U.S. Vitamin Market Size

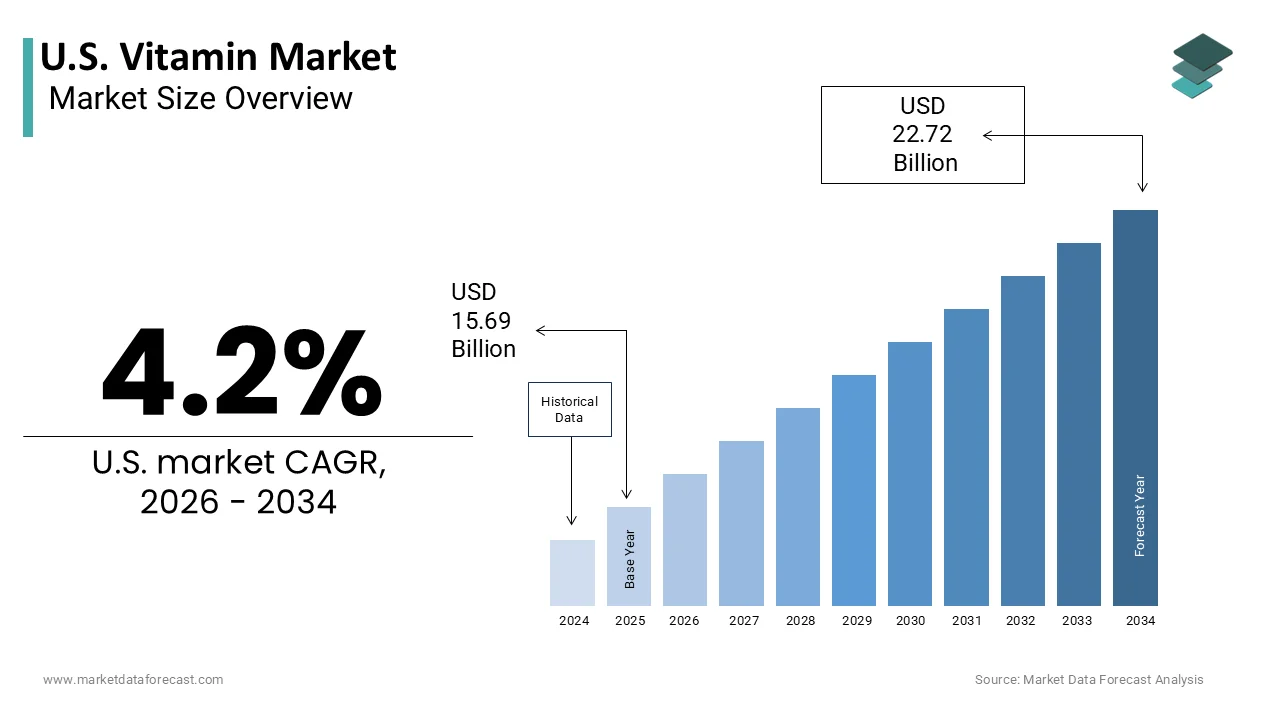

The U.S. Vitamin Market was valued at USD 15.69 billion in 2025, is estimated to reach USD 16.35 billion in 2026, and is projected to reach USD 22.72 billion by 2034, growing at a CAGR of 4.2% from 2026 to 2034.

A vitamin is a type of organic compound that your body needs in very small amounts to function, grow, and develop normally. This market includes a wide array of formulations such as tablets, capsules, gummies, powders, and liquids, catering to diverse demographic needs from pediatric care to geriatric health. Vitamins are classified into water-soluble and fat-soluble categories, each playing distinct roles in metabolic processes, immune function, and cellular repair. According to the Council for Responsible Nutrition, approximately 75 percent of American adults report using dietary supplements, indicating a deeply ingrained culture of preventive health management. As per NHANES data analyzed in the Dietary Guidelines for Americans 2020-2025, more than 90% of the population falls below recommended intakes for vitamin D, potassium, and fiber, which are classified as “nutrients of public health concern” due to their low prevalence in the standard American diet. The market is characterized by a shift toward personalized nutrition, where consumers seek products tailored to their specific genetic profiles, lifestyles, and health goals. Regulatory oversight by the Food and Drug Administration ensures safety and labeling accuracy, although the industry operates under a framework that places responsibility for efficacy largely on manufacturers. The rise of e-commerce has transformed distribution channels, allowing direct-to-consumer brands to bypass traditional retail barriers. Consumer education regarding ingredient transparency and third-party testing has become a critical factor in purchasing decisions. This dynamic landscape requires stakeholders to balance scientific rigor with marketing innovation while navigating complex regulatory environments.

MARKET DRIVERS Rising Prevalence of Chronic Diseases and Preventive Healthcare

The rising prevalence of chronic diseases and the subsequent shift toward preventive healthcare drive the growth of the United States vitamin market. Consumers are increasingly aware of the link between nutritional status and long-term health outcomes, leading to proactive supplementation to mitigate risks associated with conditions such as cardiovascular disease, diabetes, and osteoporosis. According to the CDC’s Fast Facts on Health and Economic Costs (August 2025), chronic and mental health conditions account for 90% of the nation’s $4.9 trillion in annual health care expenditures. As per the American Heart Association, adequate intake of vitamins such as B complex and D is associated with reduced inflammation and improved heart health, driving demand for these specific nutrients. The aging population further amplifies this trend, as older adults require higher levels of certain vitamins to maintain bone density and cognitive function. Healthcare providers are increasingly recommending supplements as part of holistic treatment plans, lending medical credibility to their use. Corporate wellness programs also promote vitamin usage to reduce absenteeism and improve employee productivity. The perception of vitamins as essential tools for maintaining vitality and preventing illness, rather than merely treating deficienc,y creates a robust and sustained demand. This cultural shift toward health optimization ensures that the vitamin market remains resilient and continues to expand as consumers prioritize longevity and quality of life.

Influence of Digital Health and Personalized Nutrition Trends

The influence of digital health technologies and the growing trend toward personalized nutrition greatly fuels the expansion of the United States vitamin market. This enables customized supplement recommendations based on individual data. Advances in genetic testing, microbiome analysis, and mobile health applications allow consumers to identify specific nutritional gaps and receive tailored vitamin regimens. According to the Personalized Medicine Coalition (PMC) (2025), personalized medicines accounted for 38% of new therapeutic drug approvals in 2024, signaling a shift toward molecular-based care. As per sources, personalized nutrition is one of the fastest-growing segments in the wellness industry, with consumers willing to pay a premium for products that address their unique biological needs. Subscription-based models offered by direct-to-consumer brands leverage algorithms to adjust formulations over time, enhancing customer retention and satisfaction. Social media platforms and health influencers play a crucial role in educating consumers about the benefits of targeted supplementation, driving trial and adoption. The integration of wearable devices that track health metrics further reinforces the need for specific nutrients to support performance and recovery. This data-driven approach transforms vitamins from generic commodities into personalized health solutions, increasing their perceived value. The convenience of online consultations and home delivery removes barriers to access, making personalized vitamins accessible to a broader audience. This technological empowerment ensures sustained growth in the market.

MARKET RESTRAINTS Regulatory Ambiguity and Lack of Standardization

Regulatory ambiguity and the lack of standardized efficacy requirements are major restraints to the United States vitamin market. This creates consumer skepticism and limits clinical validation. Unlike pharmaceutical drugs, dietary supplements do not require pre-market approval from the Food and Drug Administration for safety and effectiveness, leading to variability in product quality and potency. According to the Government Accountability Office, investigations have revealed significant discrepancies between labeled ingredients and actual content in some supplement products, undermining consumer trust. As per the Federal Trade Commission, enforcement actions against companies making unsubstantiated health claims are frequent, yet the sheer volume of products makes comprehensive monitoring challenging. The absence of uniform manufacturing standards across all brands results in inconsistent bioavailability and therapeutic effects, confusing consumers who seek reliable health benefits. Healthcare professionals often hesitate to recommend specific brands due to this lack of regulatory rigor, limiting professional endorsement. The complexity of navigating Good Manufacturing Practices compliance poses challenges for smaller manufacturers, potentially leading to market consolidation around larger players with resources for rigorous testing. Consumer confusion regarding terminology such as natural, organic, and clinical strength further complicates purchasing decisions. Until stricter regulatory frameworks are implemented to ensure consistency and transparency, the market will face hurdles in achieving universal credibility. This uncertainty restricts the potential for broader medical integration and limits growth among skeptical demographics.

Scientific Skepticism and Mixed Clinical Evidence

Scientific skepticism and mixed clinical evidence regarding the efficacy of multivitamins are also barriers to the United States vitamin market. This influences consumer behaviour and professional recommendations. Numerous large-scale studies have failed to demonstrate consistent benefits of general multivitamin use in preventing chronic diseases or extending lifespan in healthy populations. According to the US Preventive Services Task Force, current evidence is insufficient to assess the balance of benefits and harms of multivitamin supplementation for the prevention of cardiovascular disease or cancer in asymptomatic adults. As per the Annals of Internal Medicine (2022 update) and the COSMOS Trial (2022-2024), while multivitamins show no significant effect on total mortality or major cardiovascular events in well-nourished individuals, recent data indicate a potential 3.6% reduction in total cancer risk and significant slowing of cognitive aging. These findings are widely publicized in medical journals and mainstream media, leading to questioning of the value proposition of routine supplementation. Healthcare providers may advise patients against unnecessary supplement use, focusing instead on dietary improvements. The perception of vitamins as expensive urine or placebos persists among scientifically literate consumers, reducing willingness to pay for premium products. This evidentiary gap forces manufacturers to invest heavily in clinical trials to substantiate claims, increasing operational costs. The tension between marketing narratives and scientific consensus creates a challenging environment for brand differentiation. Until robust evidence supports broad preventative claims, the market will face resistance from evidence-based practitioners and informed consumers.

MARKET OPPORTUNITIES Expansion of Gummy and Functional Food Formats

The expansion of gummy and functional food formats creates a major opportunity for the United States vitamin market. This appeals to consumers who struggle with traditional pill swallowing and seek enjoyable consumption experiences. Gummies have evolved from pediatric products to mainstream adult supplements, offering a tasty and convenient alternative to tablets and capsules. According to research, gummy vitamins have experienced double-digit growth rates in recent years, outpacing traditional forms in several categories. As per a study, the incorporation of vitamins into everyday foods such as beverages, snacks, and bars allows for seamless integration into daily routines, reducing the perception of supplementation as a chore. The versatility of gummy formats enables manufacturers to combine multiple nutrients and botanicals in appealing flavors, attracting younger demographics and fitness enthusiasts. The aesthetic appeal and portability of gummies make them ideal for on-the-go consumption, aligning with busy lifestyles. Brands are leveraging clean label trends by using natural colors and sweeteners, addressing health concerns associated with sugary confections. The success of gummies has spurred innovation in other chewable and dissolvable formats, expanding the product landscape. Retailers are dedicating more shelf space to these innovative forms, recognizing their high turnover potential. By transforming vitamins into lifestyle products, manufacturers can tap into new consumer segments and drive incremental sales. This format innovation ensures continued market expansion and relevance.

Growth of Plant-Based and Clean Label Supplements

The growth of plant-based and clean-label supplements provides big opportunities for the United States vitamin market. This is in line with the increasing consumer demand for natural and sustainable products. Shoppers are increasingly scrutinizing ingredient lists, preferring vitamins derived from whole food sources rather than synthetic isolates. According to the Organic Trade Association (OTA) 2025 Organic Industry Survey, organic supplement sales grew by roughly 3.4% in 2024, as consumers prioritize transparency and purity despite higher price points compared to conventional options. As per sources, a significant majority of consumers prefer products with recognizable ingredients and no artificial additives, driving manufacturers to reformulate offerings using fruit and vegetable extracts. Plant-based certifications and vegan labels appeal to ethical consumers who avoid animal-derived components such as gelatin capsules. The emphasis on sustainability extends to packaging, with brands adopting recyclable and biodegradable materials to reduce environmental impact. Collaborations with agricultural suppliers ensure traceability and quality control from farm to bottle, enhancing brand credibility. The narrative of holistic health resonates strongly with millennials and Gen Z, who view supplements as part of a broader wellness ecosystem. Retailers highlight clean label products in dedicated sections, facilitating discovery for conscious shoppers. By prioritizing natural sourcing and ethical production, companies can differentiate themselves in a crowded market and command premium pricing. This alignment with values-driven consumption ensures sustained growth and loyalty.

MARKET CHALLENGES Supply Chain Volatility and Raw Material Sourcing

Supply chain volatility and challenges in raw material sourcing are major challenges to the United States vitamin market. This affects production consistency and pricing stability. The majority of vitamin raw materials, particularly active pharmaceutical ingredients, are sourced from a limited number of countries, creating dependency and vulnerability to geopolitical disruptions. According to the US Department of Commerce, trade tensions and logistical bottlenecks have led to fluctuations in the availability and cost of key nutrients such as vitamin C and B complex. As per the Bureau of Labor Statistics, inflationary pressures on transportation and labor have increased manufacturing costs, forcing companies to raise prices or absorb margins. Climate change impacts on agricultural yields affect the supply of plant-based ingredients, adding another layer of uncertainty. Quality control issues in overseas facilities can lead to recalls and reputational damage, requiring rigorous auditing and testing protocols. The lack of domestic production capacity for certain vitamins limits flexibility in responding to supply shocks. Companies must invest in diversified sourcing strategies and inventory buffers, which tie up capital and increase operational complexity. The unpredictability of raw material markets makes long-term planning difficult for manufacturers and retailers. Addressing these supply chain vulnerabilities requires strategic partnerships and investment in local processing capabilities. Resilience must be built into the supply network. Until then, the market will remain exposed to external risks.

Counterfeit Products and Brand Integrity Issues

Counterfeit products and brand integrity issues impede the expansion of the United States vitamin market. This undermines consumer trust and poses health risks. The popularity of high-demand supplements has made them targets for counterfeiters who produce substandard or contaminated products sold through unauthorized online channels. According to the FDA’s 2025 Health Fraud Product Database, counterfeit and illicit supplements are a major public health threat, with laboratory tests regularly identifying undeclared pharmaceutical ingredients and heavy metal contamination. As per the FDA, warnings about fraudulent supplements claiming to treat serious conditions are frequent, highlighting the difficulty in regulating the vast online marketplace. Consumers who inadvertently purchase fake products may experience adverse health effects, leading to negative perceptions of the entire category. Legitimate brands struggle to protect their intellectual property and monitor unauthorized sellers, incurring high legal and investigative costs. The anonymity of e-commerce platforms facilitates the sale of counterfeit goods, making enforcement challenging. Third-party verification programs help distinguish authentic products, but consumer awareness remains low. The presence of counterfeits distorts market data and erodes brand equity, making it difficult for reputable companies to compete on quality alone. Ensuring product authenticity requires advanced tracking technologies and consumer education initiatives. This persistent threat demands ongoing vigilance and collaboration across the industry to safeguard public health and brand reputation.

REPORT COVERAGE

REPORT METRIC

DETAILS

Market Size Available

2025 to 2034

Base Year

2025

Forecast Period

2026 to 2034

Segments Covered

By Application, End User, Distribution Channel, and Region.

Various Analyses Covered

Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities

Countries Covered

California, Washington, Oregon, New York, United States

Market Leaders Profiled

Abbott Laboratories, Amway Corporation, Herbalife Nutrition Ltd., Pfizer Inc., Bayer AG, Pharmavite LLC (Nature Made), The Nature’s Bounty Co., Nestlé Health Science, GlaxoSmithKline plc (Haleon – Centrum), NOW Foods, Glanbia plc, GNC Holdings LLC

SEGMENTAL ANALYSIS By Application Insights

The food and beverages segment held the majority share of 48.9% of the US vitamin market in 2025 because of the widespread practice of fortifying staple foods with essential micronutrients to prevent public health deficiencies. Government mandates and industry standards have established fortification as a critical public health strategy, ensuring that populations receive adequate levels of vitamins such as D, B12, and folic acid. According to the Centers for Disease Control and Prevention, the fortification of grain products with folic acid has significantly reduced the incidence of neural tube defects, demonstrating the effectiveness of this approach. As per the Food and Drug Administration, regulations require or encourage the addition of specific vitamins to milk, cereals, and juices, creating a consistent and high-volume demand for vitamin ingredients. This regulatory framework ensures that nearly every American consumes fortified foods daily, driving steady demand for bulk vitamin supplies. The integration of vitamins into everyday items removes the need for conscious supplementation, making it the most accessible form of nutrient intake. Manufacturers rely on stable and cost-effective vitamin sources to maintain product consistency and nutritional labels. The sheer scale of food production in the United States means that even small amounts of vitamins per unit result in massive aggregate consumption. This foundational role in the food supply chain solidifies the segment’s dominance. The economic efficiency of fortification compared to individual supplementation further supports its widespread adoption across the food industry. Consumer demand for functional and enhanced foods significantly drives the domination of the food and beverages segment by expanding the application of vitamins beyond basic nutrition to health optimization. Shoppers are increasingly seeking products that offer additional health benefits, such as immune support, energy boosting, and stress relief, leading to the incorporation of vitamins into snacks, beverages, and convenience foods. According to research, sales of functional foods and beverages have grown substantially, with vitamins like C, D, and B complex being key ingredients in these products. As per a study, the trend toward preventive health has motivated manufacturers to innovate with vitamin-enriched waters, bars, and gummies that appeal to health-conscious consumers. The convenience of obtaining nutrients through enjoyable food formats rather than pills attracts younger demographics and busy professionals. Marketing campaigns emphasize the holistic benefits of these products, positioning them as lifestyle enhancements rather than mere sustenance. Retailers dedicate prominent shelf space to functional items, recognizing their higher margin potential and consumer appeal. The versatility of vitamins allows for creative formulation in diverse product categories, from breakfast cereals to sports drinks. This continuous innovation and consumer interest ensure that the food and beverages segment remains the largest application area. The alignment with wellness trends guarantees sustained growth and market leadership.

The pharmaceuticals and cosmetics segment is predicted to witness the highest CAGR of 8.2% between 2026 and 2034. This rapid expansion of the segment is fuelled by the rise of nutraceuticals and the integration of vitamins into clinical and therapeutic formulations. Vitamins are increasingly used in prescription and over-the-counter medications to treat specific deficiencies and support medical treatments, such as using high-dose vitamin D for bone health or B vitamins for neurological conditions. According to the National Institutes of Health, research into the therapeutic potential of vitamins has expanded, leading to new indications and higher dosage formulations. As per sources, the nutraceutical sector is experiencing robust growth, with vitamins playing a central role in disease management and prevention strategies. The aging population requires more targeted medical interventions, increasing the demand for pharmaceutical-grade vitamins. Regulatory approvals for new vitamin-based therapies further validate their efficacy and encourage medical professionals’ recommendations. The precision of pharmaceutical formulations ensures higher bioavailability and effectiveness, appealing to patients with specific health needs. This clinical validation drives trust and adoption among healthcare providers and consumers. The expansion of telemedicine and personalized medicine also facilitates the prescription of tailored vitamin regimens. This shift toward the medicalization of vitamins ensures that the pharmaceuticals segment experiences rapid growth. The expansion of vitamin-infused skincare and beauty products accelerates the growth of the cosmetics segment within the pharmaceuticals and cosmetics application area. Consumers are increasingly aware of the benefits of topical vitamins such as C, E, and B3 (niacinamide) for skin health, anti-aging, and protection against environmental damage. According to the American Academy of Dermatology, the use of antioxidant vitamins in skincare routines has become standard practice for maintaining skin integrity and appearance. As per a study, the beauty and personal care industry has seen a surge in products featuring high concentrations of stabilized vitamins, driven by consumer demand for evidence-based ingredients. Social media and influencer marketing have popularized vitamin serums and creams, educating consumers on their benefits and driving trial. The perception of vitamins as safe and effective alternatives to harsh chemical treatments appeals to natural beauty enthusiasts. Manufacturers invest in advanced delivery systems to enhance the penetration and stability of vitamins in topical formulations. The premium pricing of vitamin-rich skincare products contributes to higher revenue growth compared to traditional cosmetics. This convergence of health and beauty trends ensures that the cosmetics segment continues to expand rapidly. The ongoing innovation in topical vitamin applications sustains this high growth trajectory.

By End-User Insights

The adult segment dominated the US vitamin market and captured a 47.3% share in 2025. This leading position of the segment is attributed to the high prevalence of chronic health conditions and the growing aging population that requires ongoing nutritional support. Nutrient absorption decreases with age, while the risk of conditions like osteoporosis, cardiovascular disease, and diabetes increases. Consequently, supplemental intervention often becomes necessary. According to the Census Bureau, the number of adults aged 65 and older is projected to reach 95 million by 2060, creating a large and expanding base of vitamin consumers. As per the National Council on Aging, a significant majority of older adults take multiple medications and supplements to manage their health, driving consistent demand for multivitamins and specific nutrients like calcium and vitamin D. The awareness of preventive health measures among middle-aged adults also contributes to high usage rates, as they seek to maintain vitality and prevent future health issues. Healthcare providers frequently recommend supplements to adult patients to address dietary gaps and support medical treatments. The financial capacity of adults to purchase premium health products further supports market dominance. The habitual nature of supplement use among adults ensures long-term customer retention and steady sales volume. This demographic reality solidifies adults as the primary consumer group in the vitamin market. The pressures of modern workforce lifestyles and associated nutritional gaps significantly drive vitamin consumption among adults. Busy schedules, poor dietary habits, and high stress levels lead many working adults to rely on supplements to maintain energy levels and mental focus. According to the American Psychological Association, stress is a major health concern for Americans, leading to increased interest in adaptogens and B vitamins that support nervous system health. Corporate wellness programs often encourage supplement use to improve employee health and productivity, further normalizing the behavior. The availability of targeted supplements for energy, sleep, and stress management appeals to professionals seeking performance enhancement. Marketing efforts highlight the convenience and efficacy of these products for busy lifestyles. The disposable income of working adults allows for the regular purchase of premium vitamin brands. This lifestyle-driven demand ensures that the adult segment remains the largest and most stable consumer base. The integration of vitamins into daily routines for health maintenance and performance optimization sustains their market leadership.

The children and teenagers segment is estimated to register the fastest CAGR of 7.8% during the forecast period, owing to heightened parental focus on immunity and developmental health. Parents are increasingly proactive in ensuring their children receive adequate nutrients to support growth, cognitive development, and immune function, particularly in the post-pandemic era. The rise of picky eating habits among children further motivates parents to use supplements as a safety net for nutritional intake. Marketing campaigns targeting parents emphasize the safety and efficacy of pediatric vitamins, building trust and encouraging adoption. The availability of appealing formats such as gummies and chewables makes supplementation easier for children. School health initiatives and pediatrician recommendations also play a crucial role in driving usage. This protective instinct and health consciousness among parents ensure rapid growth in this segment. The focus on long-term health outcomes for children sustains this upward trend. Apart from these, the influence of digital media and peer trends accelerates vitamin adoption among teenagers, contributing to the rapid growth of this segment. Social media platforms and influencers promote health and wellness lifestyles, making vitamin consumption a trendy and socially accepted behavior among young people. The availability of stylish and flavored vitamin products designed specifically for teens enhances their appeal and reduces stigma. Peer influence and the desire to fit in with health-conscious groups drive trial and regular use. Brands leverage digital marketing to engage directly with this demographic, creating communities around wellness. The empowerment of teens to make their own health choices further fuels market growth. This cultural shift toward proactive health management among youth ensures that the children and teenagers segment continues to expand at the fastest rate.

By Distribution Channel Insights

The pharmacies and drug stores segment was the largest segment in the US vitamin market and occupied a share of 41.5% in 2025. This supremacy of the segment is credited to the high level of consumer trust and the availability of professional recommendations. Consumers often associate pharmacies with health and medical expertise, making them the preferred destination for purchasing vitamins, especially for specific health concerns. The convenience of filling prescriptions and purchasing supplements in one location enhances customer loyalty. Pharmacy chains invest in trained staff and educational materials to assist customers in selecting appropriate products. The perception of higher quality and safety standards in pharmacies compared to other retail outlets reinforces consumer preference. Insurance and health savings account compatibility also facilitates purchases in this channel. This combination of trust, convenience, and professional support solidifies pharmacies as the dominant distribution channel. The established reputation for health reliability ensures continued market leadership. Furthermore, the extensive network and accessibility of pharmacies and drug stores significantly contribute to their market dominance by ensuring widespread availability of vitamin products. Major pharmacy chains have thousands of locations across the country, making it easy for consumers to access vitamins in their local communities. The integration of pharmacy services with grocery and convenience items further enhances foot traffic and impulse purchases. Loyalty programs and promotional offers in pharmacies encourage repeat business and brand switching. The ability to purchase vitamins alongside other health and personal care items simplifies shopping trips for busy consumers. The reliable supply chain of major pharmacy retailers ensures product availability and freshness. This widespread presence and operational efficiency make pharmacies the most accessible and convenient channel for vitamin purchases. The ease of access and comprehensive product selection sustain their leading position in the market.

The online channels segment is anticipated to witness the fastest CAGR of 10.7% from 2026 to 2034 due to the convenience of home delivery and the rise of direct-to-consumer (DTC) models. Consumers appreciate the ability to browse a wide variety of products, read reviews, and compare prices from the comfort of their homes. DTC brands offer subscription services that ensure regular delivery of vitamins, enhancing customer retention and convenience. The ability to access niche and specialized products that may not be available in local stores expands consumer choice. Digital platforms provide detailed product information and educational content, empowering consumers to make informed decisions. The ease of reordering and managing subscriptions through mobile apps enhances the user experience. This convenience and accessibility ensure that online channels continue to expand rapidly. The seamless integration of technology and retail sustains this high growth trajectory. Personalization and data-driven recommendations accelerate the growth of online vitamin channels by offering tailored solutions that meet individual health needs. E-commerce platforms use algorithms and customer data to recommend specific vitamins based on health goals, dietary preferences, and past purchases. The ability to track orders and manage subscriptions digitally enhances convenience and control for users. Social media integration and influencer partnerships drive traffic to online stores, influencing purchasing decisions. The transparency of online reviews and ratings builds trust and encourages trial of new products. The flexibility of online channels allows for rapid innovation and introduction of new formats and flavors. This focus on customization and user engagement ensures that online channels remain the fastest-growing distribution segment. The continuous improvement in digital tools and personalization capabilities sustains this dynamic growth.

COUNTRY LEVEL ANALYSIS United States

The United States led the North American vitamin market and accounted for a 85.3% share in 2025. It serves as a global leader in innovation and product development. This growth of the US market is driven by high consumer awareness, extensive product availability, and a robust regulatory framework that supports industry growth. According to the Council for Responsible Nutrition (CRN) 2023 Consumer Survey on Dietary Supplements, 74% of U.S. adults use supplements, while the CDC’s National Center for Health Statistics (Data Brief No. 399) reports that 58.5% of adults regularly consume them. As per research from the Nutrition Business Journal (2024) and consumer behavior studies, the widespread adoption of vitamins is driven by a strong culture of preventive health. NHANES data confirms this trend by showing supplement use increases with age and health consciousness. The market benefits from a mature retail infrastructure and advanced e-commerce platforms that ensure widespread access to products. Consumer preferences are influenced by trends toward personalized nutrition, clean labels, and sustainable sourcing, prompting manufacturers to innovate continuously. The presence of major multinational companies fosters competition and drives quality improvements. Regulatory oversight by the FDA ensures safety and labeling accuracy, maintaining consumer trust. The country leads in the development of new formats such as gummies and functional foods, influencing global market trends. Investment in research and clinical trials supports the scientific validation of vitamin benefits. This combination of high demand, innovation, and regulatory stability ensures that the United States remains the central pillar of the global vitamin industry.

COMPETITIVE LANSCAPE

The competition in the United States vitamin market is intense and characterized by the presence of large multinational corporations alongside numerous niche and private label brands. Major players compete based on brand recognition, product quality pricei, price, and distribution efficiency to secure shelf space and consumer loyalty. The market sees frequent innovation as companies strive to differentiate their offerings through unique form, ats, fla,v,o r s and functional benefits. Private label brands pose a significant challenge to national brands, offering lower-priced alternatives that appeal to budget-conscious shoppers. Direct-to-consumer startups contribute to market diversity by catering to specific health needs and personalization trends. Consolidation through mergers and acquisitions is common as larger firms seek to expand their portfolios and achieve economies of scale. Regulatory compliance and quality assurance standards also influence competitive dynamics, requiring continuous investment in safety and efficacy. The rise of digital health and personalized nutrition drives demand for customized solutions,s prompting reformulation and technological adoption. This dynamic landscape requires agility and strategic foresight to navigate changing preferences and maintain market relevance effectively.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the U.S. vitamin market include

Abbott Laboratories Amway Corporation Herbalife Nutrition Ltd. Pfizer Inc. Bayer AG Pharmavite LLC (Nature Made) The Nature’s Bounty Co. Nestlé Health Science GlaxoSmithKline plc (Haleon – Centrum) NOW Foods Glanbia plc GNC Holdings LLC TOP LEADING PLAYERS IN THE MARKET Nestle Health Science is a global leader in health science nutrition with a significant presence in the vitamin and supplement industry. The company offers a diverse portfolio of brands, including Garden of Life and Pure Encapsulations, which cater to various consumer needs. Nestle leverages its extensive research and development capabilities to innovate in personalized nutrition and medical nutrition therapy. Recent actions include strategic acquisitions of specialized supplement brands to expand its product range and reach new customer segments. The company focuses on digital health solutions and direct-to-consumer platforms to enhance customer engagement. These initiatives strengthen its market position by providing comprehensive health solutions and building brand loyalty. Nestle continues to invest in sustainability and ethical sourcing to meet consumer expectations. Nestle integrates science-based nutrition with consumer preferences. By doing so, they maintain their leadership in the global health and wellness market. Bayer AG is a multinational pharmaceutical and life sciences company with a strong footprint in the consumer health sector, including vitamins and supplements. The company owns well-known brands such as One A Day and Phillips, which are staples in households worldwide. Bayer focuses on preventive healthcare and wellness through its wide array of nutritional products. Recent actions involve expanding its digital health offerings and enhancing its e-commerce capabilities to reach consumers directly. The company invests heavily in scientific research to substantiate health claims and ensure product efficacy. Bayer also prioritizes sustainability in its supply chain and packaging to align with environmental goals. These efforts strengthen its market position by building trust and credibility among consumers. Bayer leverages its global distribution network and brand recognition. This allows the company to continue driving growth in the competitive vitamin market. Pfizer Inc., through its consumer healthcare spinoff Haleon, is a major player in the global vitamin and wellness market. Haleon owns iconic brands such as Centrum and Emergen-CC, which are widely recognized for their quality and reliability. The company focuses on empowering people to improve their everyday health with science-led consumer health products. Recent actions include investing in innovation and expanding its portfolio with new formats such as gummies and powders. Haleon leverages data and insights to understand consumer needs and develop targeted solutions. The company also emphasizes digital transformation to enhance customer experience and accessibility. These strategies strengthen its market position by delivering relevant and effective health solutions. Haleon maintains its status as a leading provider of vitamins and supplements globally. They achieve this by combining scientific expertise with consumer-centric innovation. TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the United States vitamin market employ several major strategies to maintain competitiveness and drive growth. Product innovation is central to these efforts, with companies developing new formats such as gummies and personalized supplements to appeal to diverse consumer preferences. Strategic acquisitions allow firms to expand their portfolios and access niche markets with high growth potential. Digital transformation enables direct-to-consumer sales and personalized marketing campaigns that build loyalty and enhance customer engagement. Sustainability initiatives, including eco-friendly packaging and ethical sourcing, enhance brand reputation and meet regulatory expectations. Partnerships with healthcare professionals and retailers ensure prominent placement and credibility in the market. Investment in scientific research substantiates health claims and builds consumer trust. These combined strategies enable participants to adapt to evolving consumer needs and sustain long-term profitability in a highly competitive environment.

MARKET SEGMENTATION

This research report on the U.S. Vitamin Market is segmented and sub-segmented into the following categories.

By Application

Food and Beverages Pharmaceuticals and Cosmetics

By End User

Adults Children and Teenagers

By Distribution Channel

Pharmacies and Drug Stores Online Channels

By Country

California Washington Oregon New York Rest of the United States