Although the S&P 500 is down 2.3% over the past six months, Xponential Fitness’s stock price has fallen further to $6.51, losing shareholders 17.9% of their capital. This was partly due to its softer quarterly results and may have investors wondering how to approach the situation.

Is now the time to buy Xponential Fitness, or should you be careful about including it in your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free.

Why Do We Think Xponential Fitness Will Underperform?

Despite the more favorable entry price, we’re cautious about Xponential Fitness. Here are three reasons we avoid XPOF and a stock we’d rather own.

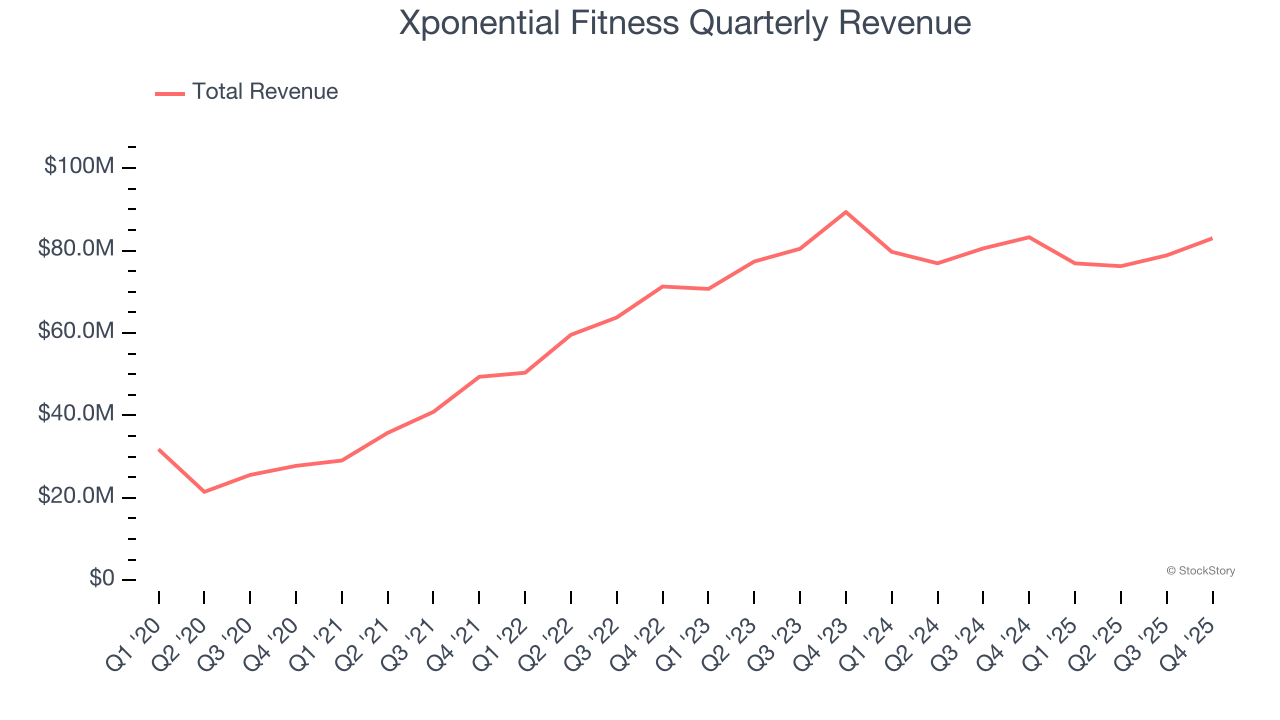

1. Long-Term Revenue Growth Disappoints

Examining a company’s long-term performance can provide clues about its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Over the last five years, Xponential Fitness grew its sales at a 24.2% compounded annual growth rate. Although this growth is acceptable on an absolute basis, it fell slightly short of our standards for the consumer discretionary sector, which enjoys a number of secular tailwinds.

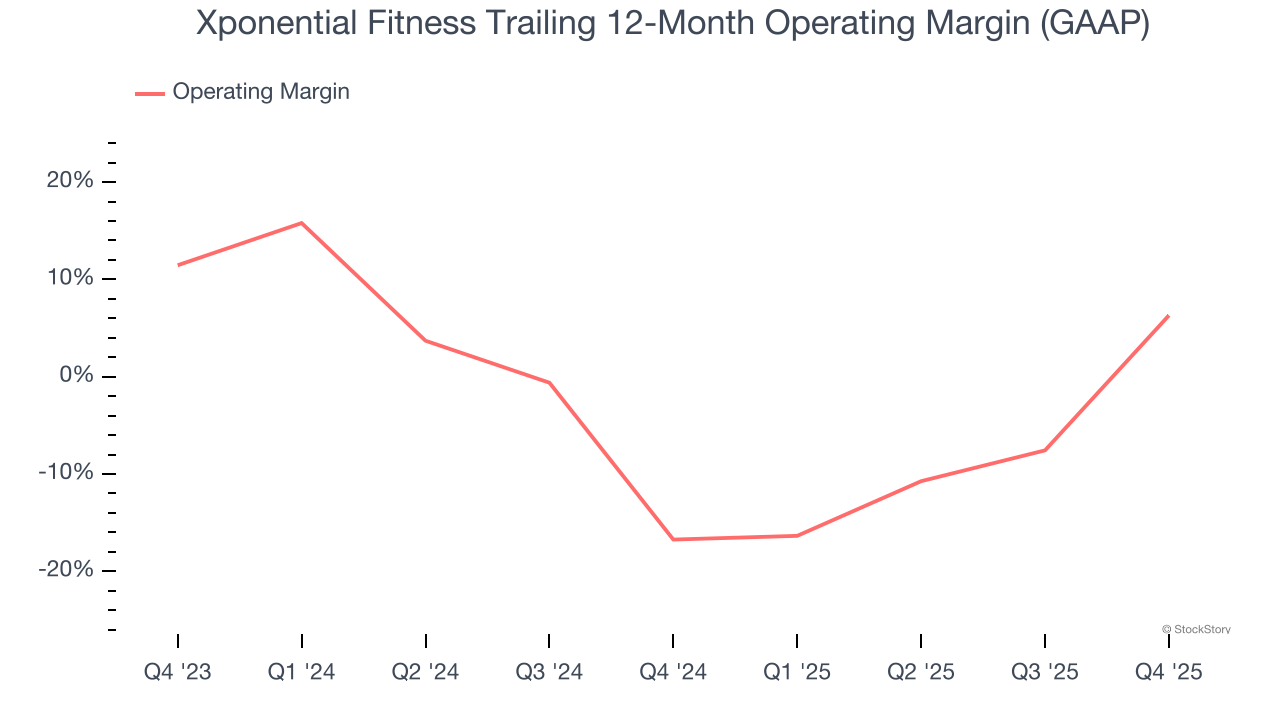

2. Operating Losses Sound the Alarms

2. Operating Losses Sound the Alarms

Operating margin is a key measure of profitability. Think of it as net income – the bottom line – excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Xponential Fitness’s operating margin has risen over the last 12 months, but it still averaged negative 5.3% over the last two years. This is due to its large expense base and inefficient cost structure.

3. Free Cash Flow Projections Disappoint

3. Free Cash Flow Projections Disappoint

Free cash flow isn’t a prominently featured metric in company financials and earnings releases, but we think it’s telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Over the next year, analysts’ consensus estimates show they’re expecting Xponential Fitness’s free cash flow margin of 7.9% for the last 12 months to remain the same.

Final Judgment

Xponential Fitness doesn’t pass our quality test. Following the recent decline, the stock trades at 9.2× forward P/E (or $6.51 per share). While this valuation is optically cheap, the potential downside is huge given its shaky fundamentals. There are better investments elsewhere. We’d recommend looking at one of our top digital advertising picks.

Stocks We Like More Than Xponential Fitness

WHILE YOU’RE HERE: Top 9 Market-Beating Stocks. The best stocks don’t just beat the market once. They do it again. And again. Robust revenue growth, rising free cash flow, returns on capital that leave their competition in the dust. The market has already rewarded these businesses.

But our AI platform says the party isn’t over. Find out which 9 stocks made the cut this week — FREE. Get Our Top 9 Market-Beating Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.