Report Overview

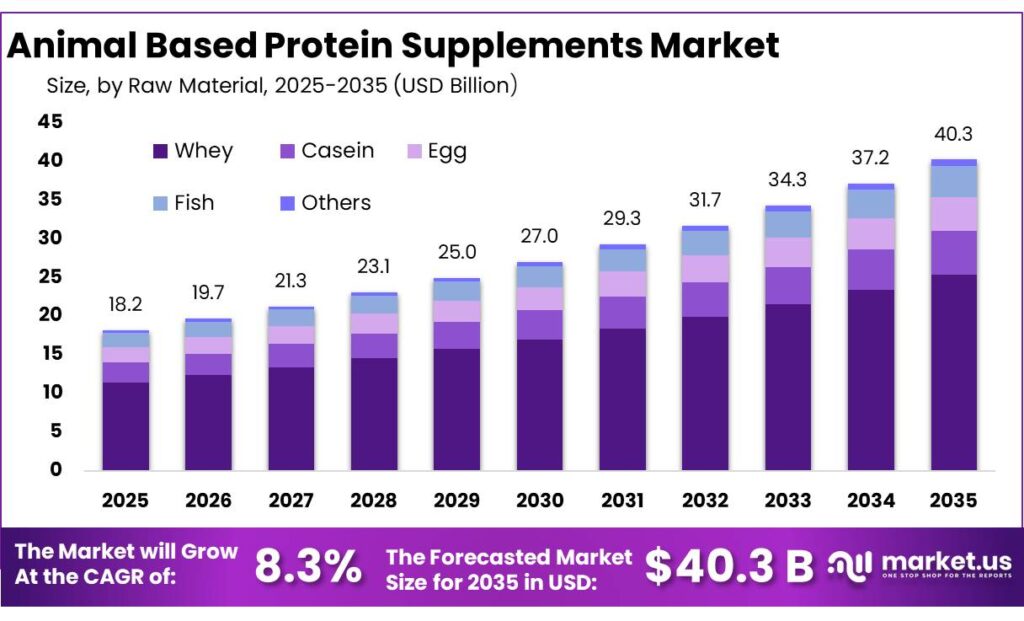

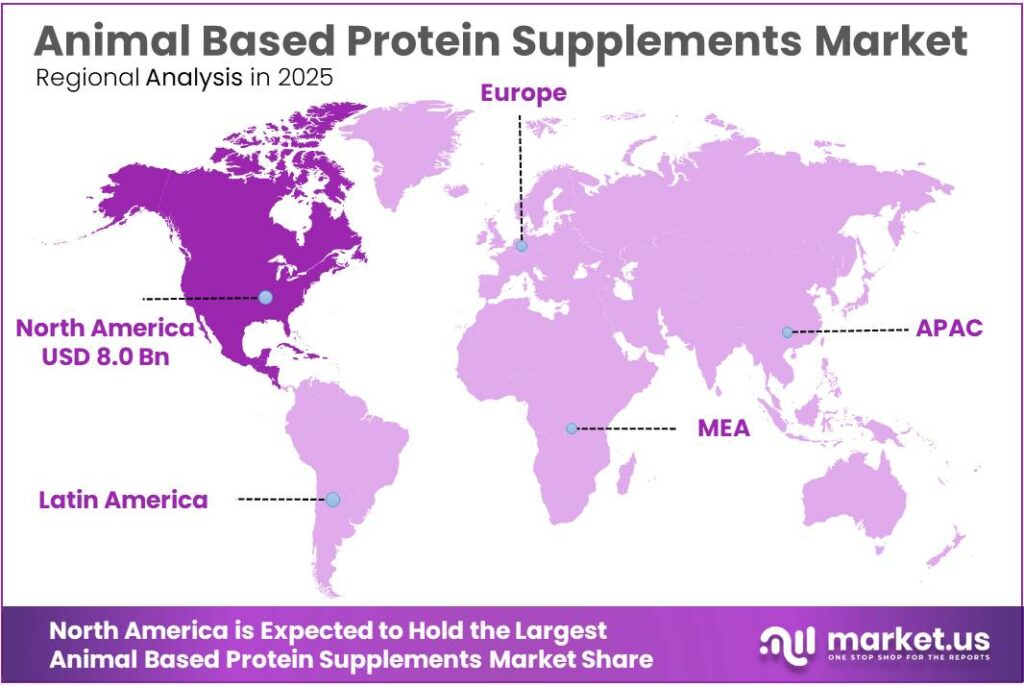

The Global Animal Based Protein Supplements Market size is expected to be worth around USD 40.3 Billion by 2035, from USD 18.2 Billion in 2025, growing at a CAGR of 8.3% during the forecast period from 2026 to 2035. In 2025, North America held a dominant market position, capturing more than a 44.5% share, holding USD 8.0 Billion revenue.

Animal-based protein supplements, led by whey, casein, collagen, and egg protein, remain a strategically important segment within functional nutrition because they sit at the intersection of sports nutrition, active aging, clinical nutrition, and fortified everyday foods. The World Health Organization has set the adult estimated average protein requirement at 0.66 g/kg/day, while WHO guidance for healthy older persons indicates 0.9–1.1 g/kg/day, reinforcing a clear nutritional case for high-quality, efficient protein delivery formats.

From an industrial standpoint, the category is supported by a large and still-expanding animal-protein supply chain. The OECD-FAO Agricultural Outlook 2025-2034 projects global agricultural production value to reach USD 3.96 trillion by 2034, with livestock production expected to rise 16% over the decade. In parallel, world meat production is projected to increase 13%, or 46 million tonnes carcass-weight equivalent, to 406 million tonnes by 2034. The same outlook notes that the output of meat, dairy products, and eggs is expected to increase 17% through 2034.

Dairy remains the most commercially important input stream, particularly for whey and casein-based supplementation. OECD-FAO states that roughly 30% of global milk will be further processed into products such as cheese, powders, and whey powder over the coming decade. In the United States, USDA reported in January 2026 production of 77.4 million pounds of dry whey, up 7.5% year over year, and 40.2 million pounds of whey protein concentrate, up 4.3%.

The main growth drivers are performance nutrition, aging demographics, premiumization, and format diversification into RTDs, bars, medical nutrition, and mainstream high-protein foods. Trade momentum also supports the category. According to IDFA, using USDA-released calendar-year data, U.S. dairy exports reached USD 9.51 billion in 2025, up 15% from 2024. USDEC separately reported USD 9.63 billion in 2025 export value and 2.32 million metric tons of dairy export volume, up 4% year over year.

Glanbia plc reported a robust 2025 performance with adjusted EPS of 134.93 US cents, while also disclosing that agreement was reached in November 2025 to acquire Scicore Nutra. At its 2025 Capital Markets Day, Glanbia also stated that Optimum Nutrition’s protein powder share rose from 30.6% in 2022 to 37.7% in 2025, highlighting brand strength in premium whey-led supplementation.

Key Takeaways

Animal Based Protein Supplements Market size is expected to be worth around USD 40.3 Billion by 2035, from USD 18.2 Billion in 2025, growing at a CAGR of 8.3%.

Whey held a dominant market position, capturing more than a 63.7% share in the animal based protein supplements market.

Protein Powder held a dominant market position, capturing more than a 65.8% share.

Sports Nutrition held a dominant market position, capturing more than a 68.9% share.

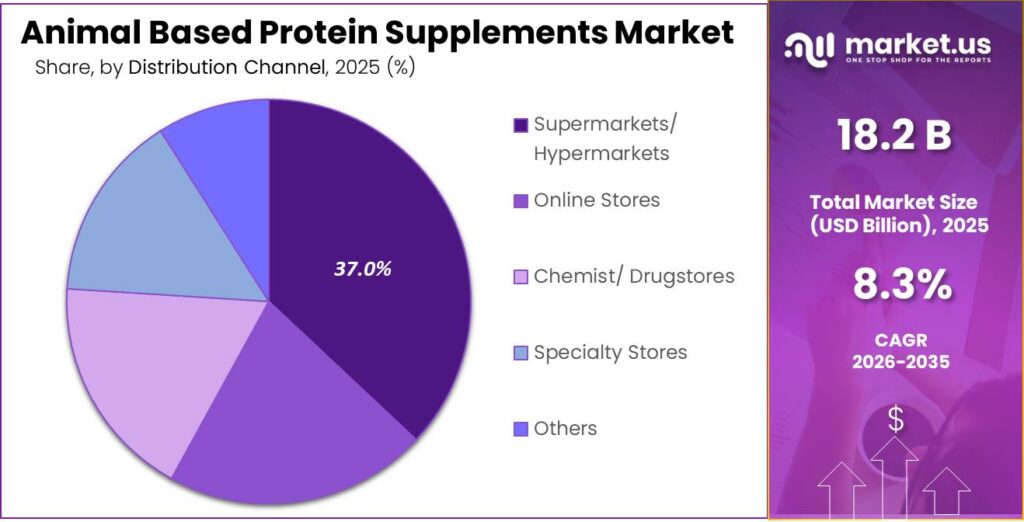

Supermarkets/ Hypermarkets held a dominant market position, capturing more than a 37.2% share.

North America held the leading position in the animal based protein supplements market in 2025, accounting for 44.5% of the global market and reaching a value of USD 8.0 billion.

By Raw Material Analysis

Whey dominates with 63.7% share in 2025, supported by strong sports nutrition demand and everyday protein use.

In 2025, Whey held a dominant market position, capturing more than a 63.7% share in the animal based protein supplements market by raw material segment. This leadership was mainly supported by its strong reputation as a fast-absorbing and high-quality protein source, widely preferred by fitness enthusiasts, athletes, and regular health-conscious consumers. Its rich essential amino acid profile, especially branched-chain amino acids that support muscle recovery and strength development, continued to make it the first choice across protein powders, ready-to-drink shakes, and nutrition bars.

By Product Analysis

Protein Powder leads the market with 65.8% share in 2025, driven by convenience, daily fitness use, and easy product availability.

In 2025, Protein Powder held a dominant market position, capturing more than a 65.8% share in the animal based protein supplements market by product. This segment remained the preferred choice among consumers because it offers a simple and flexible way to meet daily protein needs across different lifestyles. From gym users and athletes to working professionals and older adults focused on maintaining strength, protein powder continued to see broad acceptance in everyday nutrition routines. Its popularity was further supported by the wide variety of pack sizes, flavors, and formulations available for muscle gain, recovery, weight management, and general wellness.

By Application Analysis

Sports Nutrition stands strong with 68.9% share in 2025, backed by rising fitness goals and performance-focused supplement use.

In 2025, Sports Nutrition held a dominant market position, capturing more than a 68.9% share in the animal based protein supplements market by application. This segment continued to lead as protein supplementation became a core part of workout, endurance, and recovery routines for a wide consumer base. Demand remained especially strong among athletes, gym-goers, bodybuilders, and individuals following active lifestyles, all of whom increasingly relied on animal-based protein products to support muscle repair, strength building, and faster post-exercise recovery. The strong presence of whey, casein, and collagen-based formulations across pre-workout, post-workout, and recovery nutrition further supported segment growth in 2025.

By Distribution Channel Analysis

Supermarkets/Hypermarkets lead with 37.2% share in 2025, helped by easy access, shelf visibility, and trusted in-store buying.

In 2025, Supermarkets/ Hypermarkets held a dominant market position, capturing more than a 37.2% share in the animal based protein supplements market by distribution channel. This segment remained a key sales channel because consumers continued to prefer buying nutrition products from stores where they could easily compare brands, pack sizes, flavors, and price options in person. The strong shelf presence of protein powders, ready-to-drink shakes, and nutrition bars in organized retail outlets helped drive frequent purchases, especially among regular household shoppers.

Key Market Segments

By Raw Material

Whey

Casein

Egg

Fish

Others

By Product

Protein Powder

Protein Bars

Ready-to-Drink

Others

By Application

Sports Nutrition

Functional Food

By Distribution Channel

Supermarkets/ Hypermarkets

Online Stores

Chemist/ Drugstores

Specialty Stores

Others

Emerging Trends

Ready-to-drink and small-format high-protein beverages are becoming the biggest trend in animal-based supplements

One of the most visible latest trends in the animal based protein supplements market is the fast rise of ready-to-drink (RTD) shakes, protein coffees, and small-format dairy beverages. In 2025, consumers are moving toward quick, portable nutrition that fits busy routines, especially for breakfast replacement, post-workout recovery, and office snacking. This trend is strongly supported by dairy industry updates showing that demand for high-quality protein foods continues to surge, with buying patterns increasingly shifting toward convenient drinkable formats.

A strong real-world signal comes from the dairy sector, where organic dairy grew by 9.8% in 2024, much faster than historical growth levels, as high-protein milk drinks, kefir, and filtered dairy beverages gained popularity. This is directly benefiting whey and milk-protein-based supplement brands, which are launching lactose-filtered RTDs, clear whey drinks, and protein-rich yogurt beverages.

Functional animal proteins for beauty, gut health, and healthy aging are expanding beyond sports nutrition

Another major latest trend is the expansion of animal-based proteins into beauty wellness, gut health, and healthy aging products. In 2025, collagen peptides, bone broth proteins, and dairy proteins are increasingly being used not just for muscle recovery but also for skin health, joint mobility, digestion, and senior nutrition support. This trend is being driven by consumers looking for “more than muscle” benefits from their supplements.

Recent industry updates also show that dairy proteins are gaining stronger preference because of their complete amino acid profile and clean-label appeal, especially in yogurts, RTDs, and functional wellness drinks. At the same time, health-focused dairy innovation continues to rise through probiotic protein drinks and gut-friendly cultured beverages, which combine protein with digestive benefits.

Drivers

Rising sports participation and active lifestyle habits are strongly pushing demand for animal-based protein supplements

One of the biggest growth drivers for animal based protein supplements is the sharp rise in sports participation, gym activity, and everyday fitness awareness. In 2025, more consumers are focusing on strength, recovery, and lean muscle support, which naturally increases the use of whey, casein, collagen, and other animal-derived proteins. This trend is no longer limited to professional athletes. Office workers, students, older adults, and people following weight management plans are also adding protein supplements to their daily routine.

At the same time, dairy remains one of the most trusted raw material bases for supplement brands. The OECD-FAO Agricultural Outlook 2025–2034 also highlighted that global dairy consumption is expected to continue rising over the medium term as income and population grow, directly supporting whey and milk protein ingredient demand.

Government nutrition programs and healthy diet affordability initiatives are increasing protein-focused consumption

Another major driver is the growing support from governments and global food organizations toward better nutrition access and protein-rich diets. In 2025, several public health and food security programs are placing stronger focus on nutrient-dense foods, especially protein sources that support child growth, healthy aging, and recovery from malnutrition. According to the FAO, IFAD, UNICEF, WFP, and WHO joint State of Food Security and Nutrition in the World 2025, data from 178 countries is now being tracked through centralized dietary systems, while 59 household consumption surveys across 34 countries were used to assess food and nutrient intake patterns.

These numbers clearly show how governments and global institutions are investing more in nutrition monitoring and healthy diet accessibility. Such initiatives indirectly support the animal based protein supplements market, as trusted proteins like whey and casein are increasingly used in fortified foods, clinical nutrition, sports recovery, and age-related muscle health.

Restraints

Lactose intolerance and dairy sensitivity are limiting repeat use of animal-based protein supplements

One major restraining factor for the animal based protein supplements market is the growing concern around lactose intolerance, milk sensitivity, and digestive discomfort linked to dairy-based proteins such as whey and casein. A large share of animal protein supplements still depends on milk-derived raw materials, which creates a challenge in markets where lactose digestion issues are common. According to global health nutrition studies referenced by leading food organizations, around 65% of the world’s population experiences some level of lactose malabsorption, making dairy-heavy supplement use difficult for many adults.

In 2025, this remains an important restraint because even fitness-focused consumers often shift away after experiencing bloating, gas, or stomach discomfort from whey concentrates and blended dairy proteins. Trusted food and nutrition guidance from FAO also highlights milk allergy and intolerance as important dietary limitations in dairy consumption.

Stricter allergen labeling and consumer caution are reducing category accessibility

Another strong restraint comes from rising allergen awareness and stricter food labeling regulations around milk proteins. Government-backed agencies such as the U.S. FDA continue to enforce mandatory milk allergen disclosure on packaged foods and beverages, including protein powders and ready-to-drink supplements. While this improves consumer safety, it also increases caution among buyers who have even mild dairy sensitivities. Clinical nutrition studies show that cow’s milk allergy affects nearly 2% of infants and 4.5% of children, and these concerns often continue into family-level food buying decisions.

In 2025, this creates a wider hesitation around animal-derived supplements, particularly among households purchasing shared nutrition products for teenagers, adults, and older consumers. Brands must spend more on clear labeling, allergen-safe production, and education, which can increase costs and reduce impulse purchases.

Opportunity

Healthy aging nutrition needs are creating a strong growth opportunity for animal-based protein supplements

One of the biggest growth opportunities for the animal based protein supplements market is the rapidly growing need for healthy aging nutrition. As the global older adult population rises, the demand for high-quality, easy-to-digest proteins is increasing in daily diets, recovery nutrition, and muscle maintenance products. Trusted nutrition research published in 2025 shows that healthy older adults need at least 1.0–1.2 g of protein per kg of body weight per day, while those with acute or chronic health conditions may require 1.2–1.5 g/kg/day, and in severe cases even up to 2.0 g/kg/day.

Governments and public health nutrition bodies are also putting stronger focus on sarcopenia prevention and healthy longevity, which further supports the use of premium animal proteins. Because aging consumers often prefer convenient powders and ready-to-drink products, this segment offers strong room for expansion through 2026.

Clinical nutrition and senior care programs are expanding future demand potential

A second major opportunity comes from the expansion of clinical nutrition, hospital recovery, and government-supported elderly care programs. Public health systems are increasingly focusing on preventing frailty, falls, and age-related muscle loss, all of which depend heavily on sufficient protein intake. According to 2025 nutrition evidence, 25–30 g of protein per meal is considered an effective intake target to maximize muscle protein synthesis in older adults.

FAO nutrition guidance also continues to support milk and dairy proteins as highly bioavailable sources in human nutrition, strengthening confidence in whey and casein use across medical and wellness categories. In 2026, this is expected to open new product development opportunities in high-protein meal replacements, therapeutic recovery drinks, and specialized supplements for seniors with low appetite or poor nutrient absorption.

Regional Insights

North America dominates the animal based protein supplements market with 44.5% share, reaching USD 8.0 billion in 2025

North America held the leading position in the animal based protein supplements market in 2025, accounting for 44.5% of the global market and reaching a value of USD 8.0 billion. The region’s dominance is strongly linked to its advanced sports nutrition culture, high daily protein consumption awareness, and a well-established dairy ingredient supply chain. The United States remained the key revenue contributor, supported by large-scale whey and milk protein production capacity.

According to USDA dairy product data, the U.S. produced 495 million pounds of whey protein concentrate in 2024, providing a strong raw material base that continued to support supplement manufacturing growth in 2025.

Another major factor supporting North America’s leadership is strong demand from fitness users, healthy aging consumers, and clinical nutrition applications. Protein powders, ready-to-drink shakes, collagen drinks, and recovery blends have become mainstream across supermarkets, specialty nutrition stores, pharmacies, and online retail platforms.

Key Regions and Countries Insights

North America

Europe

Germany

France

The UK

Spain

Italy

Rest of Europe

Asia Pacific

China

Japan

South Korea

India

Australia

Rest of APAC

Latin America

Brazil

Mexico

Rest of Latin America

Middle East & Africa

GCC

South Africa

Rest of MEA

Key Players Analysis

Glanbia plc remains one of the strongest players in the animal based protein supplements market, supported by its globally recognized Optimum Nutrition brand and deep whey protein ingredient expertise. In 2025, the company reported USD 3.9 billion in total revenue, reflecting 2.3% growth, while its Performance Nutrition division generated nearly USD 1.8 billion, accounting for a major share of sports and whey-based supplement sales.

Abbott Laboratories is a major force in the broader clinical and adult nutrition space, which strongly supports its animal protein supplement presence through brands focused on muscle health, recovery, and senior nutrition. In full-year 2025, Abbott’s global Nutrition segment reported USD 8.45 billion in sales, including USD 4.48 billion from adult nutrition alone. This large-scale nutrition business gives Abbott a strong advantage in high-protein medical drinks, hospital recovery formulas, and muscle-support products for aging consumers.

CytoSport, Inc., widely known for its Muscle Milk brand, holds a strong position in ready-to-drink animal protein beverages and whey-based powders. The company has built strong market visibility through convenient 25g–40g protein RTD formats, making it highly popular among gym users, busy professionals, and meal-replacement consumers. Its numeric strength lies in high per-serving protein delivery and broad retail presence across supermarkets, convenience stores, and fitness outlets.

Top Key Players Outlook

Glanbiaplc

MusclePharm Corporation

Abbott Laboratories

CytoSport, Inc.

Iovate Health Sciences International Inc.

QuestNutrition

THE BOUNTIFUL COMPANY

AMCO Proteins

NOW Foods

Transparent Labs

WOODBOLT DISTRIBUTION LLC

Recent Industry Developments

In 2025, Glanbia plc strengthened its position in the animal based protein supplements sector through its strong performance nutrition and whey ingredient business, led by brands such as Optimum Nutrition and Isopure. The company’s total revenue reached USD 3.9 billion in FY 2025, up 2.3% year over year, while its Performance Nutrition segment delivered 4.5% like-for-like growth, showing solid demand for whey protein powders, RTD shakes, and muscle recovery products.

In 2025, CytoSport, Inc. continued to hold a strong position in the animal based protein supplements sector through its Muscle Milk ready-to-drink shakes and whey protein powders, with the brand remaining especially strong in convenience-led sports nutrition. From a market research perspective, CytoSport’s biggest strength is its leadership in RTD protein beverages delivering 25g, 32g, and 40g protein per serving, which keeps the brand highly relevant among gym users, working professionals, and meal-replacement consumers.

Report Scope

Partners with Superpower on Diagnostics and Supplements")