")

In recent months, Planet Fitness has been highlighted as undervalued with earnings expected to grow strongly, while also earning top placement on Entrepreneur’s 2026 Fastest-Growing Franchises list after expanding to 2,896 clubs in 2025.

At the same time, major franchise transactions such as the sale of Grand Fitness Partners to Flynn Group underline how large operators continue to commit capital to the Planet Fitness system.

We’ll now examine how this mix of optimistic earnings expectations and franchise expansion recognition may influence Planet Fitness’s existing investment narrative.

We’ve uncovered the 12 dividend fortresses yielding 5%+ that don’t just survive market storms, but thrive in them.

To own Planet Fitness, you need to believe its high volume, low price, franchise model can keep adding clubs and members while maintaining healthy unit economics. The key short term catalyst remains membership and revenue trends after the click to cancel rollout, with the main risk that higher churn lingers. Recent recognition for franchise growth and talk of undervaluation reinforce the existing narrative but do not materially change this near term risk reward balance.

The Grand Fitness Partners sale to Flynn Group looks particularly relevant here. It signals that well capitalized franchise operators are still willing to buy large Planet Fitness portfolios after years of expansion, which supports the idea that franchisee economics remain attractive. That is encouraging for the company’s growth catalyst of continued club openings, even as investors watch closely for any signs that system saturation or weaker unit returns could slow future development.

Yet behind the upbeat growth story, investors should also be aware that persistent churn pressure from easier membership cancellations could…

Read the full narrative on Planet Fitness (it’s free!)

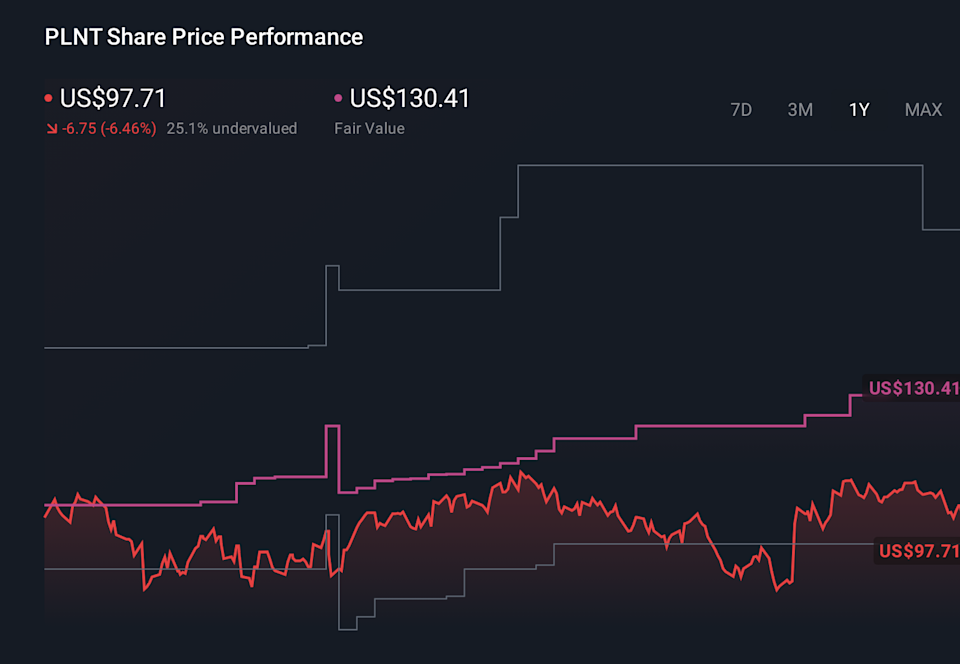

Planet Fitness’ narrative projects $1.6 billion revenue and $312.8 million earnings by 2028.

Uncover how Planet Fitness’ forecasts yield a $130.00 fair value, a 77% upside to its current price.

PLNT 1-Year Stock Price Chart

PLNT 1-Year Stock Price Chart

Some of the most optimistic analysts once projected Planet Fitness revenue reaching about US$1.8 billion and earnings near US$334 million, but the recent churn concerns and member behavior data could challenge those assumptions, so you should compare this bullish view with more cautious scenarios before deciding which narrative you find more convincing.

Explore 4 other fair value estimates on Planet Fitness – why the stock might be worth 49% less than the current price!

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

The market won’t wait. These fast-moving stocks are hot now. Grab the list before they run:

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include PLNT.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com