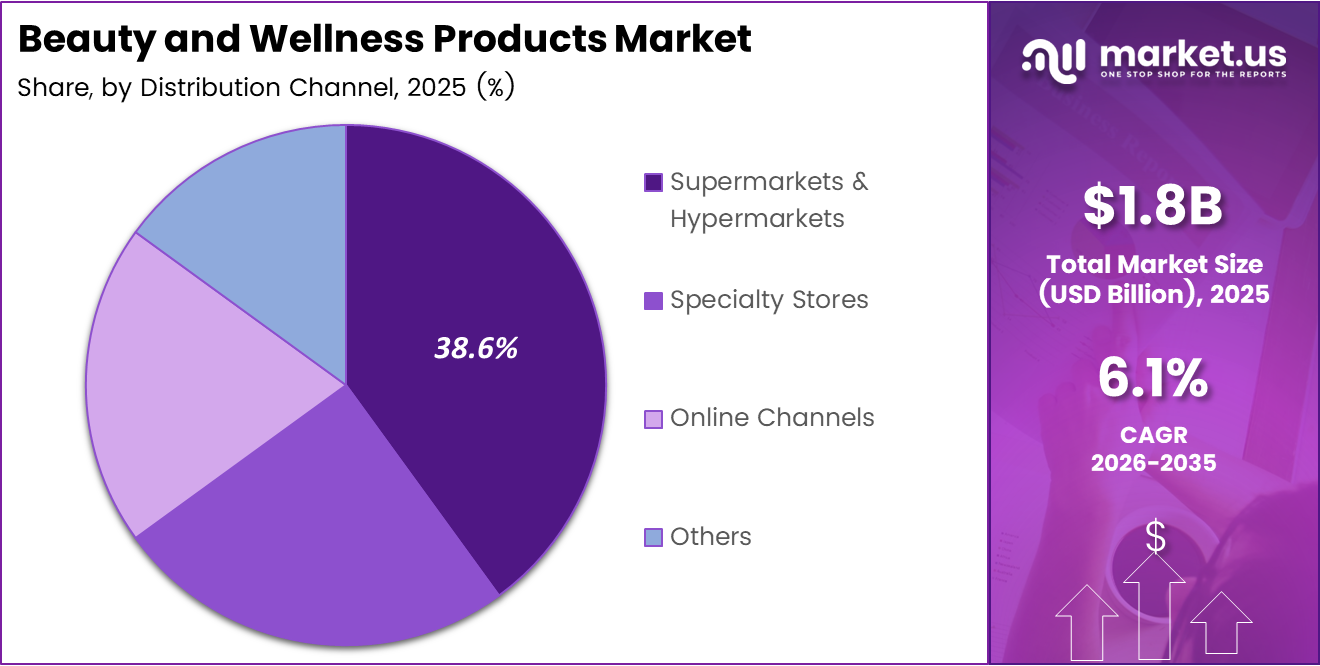

Supermarkets and hypermarkets hold a 38.6% share of distribution, while online channels continue to close that gap through direct-to-consumer brand models. This dual-channel dynamic forces legacy brands to defend shelf space while simultaneously building digital infrastructure — a costly but unavoidable strategic requirement.

Skincare products command a 38.5% share of the market by type, reflecting consumers’ prioritization of preventive care and dermatological wellness. This segment’s dominance signals that product efficacy and clinical credibility now outweigh purely aesthetic claims as purchase drivers, reshaping how brands position across all sub-categories.

In January 2025, Tru Fragrance & Beauty acquired Lake & Skye, a mission-driven fragrance and wellness brand, signaling that mid-market consolidation is accelerating as acquirers seek to absorb niche, founder-led brands before they scale independently. This pattern reflects the broader market reality that organic brand trust is now a premium acquisition asset.

According to L’Occitane Group’s ESG Report FY2025, the company achieved 97% renewable electricity across all own manufacturing sites, with 99% of manufacturing electricity from renewable sources. This metric matters beyond sustainability optics — it signals that operational cost structures in premium beauty are converging around clean energy, and brands that lag on this transition face both reputational and regulatory exposure.

According to L’Occitane Group’s ESG Report FY2025, the company reported 0% of products subject to recall for safety and health reasons, with a Net Promoter Score of 70% for L’Occitane en Provence. A 70% NPS in a category where consumer loyalty is hard-won confirms that quality consistency, not marketing spend alone, is the primary retention engine in premium beauty and wellness.

Key Takeaways

The global Beauty and Wellness Products Market was valued at USD 1.8 Billion in 2025 and is forecast to reach USD 3.3 Billion by 2035.

The market is projected to expand at a CAGR of 6.1% during the forecast period 2026 to 2035.

By Type, Skincare Products lead with a 38.5% market share in 2025.

By Distribution Channel, Supermarkets & Hypermarkets hold the dominant share at 38.6%.

North America dominates the regional landscape with a 47.8% market share, valued at approximately USD 0.8 Billion.

Key players include L’Oréal S.A., Unilever Plc., The Estée Lauder Companies Inc., The Procter & Gamble Company, and LVMH, among others.

Product Analysis

Skincare Products dominate with 38.5% due to rising preventive care and clinical demand.

In 2025, Skincare Products held a dominant market position in the By Type segment of the Beauty and Wellness Products Market, with a 38.5% share. Consumers increasingly treat skincare as a health investment rather than a cosmetic routine. This behavioral shift rewards brands with dermatology-backed formulations and penalizes those competing purely on aesthetics or packaging claims.

Hair Care Products serve as a high-frequency repeat-purchase category within the personal care portfolio. Consumers replace hair care items regularly, creating predictable revenue cycles for brands. However, the segment faces rising competition from direct-to-consumer brands offering personalized formulas, which erodes loyalty toward mass-market product lines. In March 2025, Unilever Ventures invested in Indē Wild, an Indian Ayurvedic hair and beauty brand, to capitalize on the global appetite for heritage-sourced, natural formulations.

Makeup Products differentiate through trend sensitivity and social media velocity. A single viral product launch can shift sales distribution within weeks. This volatility makes the segment high-reward but operationally demanding — brands must maintain both deep inventory depth and rapid product rotation to remain relevant across consumer cohorts.

Food & Nutrition Products represent the fastest-growing bridge between wellness and beauty. Consumers who invest in skin and hair health through ingestible supplements signal a fundamental expansion of the beauty category’s boundaries. This convergence creates cross-sell opportunities for brands already operating in topical skincare or hair care.

Medicinal Products carry the highest credibility premium within the broader wellness category. Formulations with documented clinical backing command significant price premiums and encounter lower price resistance from health-oriented consumers. This segment’s growth reflects the mainstreaming of dermatologist-recommended and pharmacy-adjacent beauty positioning.

Wellness Products capture demand at the intersection of lifestyle, mental health, and physical self-care. Brands operating in this sub-segment benefit from the halo effect of the broader self-care movement. However, differentiation is structurally difficult because wellness positioning can be adopted by competitors without significant formulation investment.

Others encompass niche and emerging product formats that do not yet fit established category definitions. This segment functions as an incubator layer — products that gain commercial traction here often migrate into defined categories over time, making it a useful leading indicator of where the broader market is heading.

Distribution Channel Analysis

Supermarkets & Hypermarkets dominate with 38.6% due to high foot traffic and broad SKU access.

In 2025, Supermarkets & Hypermarkets held a dominant market position in the By Distribution Channel segment of the Beauty and Wellness Products Market, with a 38.6% share. Physical retail consolidates impulse purchasing and trial behavior into a single touchpoint. Brands that secure prominent shelf positioning in high-footfall grocery environments benefit from passive discovery that no paid digital channel fully replicates.

Specialty Stores carry the highest margin and highest-intent shopper profile within the channel mix. Consumers entering a dedicated beauty retailer have already committed to purchase consideration, which raises conversion rates and average basket values above general grocery formats. This makes specialty retail the preferred launch environment for premium and clinical-grade product lines.

Online Channels enable brands to reach consumers outside traditional retail geographies, compress the distance between brand narrative and transaction, and collect first-party data that informs product development. The direct-to-consumer model removes wholesale margin compression, but demands significant investment in logistics, digital marketing, and customer retention infrastructure to sustain profitability.

Others include direct sales, salon and spa channels, pharmacy retail, and subscription box formats. These channels serve specific consumer trust archetypes — the pharmacy shopper prioritizes clinical validation, while the salon buyer defers to professional recommendation. Brands that map channel selection to consumer trust behavior outperform those treating all touchpoints as interchangeable.

Key Market Segments

By Type

Skincare Products

Hair Care Products

Makeup Products

Food & Nutrition Products

Medicinal Products

Wellness Products

Others

By Distribution Channel

Supermarkets & Hypermarkets

Specialty Stores

Online Channels

Others

Drivers

Rising Consumer Spending and Social Media Influence Accelerate Adoption of Skincare and Wellness Beauty Products

Consumer spending on personal care, skincare, and wellness-oriented beauty products has shifted from discretionary to habitual. This transition compresses the spending volatility that historically made beauty a cyclical category. Brands with strong repeat-purchase mechanics — particularly in skincare and hair care — now operate with more predictable revenue floors than in previous market cycles.

Social media platforms have compressed the product discovery-to-purchase cycle to hours for trend-driven categories. Celebrity endorsements and influencer content generate product demand at a speed that traditional retail shelf planning cannot accommodate. In February 2025, L’Oréal Groupe made a minority investment in Jacquemus and entered an exclusive long-term beauty partnership — a direct strategic response to the convergence of fashion credibility and beauty purchasing behavior.

According to Givaudan’s 2025 Integrated Report, the company achieved 100% purchased renewable electricity across operations, with 93% implementation of energy efficiency best practices globally. This operational benchmark reflects how leading ingredient and formulation suppliers are embedding sustainability as a structural input cost — which in turn signals that brands sourcing from these suppliers face rising material standards that consumers and regulators will increasingly require.

Restraints

Regulatory Compliance Burdens and High Market Entry Costs Constrain Competitive Supply Growth

Cosmetic ingredients and wellness formulations face stringent safety and compliance standards across global markets. These regulatory requirements vary significantly by jurisdiction, forcing multi-market brands to maintain parallel compliance workflows. For smaller entrants, this operational overhead creates a structural cost disadvantage that larger incumbents can absorb more efficiently.

High product development, branding, and marketing costs raise the minimum viable investment threshold for new market participants. A credible beauty brand launch now requires clinical substantiation, sustainable packaging, and a funded digital presence simultaneously. This compressed the competitive funnel — only well-capitalized entrants can meet baseline consumer and retailer expectations from launch.

According to Givaudan’s 2025 Integrated Report, the company achieved a 32% reduction in water withdrawal on sites facing water stress versus the 2020 baseline. This metric illustrates the depth of operational investment required to meet sustainability compliance standards — expenditures that smaller formulation and brand players cannot fund without external capital, reinforcing the incumbency advantage of large, resource-rich operators.

Growth Factors

Personalized Beauty, Men’s Wellness, E-Commerce Expansion, and Nutricosmetics Open New Revenue Tiers

AI-based skincare solutions and personalized beauty formulations address the fundamental limitation of mass-market products — one-size-fits-all efficacy claims. Brands that deliver individualized recommendations backed by diagnostic tools convert curiosity into subscription-level loyalty. This model also generates proprietary consumer data that compounds competitive advantage over time as algorithms improve with each interaction.

Male grooming, beard care, and men’s wellness products represent an underpenetrated demand segment with above-average growth potential. Male consumers historically underinvested in personal care relative to their female counterparts, but shifting cultural norms are closing that gap. Brands that establish early positioning in this segment benefit from lower competitive intensity and higher first-mover retention rates. In April 2025, Unilever acquired Wild, a UK refillable personal care brand, signaling that sustainable and gender-inclusive personal care formats are emerging as genuine volume opportunities rather than niche positioning plays.

According to L’Occitane Group’s ESG Report FY2025, the company sourced 54% of raw materials from regenerative agriculture or organic-certified sources, up from 50% in FY2024. This supply chain shift demonstrates a concrete link between organic sourcing investment and brand positioning — a model that directly supports the premium pricing power that nutricosmetics and clean-label beauty brands require to sustain margins in competitive retail environments.

Emerging Trends

Sustainable Packaging, Biotech Skincare, At-Home Devices, and Holistic Beauty Redefine Category Boundaries

Sustainable, eco-friendly, and refillable beauty packaging has moved from a marketing differentiator to a baseline consumer expectation in key markets. Brands that fail to transition away from single-use plastic packaging now face both shelf-listing pressure from major retailers and accelerating consumer rejection. The operational investment required for this transition creates a near-term cost headwind but a durable brand equity advantage.

Biotechnology and dermatology integration in skincare formulations is shifting the efficacy conversation from cosmetic to clinical. Brands that develop or license biotech-derived actives can substantiate performance claims at a precision level that traditional cosmetic chemistry cannot match. This creates a premium pricing tier that is structurally protected from private-label competition because replication requires significant R&D infrastructure.

According to Givaudan’s 2025 Integrated Report, the company reduced its total recordable case rate by 48% since the 2018 baseline, reaching 1.33 in 2025. Beyond safety compliance, this metric signals that ingredient and formulation suppliers are operating at a standard of process discipline that increasingly flows through to product quality and regulatory documentation — a trend that directly supports the clinical credibility claims that at-home beauty device and advanced skincare brands depend on for consumer trust.

Regional Analysis

North America Dominates the Beauty and Wellness Products Market with a Market Share of 47.8%, Valued at USD 0.8 Billion

North America leads the global beauty and wellness products landscape with a 47.8% share, valued at approximately USD 0.8 Billion. This position reflects the region’s mature specialty retail infrastructure, high consumer willingness to pay for premium formulations, and a well-funded brand ecosystem that continuously resets category benchmarks. Additionally, regulatory frameworks here accelerate clinical beauty adoption ahead of other regions.

Europe Beauty and Wellness Products Market Trends

Europe occupies a structurally strong second position, anchored by Germany, France, and the UK as the primary consumption markets. The region’s regulatory environment — particularly under EU cosmetics legislation — sets some of the world’s highest ingredient safety standards, which paradoxically advantages compliant incumbents by raising entry costs for formulation newcomers. Moreover, French luxury beauty brands set global pricing benchmarks. In January 2025, SKKY Partners made a minority investment in 111Skin, a clinically inspired skincare brand, to strengthen its direct-to-consumer business and expand in North America and Asia, reflecting European clinical brands’ growing cross-regional ambitions.

Asia Pacific Beauty and Wellness Products Market Trends

Asia Pacific represents the highest long-term volume growth opportunity in the global market. China, Japan, South Korea, and India each carry distinct beauty consumption cultures — K-beauty’s multi-step skincare philosophy, Japanese minimalist efficacy, and India’s Ayurvedic heritage all create product differentiation frameworks that export well globally. Additionally, rising middle-class disposable income across APAC markets continuously expands the addressable consumer base for premium beauty.

Latin America Beauty and Wellness Products Market Trends

Latin America presents a mid-tier growth opportunity where Brazil and Mexico anchor regional demand. Brazil’s large and beauty-engaged consumer population makes it one of the world’s top-five beauty markets by volume. However, import tariffs, currency volatility, and fragmented retail infrastructure raise the operational complexity for international brands seeking profitable market entry without local manufacturing or distribution partnerships.

Middle East and Africa Beauty and Wellness Products Market Trends

The Middle East and Africa region operates across two distinct sub-markets. GCC countries — particularly the UAE and Saudi Arabia — show strong appetite for luxury and premium beauty products, supported by high per-capita income and a young, aspirational consumer demographic. Sub-Saharan Africa represents an earlier-stage opportunity, where urban population growth and expanding modern retail formats are the primary structural enablers of future market development.

Key Regions and Countries

North America

Europe

Germany

France

The UK

Spain

Italy

Rest of Europe

Asia Pacific

China

Japan

South Korea

India

Australia

Rest of APAC

Latin America

Brazil

Mexico

Rest of Latin America

Middle East & Africa

GCC

South Africa

Rest of MEA

Key Company Insights

L’Oréal S.A. anchors its competitive position through a dual strategy of luxury brand acquisition and mass-market volume scale. The company’s February 2025 minority investment in Jacquemus and its October 2025 acquisition of Kering’s beauty division demonstrate a deliberate move to capture fashion-credibility adjacency within the luxury beauty tier — a positioning that competitors relying purely on organic brand development cannot replicate at comparable speed.

Unilever Plc. operates with a strategic portfolio logic built on sustainability differentiation and emerging-market access. Its April 2025 acquisition of Wild — a UK refillable personal care brand — and its March 2025 investment in Indē Wild signal that the company is building a refillable and natural beauty sub-portfolio ahead of regulatory pressure. This positions Unilever to capture the premium-but-sustainable consumer segment before it becomes the mainstream default.

The Estée Lauder Companies Inc. derives structural competitive advantage from its dominance in prestige department store and specialty beauty retail channels. The company’s brand portfolio spans multiple price tiers within the premium segment, allowing it to capture consumer trading up and down without category exit. This channel depth creates barriers to displacement that digitally native brands — despite their acquisition efficiency — struggle to replicate at equivalent scale.

The Procter & Gamble Company leverages formulation science and retail distribution scale as its primary competitive moats in beauty and personal care. Its R&D investment enables continuous incremental product improvement across large-volume SKUs, compounding margin protection through defensible efficacy claims. P&G’s strength in mass-market channels also gives it pricing power in value-sensitive consumer segments that premium-focused competitors cannot efficiently serve.

Key Players

L’Oréal S.A.

Unilever Plc.

The Estée Lauder Companies Inc.

The Procter & Gamble Company

LVMH

Maison Margiela

Beiersdorf AG

Shiseido Co., Ltd.

Coty Inc.

Rituals Cosmetics Enterprise B.V.

Kao Corporation

Recent Developments

May 2025 — e.l.f. Beauty acquired Rhode, Hailey Bieber’s skincare and colour cosmetics brand, in a $1 billion deal, with Bieber continuing as Chief Creative Officer and Head of Innovation. This transaction represents one of the largest celebrity-founded brand acquisitions in recent beauty market history, validating the revenue multiple that high-authenticity consumer brands command.

September 2025 — Space Camp Wellness launched its exclusive USDA-certified organic Berry Stardust lip balm for retail debut at Target stores nationwide. The placement at a mass retail giant signals that USDA-certified organic lip care has crossed from specialty to mainstream channel accessibility.

September 2025 — Beekman 1802 launched the Pistachio & Dark Cherry scent in its Milk Shake Body, Whipped Body Cream, and Hand & Body Wash lines using proprietary microbiome-friendly Z-Biome technology. The use of microbiome science in body care formulations reflects the broader biotech integration trend reshaping product development across premium personal care.

September 2025 — Sincerely Yours launched its clean, dermatologist-developed teen skincare brand with a Barrier Friendly Formula exclusively at Sephora stores and online. A dedicated teen skincare line with clinical dermatologist backing at Sephora confirms that Gen Z consumers now represent a distinct, high-value purchasing cohort with specific product requirements.

October 2025 — L’Oréal acquired Kering’s beauty division, including key fragrance and wellness assets, as part of a major strategic expansion in luxury beauty. This acquisition consolidates significant luxury fragrance and wellness brand equity within the L’Oréal portfolio, accelerating its competitive separation from the second tier of global beauty conglomerates.

November 2024 — OneSkin raised $20 million in Series A funding to accelerate research and development of peptide-based anti-aging skincare formulas focused on skin longevity at the cellular level. This investment signals that institutional capital views cellular longevity science as the next defensible premium tier in anti-aging skincare, ahead of mainstream market adoption.

Report Scope