Report Overview

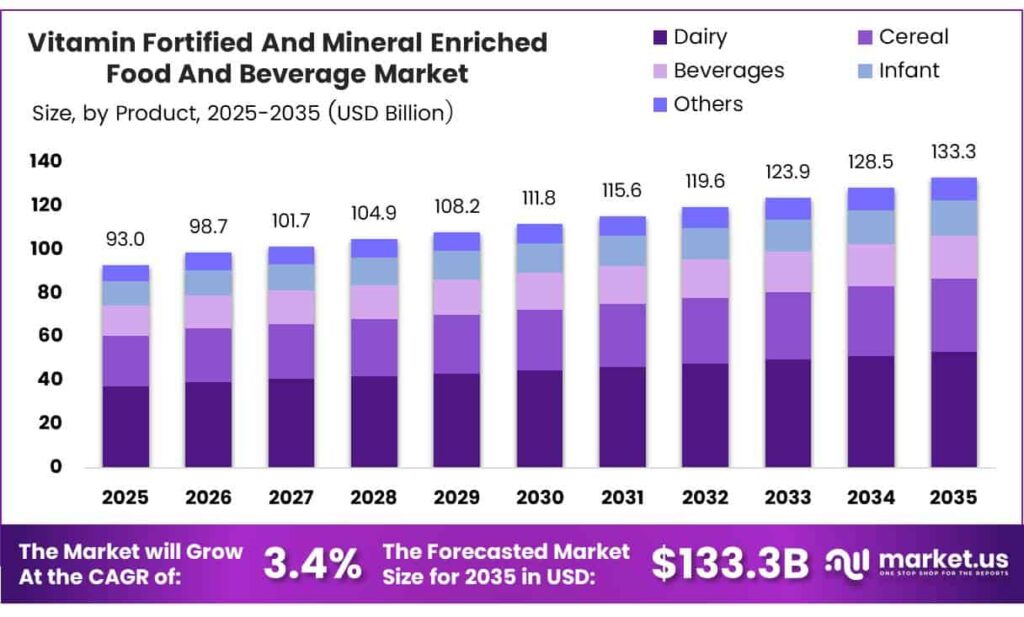

The Global Vitamin Fortified and Mineral Enriched Food and Beverage Market size is expected to be worth around USD 133.3 billion by 2035 from USD 93.0 billion in 2025, growing at a CAGR of 3.4% during the forecast period 2026 to 2035.

The vitamin-fortified and mineral-enriched food and beverage market covers products that manufacturers enhance with added vitamins, minerals, and micronutrients. These products help consumers meet daily nutritional requirements. Dairy items, cereals, beverages, and infant formulas represent the core product categories driving this market forward.

Consumer awareness about preventive healthcare continues to reshape purchasing decisions globally. Shoppers increasingly seek functional nutrition that delivers health benefits beyond basic calories. Consequently, food and beverage brands invest heavily in developing enriched product lines that combine convenience with measurable nutritional value.

Nestlé’s Annual Report recorded total sales of CHF 91.4 billion in FY2024, reflecting the scale of demand for fortified nutrition, infant formula, and micronutrient-enriched beverages globally. This revenue base underscores how essential enriched food products have become within mainstream consumer consumption patterns.

PepsiCo’s company generated net revenue of USD 91.9 billion, including sales from fortified cereals, Quaker oat products, and functional beverages. These figures demonstrate how leading multinationals increasingly rely on nutrient-enriched portfolios to sustain revenue growth in competitive global markets.

Investment in research and innovation strengthens product development pipelines across the industry. Manufacturers collaborate with nutrition scientists to identify micronutrient gaps in consumer diets. Moreover, ingredient technology advances allow brands to fortify products without compromising taste, texture, or shelf life.

Key Takeaways

The Global Vitamin Fortified and Mineral Enriched Food and Beverage Market is valued at USD 93.0 billion in 2025 and is projected to reach USD 133.3 billion by 2035, at a CAGR of 3.4%.

Dairy products hold the dominant share at 28.4% in 2025.

Conventional products lead the segment with a 72.5% market share.

Bottle packaging dominates with a 37.8% share.

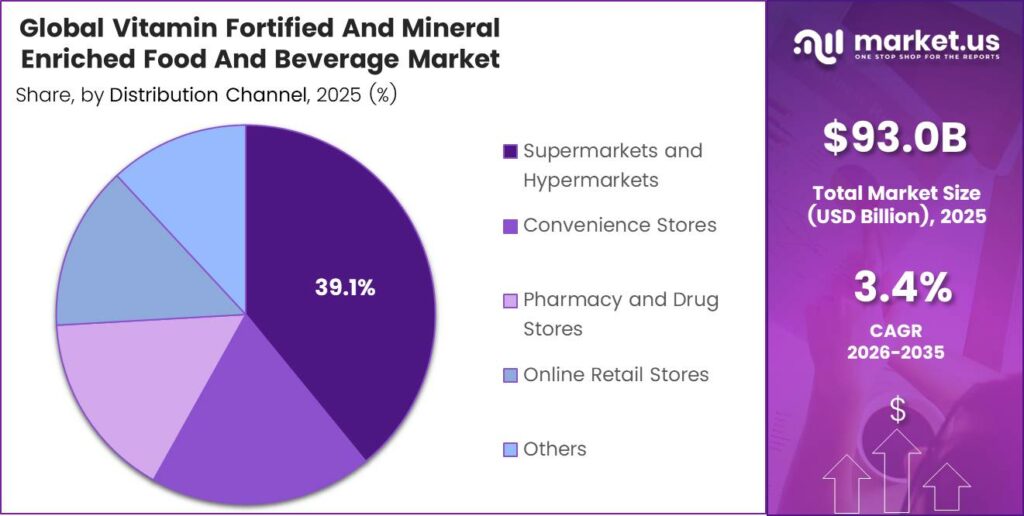

Supermarkets and Hypermarkets hold the largest share at 39.1%.

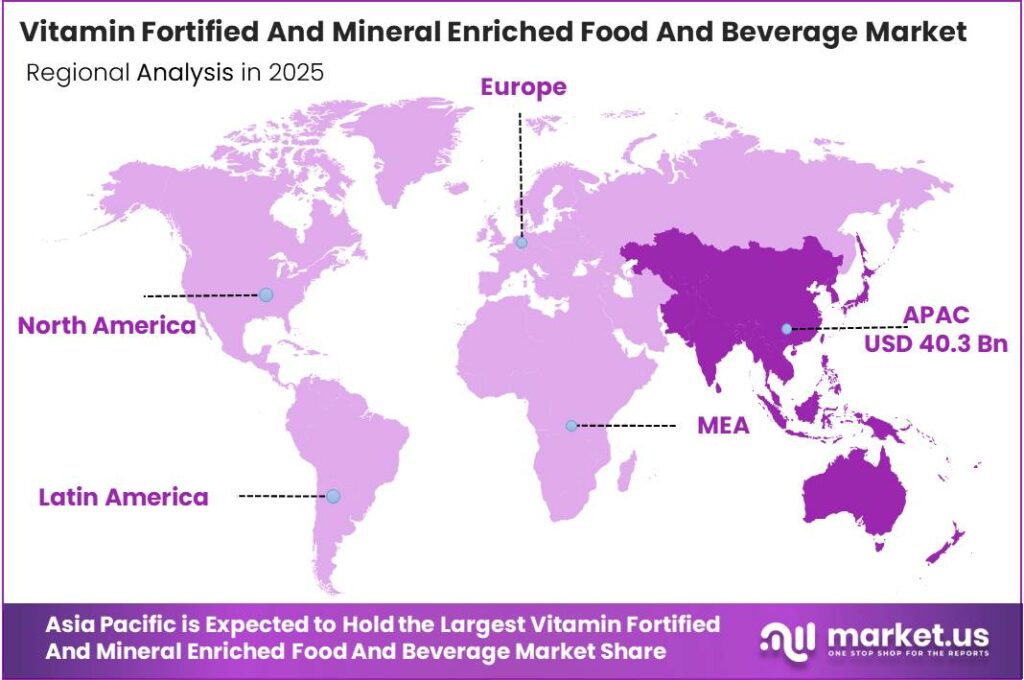

Asia Pacific dominates the regional landscape with a 43.3% share, valued at USD 40.3 billion.

By Product Type Analysis

Dairy products dominate with 28.4% due to widespread consumer trust and fortification compatibility.

In 2025, Dairy Products held a dominant market position in the By Product Type segment of the Vitamin Fortified and Mineral Enriched Food and Beverage Market, with a 28.4% share. Dairy products offer ideal matrices for adding vitamins D, A, and calcium. Moreover, strong consumer familiarity drives consistent retail demand across both developed and emerging markets.

Cereal Based Products represent a significant and fast-growing sub-segment within the fortified food market. Breakfast cereals and grain-based snacks serve as common vehicles for iron, B vitamins, and zinc fortification. Consequently, manufacturers expand cereal portfolios to target health-conscious consumers seeking convenient daily nutrition solutions.

Beverages form a rapidly evolving sub-segment, attracting innovation in functional hydration and vitamin-infused drink formats. Sports drinks, juices, and plant-based milk alternatives increasingly carry enriched nutrient profiles. Therefore, beverages attract strong investment from both large multinationals and emerging health-focused brands targeting active lifestyle consumers.

By Nature Analysis

Conventional products dominate with 72.5% due to affordability, scale, and wide retail availability.

In 2025, Conventional products held a dominant market position in the By Nature segment of the Vitamin Fortified and Mineral Enriched Food and Beverage Market, with a 72.5% share. Conventional fortified products offer affordability and mass-market scalability. Moreover, established manufacturing infrastructure allows brands to reach broad consumer bases across global retail channels efficiently.

Organic and Natural fortified food and beverages represent the fastest-growing sub-segment within this category. Consumers increasingly associate organic certification with safety, sustainability, and superior ingredient quality. Consequently, premium retail channels and e-commerce platforms drive strong growth in organic fortified products, particularly among urban, health-aware consumer segments.

By Packaging Type Analysis

Bottle packaging dominates with 37.8% due to strong appeal in beverage and liquid supplement categories.

In 2025, Bottle packaging held a dominant market position in the By Packaging Type segment of the Vitamin Fortified and Mineral Enriched Food and Beverage Market, with a 37.8% share. Bottle formats provide convenience, portability, and excellent product visibility on retail shelves. Additionally, glass and PET bottle options support diverse fortified beverage and liquid supplement product lines globally.

Box packaging serves as the primary format for cereal-based and dry fortified food products across global markets. Cardboard box formats offer cost efficiency and a strong branding surface area for nutritional labeling. Therefore, manufacturers of breakfast cereals, protein powders, and dry fortified snacks consistently prefer this packaging solution for retail distribution.

Tetrapack packaging supports long shelf life and hygienic storage for liquid fortified products such as juices and plant-based milk. This format suits markets with limited cold chain infrastructure, making it valuable in developing economies. Moreover, Tetrapack’s recyclability appeals to environmentally conscious consumers and brands prioritizing sustainable packaging goals.

By Distribution Channel Analysis

Supermarkets and Hypermarkets dominate with 39.1% due to broad product access and consumer footfall.

In 2025, Supermarkets and Hypermarkets held a dominant market position in the By Distribution Channel segment of the Vitamin Fortified and Mineral Enriched Food and Beverage Market, with a 39.1% share. These retail formats offer a wide product assortment and high daily footfall. Consequently, fortified food and beverage brands prioritize shelf space in supermarkets to maximize consumer reach and brand visibility.

Convenience Stores provide quick purchase access for on-the-go fortified snacks, drinks, and single-serve products. Urban consumers increasingly rely on convenience stores for daily nutritional top-up purchases. Moreover, strategic product placements near checkout zones help brands drive impulse purchases of vitamin-enriched energy drinks and fortified snack bars.

Pharmacy and Drug Stores serve as a trusted channel for science-backed fortified nutrition products targeting specific health conditions. Consumers seeking medically recommended supplements and enriched formulas prefer pharmacy channels for credibility. Additionally, pharmacist recommendations strengthen consumer confidence in fortified food and beverage purchases made through this specialized retail environment.

Key Market Segments

By Product Type

Dairy Products

Cereal-Based Products

Beverages

Infant Formulas

Others

By Nature

Conventional

Organic and Natural

By Packaging Type

Bottle

Box

Tetrapack

Others

By Distribution Channel

Supermarkets and Hypermarkets

Convenience Stores

Pharmacy and Drug Stores

Online Retail Stores

Others

Emerging Trends

Wellness-Focused Botanicals and Low-Sugar Formulations Gain Consumer Momentum

Consumers increasingly choose low-sugar, botanical, and floral-infused fortified beverages that promote calm and functional wellness benefits. Brands reformulate existing products to reduce synthetic content while maintaining enriched nutrient profiles. Keurig Dr Pepper brewer shipments reached 10.4 million units in 2024, reflecting strong consumer adoption of functional single-serve fortified beverage formats across North American markets.

AI-Driven Flavor Innovation and Sustainable Sourcing Reshape Product Development

Food and beverage companies integrate artificial intelligence tools to predict consumer flavor preferences and accelerate personalized product development pipelines. Moreover, brands emphasize traceable and ethical sourcing practices to meet growing demand for transparency in fortified ingredient supply chains. Restaurant and foodservice sector trends further amplify global culinary fusion launches in enriched food and beverage categories.

Drivers

Clean-Label Ingredient Demand and Convenience Food Growth Fuel Market Expansion

Consumer preference for natural and clean-label ingredients reshapes formulation strategies across fortified food and beverage categories globally. Additionally, explosive growth in processed convenience foods and ready-to-eat meals creates sustained demand for vitamin and mineral enrichment. Coca-Cola’s company generated net operating revenues of USD 47.1 billion, supported by fortified juice, dairy, and enhanced beverage portfolios driving category growth.

Rising Disposable Incomes and Flavor Technology Breakthroughs Support Global Demand

Rising global disposable incomes enable consumers to spend more on premium fortified and nutritionally enhanced food products. Furthermore, breakthroughs in flavor extraction technologies allow manufacturers to develop complex, customized taste profiles in enriched food formats. International travel also exposes consumers to exotic nutritional products, expanding demand for globally inspired fortified food and beverage innovations.

Restraints

Regulatory Compliance Burdens Create Significant Market Entry Barriers

Stringent regulatory mandates governing synthetic additive usage limit formulation flexibility for manufacturers across global markets. Compliance with food safety laws in the US, EU, and Asia Pacific requires extensive testing, labeling, and approval processes. Kraft Heinz’s company returned USD 2.7 billion to shareholders, reflecting financial pressure from managing regulatory costs within packaged nutrition and enriched food operations.

Raw Material Volatility and Supply Chain Disruptions Constrain Production Economics

Persistent price volatility in natural raw materials creates unpredictable production costs for vitamin and mineral-enriched food manufacturers. Supply chain disruptions from climate events, geopolitical tensions, and logistics bottlenecks further impact ingredient availability. Consequently, manufacturers face margin pressure when sourcing botanical extracts, vitamins, and mineral compounds from geographically concentrated supply regions worldwide.

Growth Factors

Functional Foods and Plant-Based Alternatives Drive High-Value Product Innovation

Functional food and beverage categories integrating health-promoting botanical ingredients attract strong consumer and investor interest globally. Simultaneously, the surge in plant-based dairy alternatives creates significant demand for specialized fortification systems that replicate the nutritional profiles of conventional dairy. Keurig Dr Pepper’s net sales reached USD 15.4 billion, reflecting strong exposure to enhanced hydration and vitamin beverage growth formats.

Premium Snack Expansion and Emerging Market Penetration Accelerate Revenue Growth

Premium snack brands and gourmet food producers increasingly differentiate through high-margin fortified ingredient innovations that command consumer price premiums. Moreover, urbanization across Asia-Pacific and Latin America fuels middle-class demand for packaged, enriched, and convenience-oriented food and beverage products. Consequently, market participants aggressively expand distribution networks and localized product portfolios across these high-growth emerging economy regions.

Regional Analysis

Asia Pacific Dominates the Vitamin Fortified and Mineral Enriched Food and Beverage Market with a Market Share of 43.3%, Valued at USD 40.3 Billion

Asia Pacific holds the leading position in the global market, commanding a 43.3% share valued at USD 40.3 billion in 2025. Rapid urbanization, a large and growing middle-class population, and government-mandated fortification programs in countries like China, India, and Indonesia drive this dominance. Additionally, rising health awareness and organized retail expansion further accelerate regional market growth.

North America represents a mature and high-value market for vitamin-fortified and mineral-enriched food and beverage products. Strong consumer health consciousness, advanced retail infrastructure, and a robust regulatory framework for fortified nutrition drive consistent demand. Moreover, innovation in functional beverages and clean-label enriched products sustains market momentum across the United States and Canada.

Europe maintains a strong market presence for fortified food and beverage products, driven by stringent nutritional standards and consumer preference for organic and natural enriched options. Germany, France, and the United Kingdom lead regional consumption. Additionally, EU-level regulatory harmonization supports cross-border trade in compliant fortified nutrition products throughout the region.

The Middle East and Africa market demonstrates steady growth potential, supported by government public health programs targeting micronutrient deficiency across large populations. Rising urbanization and improving retail infrastructure expand access to enriched food and beverage products. Furthermore, international brand entry into GCC markets and South Africa supports growing consumer demand for premium fortified nutrition options.

Key Regions and Countries

North America

Europe

Germany

France

The UK

Spain

Italy

Rest of Europe

Asia Pacific

China

Japan

South Korea

India

Australia

Rest of APAC

Latin America

Brazil

Mexico

Rest of Latin America

Middle East & Africa

GCC

South Africa

Rest of MEA

Key Players Analysis

Abbott Laboratories stands as a globally recognized leader in science-based nutrition, delivering fortified products across infant, pediatric, and adult health segments. The company’s nutrition division develops clinically validated enriched formulas that address specific micronutrient deficiencies. Moreover, Abbott’s strong presence in hospital and pharmacy channels reinforces its authority in the therapeutic and functional fortified nutrition space worldwide.

Kellanova operates a broad portfolio of fortified cereal and snack brands that serve health-conscious consumers across global retail channels. The company consistently invests in nutritional fortification innovation, particularly within breakfast cereal and grain-based snack categories. Consequently, Kellanova maintains a strong market position by combining functional nutrition credentials with high-volume distribution across North American and international markets.

Nestlé SA commands one of the most extensive fortified food and beverage portfolios globally, spanning infant formula, dairy, cereals, and enriched beverages. The company integrates micronutrient science into product development across all major consumer segments and geographies. Additionally, Nestlé’s research and development investments continuously improve the bioavailability and sensory appeal of its vitamin and mineral-enriched product range.

PepsiCo, Inc. leverages its diversified food and beverage portfolio to deliver fortified nutrition through brands spanning cereals, sports drinks, and functional snacks. The company’s Quaker Oats and Gatorade lines represent key vehicles for vitamin and mineral enrichment across mass-market channels. Furthermore, PepsiCo actively expands its health-oriented product lines to respond to shifting consumer preferences for nutritionally enhanced food and beverage options.

Top Key Players in the Market

Abbott Laboratories

Kellanova

Nestlé SA

PepsiCo, Inc.

The Coca-Cola Company

The Hain Celestial Group

Amway Corporation

General Mills Inc.

Danone SA

Kraft Heinz Company

Monster Beverage Corporation

HiPP GmbH

Perrigo Company

Reckitt Benckiser Group

Glanbia Plc

Recent Developments

In 2025, Abbott Nutrition continues to maintain and update its portfolio of science-based, nutrient-fortified products for nutritional support across life stages. The company published its Adult Product Reference Guide, which details a range of fortified nutrition solutions, including specialized formulas such as EleCare Jr. (amino acid-based nutrition powder for ages 1+, supporting dietary needs with essential nutrients).

In 2025, Kellanova has advanced reformulation and innovation in snacks and cereals with enhanced nutritional profiles, including fortification with vitamins and minerals. The company launched or expanded products such as Kellogg’s Oaties (Original Crunch and Choco Crunch; high in fibre, and a source of B vitamins, iron, and vitamin D), Kellogg’s High Protein Bites, and Kellogg’s Bluey Multigrain cereal (high-fibre recipes fortified with key micronutrients).

Report Scope