Report Overview

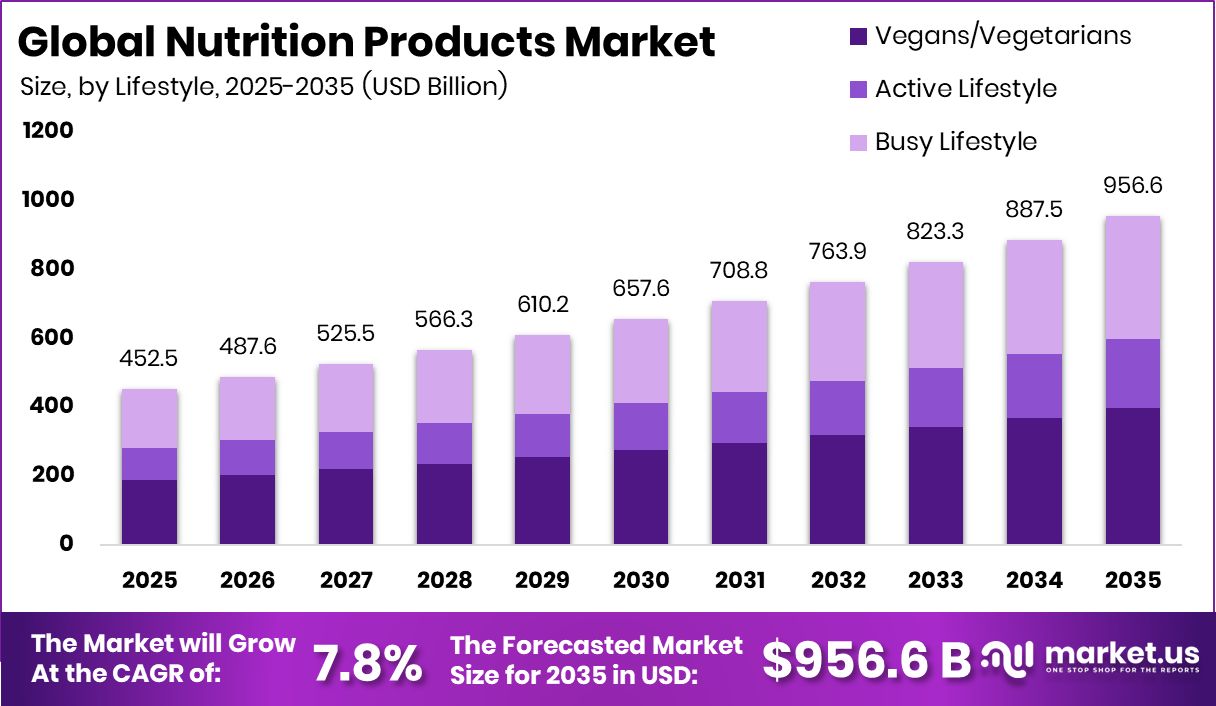

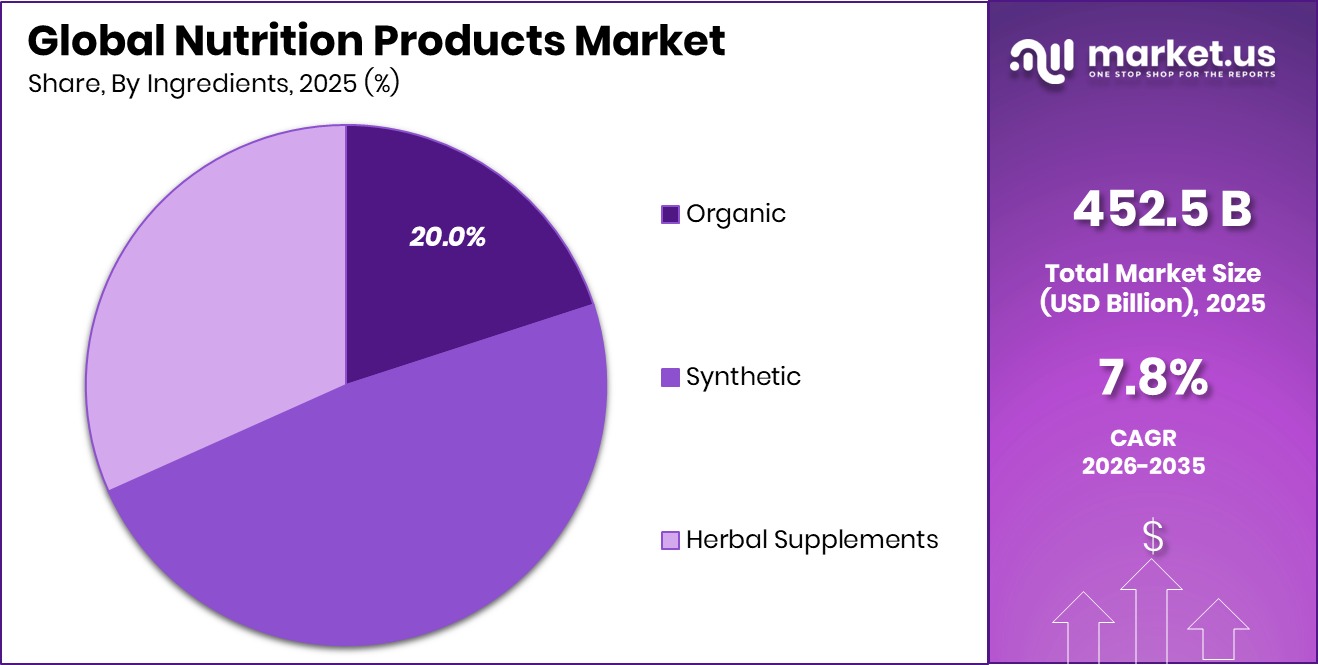

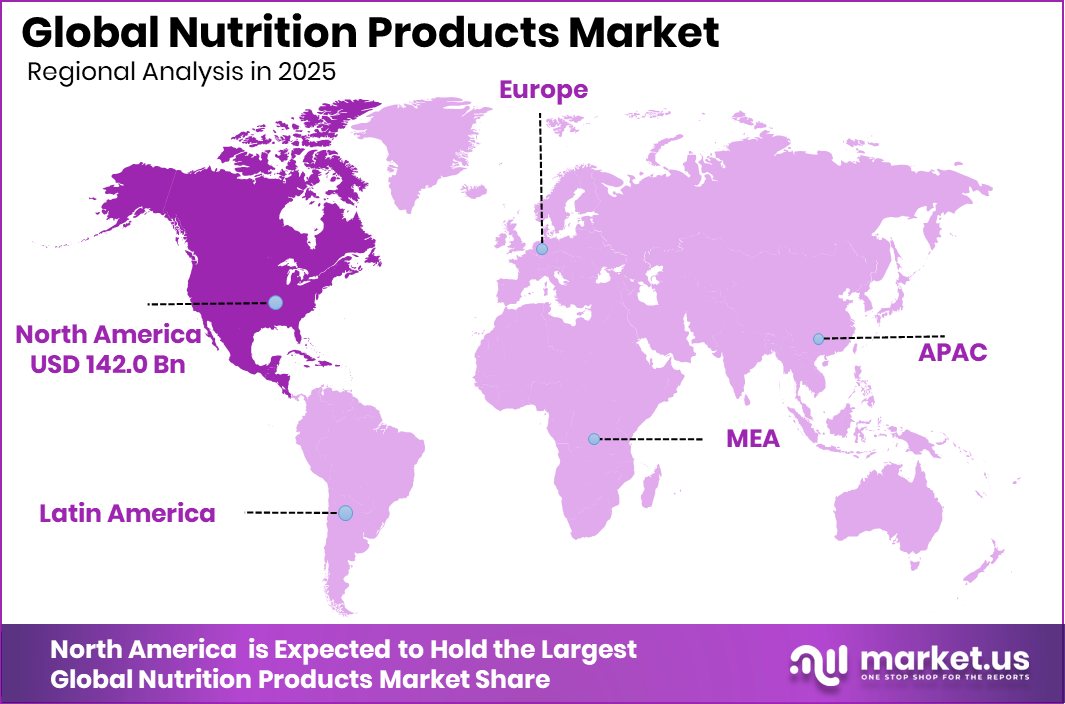

The Global Nutrition Products Market is expected to be worth around USD 956.6 billion by 2035, up from USD 452.5 billion in 2025. It is projected to grow at a CAGR of 7.8% from 2026 to 2035. North America accounted for 31.4%, valued at USD 142.0 Bn marketwide in 2025 overall.

Nutrition Products are consumable health-focused products designed to support daily dietary needs, improve wellness, and address specific nutritional gaps. These include dietary supplements, meal replacement products, medical foods, plant-based products, and other functional nutrition solutions. They are widely used across age groups, lifestyles, and health goals, helping consumers manage immunity, energy, weight, muscle health, and long-term wellness through convenient formats such as powders, capsules, bars, drinks, and fortified foods.

The Nutrition Products Market refers to the global industry built around the development, production, distribution, and sale of these nutrition-supporting products. The market is structured across your taxonomy, including type, age group, lifestyle, ingredients, and distribution channels, creating broad consumer relevance. Growth is strongly supported by rising health awareness, preventive nutrition habits, aging populations, active lifestyles, and the increasing shift toward plant-based and specialized formulations.

Additional momentum is visible through strong funding activity, including FDA’s $7.2 billion food safety and nutrition initiative, NextFoods’ $10M functional nutrition expansion, David’s $10M seed funding for science-based products, Herbalife Nutrition’s RMB 600 million China growth fund, and Needed’s $3.7M seed financing, all of which reflect continued innovation and category expansion.

A major growth factor in this market is the widening use of personalized and lifestyle-based nutrition. Consumers aged 20–39 seek convenient products for busy routines, while those aged 40+ increasingly prioritize preventive wellness and condition-focused support. Demand for vegan, active lifestyle, and herbal supplement products is also accelerating product diversification.

From a demand perspective, supermarkets, online stores, and health food stores continue to improve product accessibility, allowing faster consumer adoption. Strong interest in organic, synthetic, and herbal ingredient formats supports steady category expansion across multiple use cases and preferences.

The strongest opportunity lies in innovation-led premiumization, where brands can target meal replacement, medical foods, and plant-based nutrition with age-specific and lifestyle-specific solutions. Expanding consumer trust, broader retail penetration, and continued capital inflow into science-backed formulations create long-term opportunities for new product development and global category growth.

In April 2024, Bayer AG, which works in consumer health, vitamins, minerals, and nutritional supplements, expanded its nutrition-focused consumer portfolio through continued One A Day wellness product innovation and line extension activities. This 2024 development strengthened its daily nutrition and immunity support offerings, improving relevance in preventive health solutions.

Key Takeaways

The Global Nutrition Products Market is expected to be worth around USD 956.6 billion by 2035, up from USD 452.5 billion in 2025. It is projected to grow at a CAGR of 7.8% from 2026 to 2035.

In the Nutrition Products Market, dietary supplements lead by type, capturing 44.8% share globally today.

Within the Nutrition Products Market, consumers aged 40-59 dominate demand with a 45.2% share worldwide.

In the Nutrition Products Market, vegans and vegetarians represent 41.7% through strong lifestyle-driven purchasing trends.

Across the Nutrition Products Market, synthetic ingredients account for 48.3%, reflecting scalability and consistency worldwide.

In the Nutrition Products Market, supermarkets and hypermarkets contribute 36.8% through convenient mass retail distribution.

At 31.4%, North America generated USD 142.0 Bn, dominating nutrition sales regionally today strongly.

By Type Analysis

In the nutrition products market, dietary supplements lead the type segmentation with a 44.8% share.

In 2025, the Nutrition Products Market is strongly shaped by the growing dominance of dietary supplements, which account for 44.8% of the market by type. This leading share reflects rising consumer awareness around preventive healthcare, immunity support, and daily wellness routines. People are increasingly turning to vitamins, minerals, protein blends, and functional capsules to fill nutritional gaps caused by busy lifestyles and changing food habits. The demand is especially high among working professionals, fitness-focused consumers, and aging populations looking for convenient health solutions.

Manufacturers are responding with personalized formulations, clean-label claims, and targeted benefits such as energy, gut health, and immunity. This segment’s strong performance highlights how supplements continue to move from optional products to essential everyday nutrition choices across both developed and emerging markets.

By Age Group Analysis

Age 40-59 dominates the nutrition products market, accounting for 45.2% globally.

In 2025, the Nutrition Products Market sees its strongest age-based demand coming from consumers aged 40–59, who contribute 45.2% of total market share. This age group is highly focused on maintaining long-term health, managing lifestyle-related conditions, and supporting active aging. Products aimed at bone strength, heart health, joint care, immunity, and weight management are especially popular among these consumers. As individuals in this demographic often have stable incomes and greater awareness of wellness, they are more willing to invest in premium nutrition solutions.

Brands are increasingly launching age-specific formulations that address metabolism changes and energy support needs. The high contribution from this segment shows how middle-aged consumers are becoming the backbone of market growth, driving innovation and encouraging companies to expand specialized offerings tailored to healthy aging goals.

By Lifestyle Analysis

Vegans and vegetarians represent 41.7% of the nutrition products market’s lifestyle consumers worldwide.

In 2025, the Nutrition Products Market is significantly influenced by vegan and vegetarian lifestyles, with this segment accounting for 41.7% of the market by lifestyle preference. The rise reflects a global shift toward plant-based living, driven by health consciousness, ethical choices, and environmental concerns.

Consumers following these lifestyles actively seek protein powders, fortified beverages, plant-based vitamins, omega alternatives, and natural superfood blends that align with their dietary values. This demand is encouraging brands to develop soy-free, dairy-free, and allergen-friendly formulations using pea protein, algae-based omega-3, and botanical extracts.

The trend is also supported by younger urban populations who view plant-based nutrition as part of a holistic wellness routine. As this consumer base expands, the market continues to evolve toward sustainable, transparent, and naturally sourced nutrition products.

By Ingredients Analysis

Synthetic ingredients hold a 48.3% share in the nutrition products market formulations globally today.

In 2025, synthetic ingredients led the Nutrition Products Market by ingredient type, capturing 48.3% of the total share. This dominance is largely due to the consistency, scalability, and cost-effectiveness that synthetic formulations offer manufacturers. Synthetic vitamins, minerals, amino acids, and fortified compounds are widely used because they provide precise dosages, longer shelf life, and easier mass production. These advantages make them highly suitable for tablets, capsules, powders, and fortified food products sold globally.

Despite the growing interest in natural ingredients, synthetic options remain preferred in many mainstream products because they support affordability and standardized quality. Pharmaceutical-grade precision and regulatory compliance also strengthen this segment’s market position. The continued reliance on synthetic ingredients highlights their importance in meeting large-scale consumer demand for accessible and reliable nutrition solutions.

By Distribution Channel Analysis

Supermarkets and hypermarkets capture 36.8% of the nutrition products’ market distribution channels worldwide.

In 2025, supermarkets and hypermarkets remain the leading distribution channel in the Nutrition Products Market, holding 36.8% of total market share. Their strong position comes from wide product availability, consumer trust, and the convenience of comparing multiple brands in one location. These retail spaces allow shoppers to physically inspect packaging, review nutritional claims, and make instant purchase decisions, which is especially important for first-time buyers. Promotional offers, discounts, and bundle deals further boost sales through this channel.

Major retailers are also dedicating larger shelf spaces to protein powders, supplements, fortified snacks, and wellness drinks, reflecting growing demand. The dominance of supermarkets and hypermarkets shows that traditional retail still plays a crucial role in consumer purchasing behavior, even as online channels continue to expand within the broader nutrition products industry.

Key Market Segments

By Type

By Age Group

Age 20-39

Age 40-59

Age 60 and above

By Lifestyle

Vegans/Vegetarians

Active Lifestyle

Busy Lifestyle

By Ingredients

By Distribution Channel

Supermarkets/Hypermarkets

Online Stores

Health Food Stores

Others

Driving Factors

Rising preventive healthcare boosts supplement adoption

A major driving factor in the Nutrition Products Market is the rising focus on preventive healthcare, which continues to boost supplement adoption across daily wellness routines. Consumers are increasingly choosing vitamins, minerals, immunity boosters, and condition-support nutrition products to reduce future health risks and maintain long-term wellbeing. This momentum is further reinforced by large-scale public health support, highlighted by the FDA Seeks $7.2 Billion to Enhance Food Safety and Nutrition, Advance Medical Product Safety, and Strengthen Public Health initiative.

Such large funding support strengthens confidence in nutrition-linked health systems and encourages broader product innovation, quality enhancement, and category expansion. The shift toward prevention-first health behavior is making nutrition products a regular part of modern lifestyles, supporting stronger demand across age groups, wellness needs, and preventive care applications worldwide.

Busy lifestyles increase meal replacement demand

Another key growth driver in the Nutrition Products Market is the rise of busy lifestyles, which continues to increase demand for convenient meal replacement and ready-to-consume nutrition solutions. Working professionals, students, travelers, and active urban consumers are increasingly preferring products that save time while still delivering balanced nutritional value.

Meal shakes, protein bars, fortified beverages, and grab-and-go nutrition snacks are gaining wider adoption because they fit easily into fast-paced routines. This demand trend is further supported by investment momentum, including ARTAH Nutrition’s £2.85m investment to grow its dietary supplement business, which reflects confidence in scalable wellness and convenience-led nutrition solutions. The growing preference for easy, portable, and functional nutrition formats is strengthening this factor as a long-term demand accelerator for the overall market.

Restraining Factors

High product costs limit accessibility

A major restraining factor for the Nutrition Products Market is the high cost of premium formulations, which can limit product accessibility among price-sensitive consumers. Nutrition products containing advanced blends, specialized ingredients, or targeted wellness benefits often carry higher retail prices, reducing mass-market penetration. This challenge is visible even as investment activity continues, such as Kradle secures $4M investment to expand pet supplement offerings, highlighting how product innovation and expansion often require significant capital.

Higher production costs, ingredient sourcing expenses, and premium packaging further increase end-user prices. As a result, affordability remains a barrier in several consumer segments, especially where everyday nutrition spending competes with broader household budgets. This pricing pressure can slow volume adoption despite strong health awareness and demand potential.

Regulatory complexity slows product approvals globally

Another restraint in the Nutrition Products Market is the complexity of regulatory approvals, which can delay product launches and limit faster innovation cycles. Nutrition products often require ingredient validation, label compliance, safety checks, and region-specific regulatory alignment before reaching commercial shelves. These requirements can slow expansion plans, particularly for new formulations and personalized wellness solutions.

The challenge remains relevant despite rising investor confidence, as seen in Cristiano Ronaldo’s investment in London-based Bioniq, bringing its total valuation to €75.7 Million, showing that even well-funded nutrition-focused businesses must navigate complex compliance environments. Extended approval timelines can affect speed-to-market, reduce launch flexibility, and increase development costs, creating operational pressure for manufacturers seeking faster category growth.

Growth Opportunity

Plant-based nutrition expands untapped consumers

A strong growth opportunity in the Nutrition Products Market lies in plant-based nutrition, which continues to expand untapped consumer segments seeking healthier, ethical, and sustainable alternatives. Demand is rising across vegan, vegetarian, flexitarian, and wellness-driven buyers who increasingly prefer plant-based protein, dairy alternatives, and botanical nutrition solutions. This opportunity is strongly supported by innovation funding, including French startup NxtFood (ACCRO), which raised $58 m to scale an alt-meat platform, aiming for profitability in 12-18 months, reflecting the scalability and commercial confidence surrounding plant-based nutrition expansion. As more consumers align dietary habits with sustainability and health goals, plant-based categories are opening new product spaces across supplements, meal replacements, and functional foods, creating long-term expansion potential for the market.

Personalized wellness creates premium product opportunities

Another major opportunity in the Nutrition Products Market is personalized wellness, where consumers increasingly seek nutrition products tailored to age, lifestyle, health goals, and dietary preferences. Customized vitamins, targeted protein blends, gut-health formulas, and precision wellness products are creating strong premium demand. This opportunity is reinforced by funding activity such as PlantBaby, raising $4 million in seed funding, which highlights continued investor confidence in specialized and targeted nutrition innovation.

Personalized solutions allow brands to improve consumer engagement, boost repeat purchasing, and capture higher-value market segments. As digital health awareness and individualized wellness routines continue to expand, this segment offers strong premiumization and differentiation potential.

Latest Trends

Herbal supplements gain mainstream popularity

A leading trend in the Nutrition Products Market is the mainstream rise of herbal supplements, supported by growing consumer preference for natural, plant-derived, and traditional wellness ingredients. Herbal blends for immunity, digestion, stress support, and daily vitality are increasingly becoming part of modern nutrition habits. This trend aligns with innovation activity such as Project Eaden, which raised $15.6 m Series A to launch ‘ultra-realistic’ plant-based meat using fiber spinning tech, reflecting wider market confidence in plant-led and naturally positioned nutrition solutions. As consumers increasingly associate herbal ingredients with clean-label wellness, this trend continues to influence product development and shelf expansion.

Online stores accelerate direct nutrition sales

Another major trend shaping the Nutrition Products Market is the rapid acceleration of online stores, which are strengthening direct nutrition product sales globally. Consumers increasingly prefer digital platforms for product comparison, subscription purchases, personalized recommendations, and doorstep convenience. This shift is supported by major funding developments such as NotCo getting its horn following a $235M round to expand plant-based food products, showing the scale of digital-first growth opportunities in nutrition-related categories. Online channels are becoming central to brand visibility, repeat engagement, and faster product reach.

Regional Analysis

North America leads the Nutrition Products Market with a 31.4% share, reaching USD 142.0 billion.

In 2025, the Nutrition Products Market demonstrates a regionally diversified growth pattern across North America, Europe, Asia Pacific, the Middle East & Africa, and Latin America, with demand shaped by varying consumer health priorities and product accessibility across these geographies.

Among all regions, North America emerges as the dominating region, accounting for 31.4% of the global market and reaching a value of USD 142.0 Bn, highlighting its strong leadership in overall revenue contribution. The region’s dominant position reflects its established consumer base, broad product penetration, and mature retail availability within the nutrition products industry.

Meanwhile, Europe, Asia Pacific, the Middle East & Africa, and Latin America continue to represent important regional segments of the market, collectively contributing to the broader global expansion and competitive landscape. These regions support market diversification through evolving dietary preferences, expanding health awareness, and increasing accessibility of nutrition-focused products across multiple consumer groups.

The clear leadership of North America (31.4%, USD 142.0 Bn) reinforces its role as the key revenue-generating region within the global Nutrition Products Market, while the presence of other major regions strengthens the market’s international growth structure.

Key Regions and Countries

North America

Europe

Germany

France

The UK

Spain

Italy

Rest of Europe

Asia Pacific

China

Japan

South Korea

India

Australia

Rest of APAC

Latin America

Brazil

Mexico

Rest of Latin America

Middle East & Africa

GCC

South Africa

Rest of MEA

Key Players Analysis

In 2025, Abbott continues to hold a strong strategic position in the global Nutrition Products Market through its well-established nutrition-focused portfolio and broad consumer trust. From an analyst’s viewpoint, the company’s strength lies in its ability to address diverse nutritional needs across age groups and lifestyle requirements, ranging from daily wellness support to specialized nutritional solutions. Its consistent focus on product quality, scientifically structured formulations, and wide consumer acceptance supports stable brand positioning. The company’s disciplined approach to portfolio depth and category relevance allows it to maintain strong visibility in a highly competitive global nutrition landscape.

In 2025, Amway Corp remains a highly influential participant in the global Nutrition Products Market, supported by its strong brand-driven nutrition offerings and direct consumer engagement model. An analyst perspective highlights the company’s advantage in building long-term consumer relationships through personalized wellness-oriented product ecosystems. Its nutrition business benefits from strong loyalty, repeat purchasing behavior, and lifestyle-centric product positioning. This creates sustained demand momentum and reinforces its presence among health-conscious consumers seeking trusted daily nutritional support products.

In 2025, Optimum Nutrition stands out as a performance-focused key player in the global Nutrition Products Market, particularly through its strong identity in active nutrition and wellness categories. From an analyst standpoint, the company’s brand strength is closely tied to credibility, product consistency, and focused consumer appeal among fitness-oriented and health-aware buyers. Its specialized positioning in high-demand nutrition formats supports continued brand relevance and competitive differentiation globally.

Top Key Players in the Market

Abbott.

Amway Corp

Optimum Nutrition

Herbalife International of America, Inc.

Bayer AG

Otsuka Pharmaceutical Co., Ltd.

Danone India.

Himalaya Wellness Company

Cargill, Incorporated

NOW Foods

Nature’s Sunshine Products, Inc.

DuPont

Recent Developments

In March 2025, Amway Corp, which works in nutrition and supplements through Nutrilite, introduced a personalized nutrition platform in Korea, marking an important nutrition product development focused on healthy aging and tailored wellness support. This launch strengthened its science-led nutrition business and expanded personalized product innovation.

In January 2024, Optimum Nutrition, which works in sports nutrition, whey protein, creatine, amino acids, and performance supplements, expanded its active nutrition focus by strengthening its creatine category education and product visibility, including creatine powder, capsules, and gummies across its platform. This 2024 development supported strength and endurance nutrition demand and reinforced its athlete-focused supplement portfolio.

Report Scope