Valuation After Recent Share Price Pullback")

Recent share performance and business scale

With no single headline event driving attention, e.l.f. Beauty (ELF) is drawing investor interest after a period of weaker share performance, including a 34% drop over the past month and a 24% decline over the past 3 months.

At a last close of US$61.05, the Oakland based beauty company has a market value of about US$3.9b. It reported annual revenue of US$1.52b with net income of US$103.94m.

See our latest analysis for e.l.f. Beauty.

The recent 34% 1 month share price return decline and 24% 3 month share price return decline come after a longer run in which the 5 year total shareholder return is still up 126.61%. Recent momentum looks to be fading even as the longer term story remains positive.

If the recent pullback has you reassessing opportunities in consumer names, it can also be a good moment to widen your search and uncover 20 top founder-led companies

With e.l.f. Beauty now trading well below recent levels, despite annual revenue of US$1.52b and net income of US$103.94m, is the pullback opening a value gap, or is the market already baking in future growth?

Most Popular Narrative: 76% Undervalued

According to the most followed narrative from WallStreetWontons, a fair value of about $251 for e.l.f. Beauty sits well above the last close at $61.05, which frames the recent pullback in a very different light for anyone focused on long term potential rather than short term price swings.

e.l.f. Beauty has experienced tremendous growth in recent years, and several key catalysts have contributed to this success. Here are some of the most significant factors driving the company’s expansion:

Strong Brand Positioning and Product Innovation: e.l.f. Beauty has established itself as a leading brand in the masstige beauty category, offering high-quality products at affordable prices. The company is known for its innovative approach to product development, consistently introducing new and exciting items that appeal to a wide range of consumers.

Curious what has to happen for that higher fair value to make sense? The narrative leans on sustained brand strength, expanding reach, and profitability assumptions that are anything but conservative.

Result: Fair Value of $251 (UNDERVALUED)

Have a read of the narrative in full and understand what’s behind the forecasts.

However, the narrative could unravel if decelerating sales growth persists and rising costs continue to pressure margins, particularly given that a high valuation already appears to be reflected in the share price.

Find out about the key risks to this e.l.f. Beauty narrative.

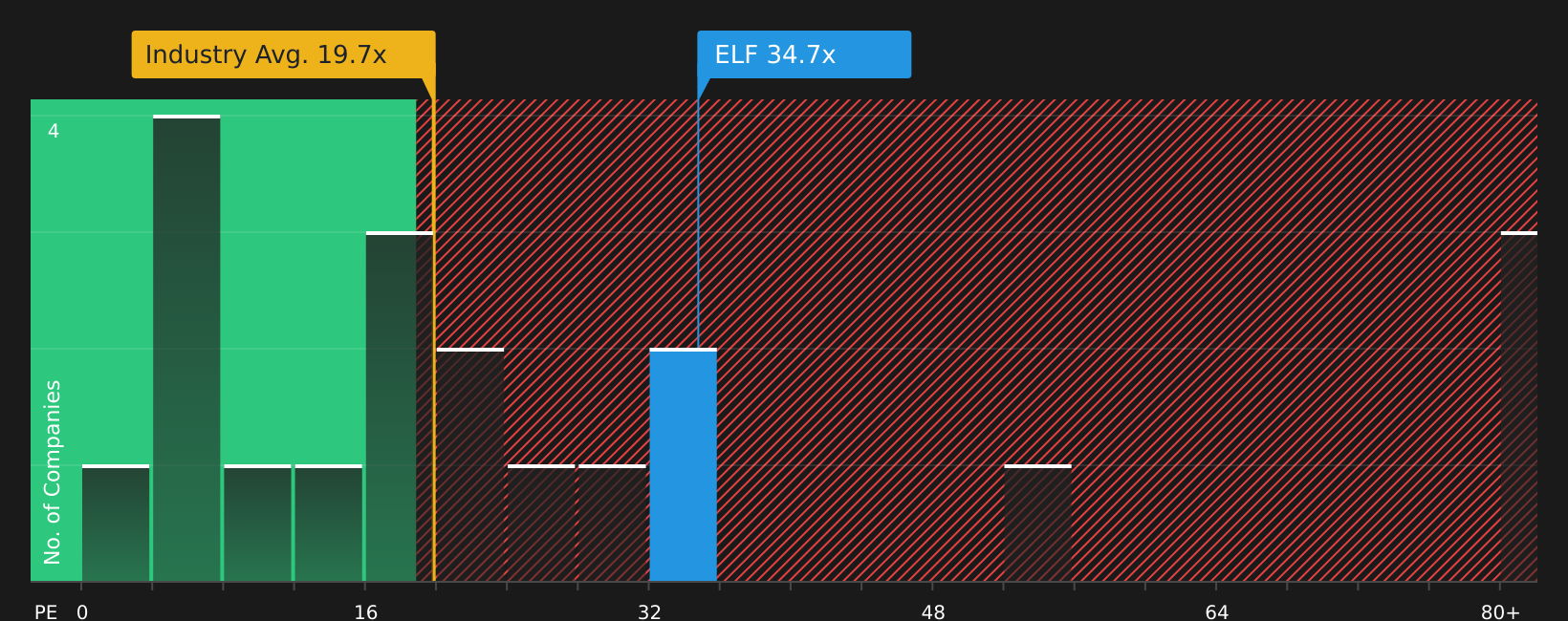

Another valuation lens: earnings multiples send a different message

The most popular fair value estimate of $251 leans on strong growth and profitability assumptions. By contrast, e.l.f. Beauty trades on a P/E of 34.7x, which sits below the fair ratio of 41.2x but well above peers at 10.1x and the wider Personal Products industry at 19.7x. That mix of apparent discount to the fair ratio and premium to peers leaves a simple question: is this a quality story at a high entry price or just a crowded trade waiting to reset?

For a closer look at how this P/E gap stacks up against peers and the fair ratio in practice, See what the numbers say about this price — find out in our valuation breakdown.

NYSE:ELF P/E Ratio as at Mar 2026

NYSE:ELF P/E Ratio as at Mar 2026

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out e.l.f. Beauty for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 61 high quality undervalued stocks. If you save a screener we even alert you when new companies match – so you never miss a potential opportunity.

Next Steps

With sentiment clearly split between risks and rewards, this is a moment to look at the data first hand and move quickly while debate is active. Start with 3 key rewards and 1 important warning sign.

Ready to hunt for more opportunities?

If e.l.f. Beauty is on your radar, do not stop there. Put the same focus into finding other ideas before the market does.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We’ve created the ultimate portfolio companion for stock investors, and it’s free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com