Australia Nutritional Supplements Market Overview

Australia Nutritional Supplements Market Overview

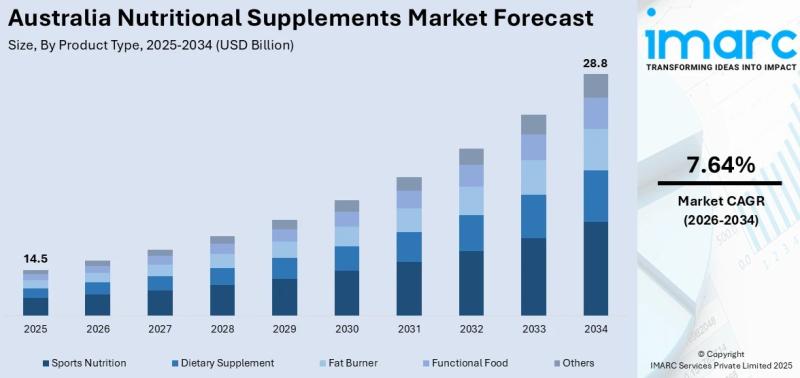

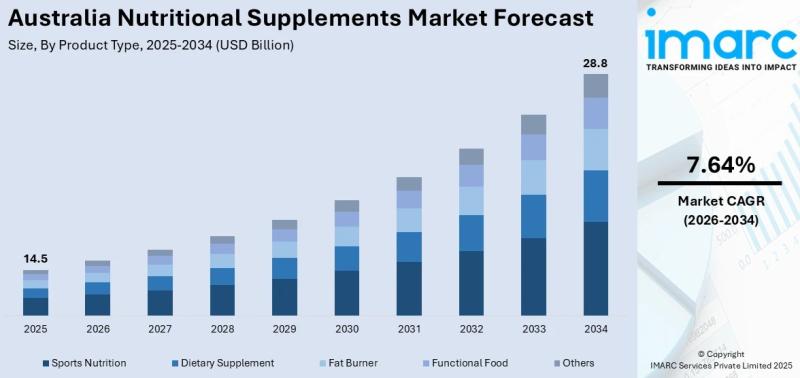

According to IMARC Group’s latest research report, the Australia nutritional supplements market reached a value of USD 14.5 Billion in 2025. Looking forward, the market is expected to reach USD 28.8 Billion by 2034, growing at a CAGR of 7.64% during 2026-2034. The market is driven by approximately two-thirds of Australian adults consuming regularly, a personalized nutrition segment valued at USD 359.5 million and projected to more than double by 2030, rising demand for plant-based supplements with 48% of Australians actively seeking plant-based alternatives, strengthened TGA regulatory frameworks enhancing consumer confidence, and e-commerce supplement sales reaching AUD 1.2 billion with sustained double-digit growth.

Get a sample copy of this report: https://www.imarcgroup.com/australia-nutritional-supplements-market/requestsample

Australia Nutritional Supplements Market Summary

• Australia’s nutritional supplements market benefits from one of the highest supplement consumption rates globally, with approximately two-thirds of adults incorporating into their daily routines and 50% of Australians aged 18 to 64 consuming them regularly. This widespread adoption reflects a cultural shift toward preventive healthcare, with 63% of Australian adults actively seeking to improve their wellbeing through dietary changes. The post-pandemic focus on immunity, mental wellness, and general vitality has cemented supplement use as a mainstream health practice rather than a niche behavior.

• The segment commands the largest share of the product mix, with vitamin supplements accounting for approximately 29.4% of the broader category. Vitamins C, D, and multivitamins remain the highest-demand products, driven by consumer awareness of immune support, bone health, and nutritional gap-filling. The proteins and amino acids segment is emerging as the fastest-growing category, projected to expand at a 13.9% compound annual growth rate, fueled by Australia’s strong fitness culture, the rise of functional nutrition, and growing consumer interest in muscle recovery and sports performance products.

• Sports nutrition represents a dynamic and rapidly expanding product category, with Australia’s protein supplements market reaching approximately AUD 540 million. The Therapeutic Goods Administration’s (TGA) regulatory reform effective since November 2023 now requires sports supplements in pill, capsule, or tablet forms to be registered as therapeutic goods, raising quality and safety standards across the industry. Nutrition Warehouse, Australia’s leading health and personal care retailer, operates over 120 stores nationwide alongside a thriving e-commerce platform, serving as a key distribution channel for sports nutrition products.

• The e-commerce distribution channel is experiencing exceptional growth, with online supplement sales in Australia reaching AUD 1.2 billion and recording a 15% year-on-year increase. Online protein supplement sales specifically grew 14% year-on-year, driven by subscription-based fitness programs and rising demand for ready-to-drink protein beverages among urban consumers. The geographic spread of Australia’s population makes digital channels especially important for reaching regional and remote customers, while direct-to-consumer models enable brands to offer personalized recommendations, subscription services, and tailored product bundles.

• Personalized nutrition has emerged as a high-growth frontier in the Australian supplements market, with the personalized nutrition and supplements segment valued at USD 359.5 million and projected to grow to USD 853.5 million by 2030. Genetic testing, digital health platforms, and AI-driven recommendation engines are enabling brands to deliver customized supplement protocols tailored to individual health profiles, lifestyle factors, and wellness goals. Blackmores’ AU$85 million investment in its AI-powered VitalMatch personalized nutrition platform in February 2025 signals the scale of industry commitment to this segment.

• Plant-based and clean-label supplements are gaining significant consumer traction, with 48% of Australians actively seeking plant-based alternatives and projected plant-based supplement sales reaching AUD 600 million. This demand is driven by growing environmental awareness, ethical sourcing preferences, and recognition of the health benefits from botanical and organic compounds. Herbal extracts, natural-source vitamins, superfoods, and adaptogenic ingredients are becoming increasingly popular across diverse consumer groups, pushing manufacturers to reformulate existing products and develop new lines that meet clean-label expectations.

• The geriatric consumer group represents a substantial and expanding demand segment, as Australia’s aging population drives increasing need for supplements targeting bone density, joint health, cardiovascular performance, cognitive function, and immune support. Older Australians are embracing supplements as a complementary approach to managing age-related conditions including arthritis, diabetes, and cardiovascular disease. Healthcare professionals are increasingly recommending targeted supplementation to address nutritional deficiencies and enhance quality of life, providing clinical validation that reinforces consumer confidence in the geriatric supplement category.

• The ACT and New South Wales region leads national demand, reflecting the concentration of Australia’s population, retail infrastructure, and health-conscious urban consumers in Sydney and surrounding areas. Victoria and Tasmania follow closely, anchored by Melbourne’s wellness-oriented consumer base, while Queensland benefits from a strong fitness and outdoor lifestyle culture that supports sports nutrition and active health supplement consumption. Western Australia’s mining workforce and remote communities present unique distribution challenges that have accelerated e-commerce adoption and direct-to-consumer supplement delivery models.

Key Trends Shaping the Australia Nutritional Supplements Market

• The TGA’s regulatory tightening is reshaping Australia’s supplement landscape, with new vitamin B6 regulations announced in November 2025 requiring products with doses between 50mg and 200mg to be classified as Schedule 3 pharmacist-only medicines. This followed 250 reports of peripheral neuropathy linked to vitamin B6 products between January 2023 and October 2025. The regulatory evolution is raising compliance standards across the industry, enhancing consumer safety, and favoring established manufacturers with robust quality assurance systems over smaller operators who may struggle to meet the higher registration requirements.

• Mental health and sleep support supplements have become one of the fastest-growing product niches in the Australian market, with brands like Blackmores and Swisse investing heavily in formulations targeting stress relief, cognitive performance, and sleep quality. This trend reflects broader societal awareness of mental wellbeing and the desire for natural, non-pharmaceutical approaches to managing everyday stress and anxiety. Products featuring magnesium, ashwagandha, L-theanine, and melatonin are experiencing particularly strong demand across adult consumer segments.

• Beauty-from-within supplements featuring collagen peptides, hyaluronic acid, biotin, and antioxidant-rich vitamins have gained mainstream acceptance, particularly among female consumers and the aging population. This convergence of beauty and wellness is creating a new product category that bridges traditional supplement and skincare markets, with ingestible beauty products appearing across pharmacy, health food, and even mainstream grocery retail channels. Australian consumers are increasingly viewing nutritional supplementation as an integrated approach to both internal health and external appearance.

• Functional foods and beverages are blurring the line between traditional supplements and everyday nutrition, with products like Beforeyouspeak Coffee’s health-focused blends expanding into major retailers including Woolworths, Ampol, and Caltex convenience stores. This trend reflects consumer preference for incorporating nutritional benefits into familiar food and drink formats rather than taking additional pills or capsules. The functional food segment benefits from higher consumption frequency and stronger brand loyalty compared to traditional supplement formats.

• Subscription-based and direct-to-consumer models are transforming how Australians purchase supplements, enabling brands to build recurring revenue streams while delivering personalized product recommendations and convenient auto-replenishment. These digital-first business models reduce dependence on traditional brick-and-mortar retail, allow for richer customer data collection, and support the personalized nutrition trend by adjusting supplement protocols based on ongoing health feedback and changing lifestyle needs.

Explore the full report with TOC & list of figures: https://www.imarcgroup.com/australia-nutritional-supplements-market

Market Growth Factors

Preventive Healthcare Culture and Post-Pandemic Wellness Focus

Australia’s shift toward preventive healthcare represents the most fundamental growth driver for the nutritional supplements market. Approximately two-thirds of Australian adults now consume daily, and 63% are actively seeking to improve their wellbeing through dietary changes. The COVID-19 pandemic served as a catalyst for this behavioral shift, with sustained post-pandemic demand for immunity-boosting supplements including vitamin C, vitamin D, zinc, and elderberry. This preventive mindset extends beyond immunity to encompass mental wellness, energy management, gut health, and stress support, creating multiple demand verticals within the supplement category. Health-oriented media content, social media influencers, and greater access to health information through digital platforms have educated consumers about the role of nutritional supplementation in long-term wellbeing. Corporate wellness programs are further amplifying demand by incorporating supplement allowances and health screenings into employee benefit packages. The alignment of consumer behavior, employer incentives, and healthcare practitioner recommendations creates a reinforcing growth cycle that supports sustained market expansion.

Aging Population and Chronic Disease Management

Australia’s aging demographic profile is creating a structural growth driver for nutritional supplements, with older Australians increasingly seeking products that support bone density, joint health, cardiovascular performance, cognitive function, and immune resilience. The rising incidence of chronic conditions including diabetes, cardiovascular disease, and arthritis has positioned supplements as a complementary therapy alongside conventional medical treatment. Healthcare providers are increasingly advocating nutritional supplementation to manage deficiencies and improve quality of life, providing clinical endorsement that strengthens consumer confidence. The geriatric consumer group’s willingness to invest in premium, condition-specific formulations supports higher average selling prices and creates opportunities for specialized product lines. Simultaneously, the pregnant consumer segment drives demand for prenatal vitamins, folate, iron, and omega-3 supplements, supported by government health guidelines and medical practitioner recommendations. These demographically driven demand segments provide predictable, long-term growth foundations that are largely insulated from discretionary spending fluctuations.

E-Commerce Expansion and Digital Innovation in Supplement Retail

The rapid growth of e-commerce and direct-to-consumer channels represents a transformative force in Australia’s nutritional supplements market. Online supplement sales have reached AUD 1.2 billion, recording a 15% year-on-year increase, while online protein supplement sales grew 14% year-on-year driven by subscription fitness programs and urban demand for ready-to-drink formats. Australia’s geographically dispersed population of 26 million across a vast continent creates a compelling case for digital distribution, enabling brands to serve remote and regional customers cost-effectively through direct shipping logistics. Blackmores’ AU$85 million investment in the AI-powered VitalMatch personalized nutrition platform demonstrates how technology is converging with e-commerce to create differentiated consumer experiences. Subscription models, influencer marketing, and content-driven health education campaigns are enabling supplement brands to build deeper customer relationships and higher lifetime values than traditional retail allows. The personalized nutrition segment, valued at USD 359.5 million and projected to reach USD 853.5 million by 2030, is almost entirely enabled by digital platforms that collect health data and deliver customized recommendations at scale.

Australia Nutritional Supplements Market Segmentation

IMARC Group provides an analysis of the key trends in each segment of the Australia nutritional supplements market, along with forecasts at the country and regional levels from 2026-2034. The market has been categorized based on product type, form, distribution channel, consumer group, and region.

By Product Type:

• Sports Nutrition

• Fat Burner

• Functional Food

• Others

By Form:

• Powder

• Tablets

• Capsules

• Liquid

• Soft Gels

• Others

By Distribution Channel:

• Brick and Mortar

• E-Commerce

By Consumer Group:

• Infants

• Children

• Adults

• Pregnant

• Geriatric

By Region:

• Australia Capital Territory & New South Wales

• Victoria & Tasmania

• Queensland

• Northern Territory & Southern Australia

• Western Australia

Key Players in the Australia Nutritional Supplements Market

The competitive landscape of the Australia nutritional supplements market features a combination of established domestic brands, international pharmaceutical companies, and emerging direct-to-consumer startups. Blackmores (acquired by Japan’s Kirin Holdings in 2023 for AUD 1.9 billion) and Swisse Wellness (owned by Hong Kong-listed H&H Group since 2015) remain the dominant market leaders with extensive product portfolios spanning vitamins, minerals, herbal supplements, and sports nutrition. Other prominent players include PharmaCare’s Nature’s Way and Bioglan brands, Nutrition Warehouse (operating over 120 stores nationally), and BioCeuticals (also part of the Kirin portfolio). Emerging brands such as Vitadrop and Beforeyouspeak Coffee are disrupting traditional categories with innovative formats and health-focused positioning. Competition is shaped by brand trust, TGA compliance capabilities, distribution reach across pharmacy and e-commerce channels, product innovation in personalized and plant-based segments, and the ability to build direct consumer relationships through digital platforms.

Key Aspects Required for the Australia Nutritional Supplements Market Report

• Market Performance: An in-depth analysis of the Australia nutritional supplements market covering historical trends and current dynamics, with a focus on the USD 14.5 Billion valuation and projected growth trajectory reaching USD 28.8 Billion by 2034.

• Market Segmentation: Comprehensive breakdown across product types (sports nutrition, fat burner, functional food), forms (powder, tablets, capsules, liquid, soft gels), distribution channels, consumer groups, and regions.

• Regional Analysis: Detailed evaluation of supplement demand across ACT & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, and Western Australia, covering urban vs. regional consumption patterns and distribution dynamics.

• Competitive Landscape: Profiling of major players including Blackmores, Swisse Wellness, Nature’s Way, BioCeuticals, Nutrition Warehouse, and emerging DTC brands, covering product portfolios, acquisition activity, and market positioning strategies.

• Industry Trends and Drivers: Assessment of preventive healthcare adoption, aging population dynamics, personalized nutrition growth, plant-based supplement demand, e-commerce expansion, and TGA regulatory evolution shaping market direction.

• Regulatory Analysis: Examination of TGA reforms including sports supplement registration requirements, vitamin B6 scheduling changes, and evolving compliance frameworks that influence product development, marketing claims, and market access.

• Consumer Behavior Analysis: Evaluation of supplement consumption patterns across demographic groups, spending trends, channel preferences, brand loyalty factors, and the influence of digital health platforms and social media on purchasing decisions.

• Future Outlook: Forward-looking projections covering the implications of AI-driven personalized nutrition, functional food convergence, subscription commerce growth, and international expansion opportunities on long-term market development.

Recent News and Developments

• February 2025: Blackmores Group announced an AU$85 million investment in VitalMatch, an AI-powered personalized nutrition platform utilizing genetic testing and health data analytics to deliver customized supplement recommendations for Australian consumers.

• November 2025: The TGA announced new vitamin B6 regulations requiring products with doses between 50mg and 200mg to be classified as Schedule 3 pharmacist-only medicines, with labels to be updated by June 2027, following 250 reports of peripheral neuropathy.

• 2025: Online nutritional supplement sales in Australia continued double-digit growth, with e-commerce channel revenue reaching AUD 1.2 billion and online protein supplement sales recording a 14% year-on-year increase driven by subscription models.

• 2025: The personalized nutrition and supplements market in Australia was valued at USD 359.5 million, with genetic testing and AI-driven recommendation platforms enabling customized supplement protocols for individual health profiles.

• May 2025: Polaris Lawyers announced investigation of a proposed class action against Blackmores over vitamin B6 content in supplements, receiving approximately 900 responses by July 2025, highlighting the importance of dosage safety and regulatory compliance.

• 2025: Plant-based supplement demand surged with 48% of Australians actively seeking plant-based alternatives, driving projected plant-based supplement sales toward AUD 600 million as clean-label and botanical products gained mainstream acceptance.

• 2024: Vitadrop, founded by Charlie Wood and Dan Concannon, released 11 water-based vitamin supplements including four TGA-accredited products in major Australian retailers, projecting AUD 2 million revenue in 2024 with a target of AUD 50 million by 2030.

• 2024: Beforeyouspeak Coffee expanded into the Middle East, launching health-focused coffee blends in 25 UAE supermarkets with plans to enter Saudi Arabia, while increasing its Australian presence in Woolworths and convenience store chains.

Ask an analyst for your customized sample: https://www.imarcgroup.com/request?type=report&id=36682&flag=C

Contact Us

IMARC Group

134 N 4th St. Brooklyn, NY 11249, USA

Email: sales@imarcgroup.com

Tel No: (D) +91 120 611 7970

United States: +1-631-791-1145

About Us

IMARC Group is a global management consulting firm that helps the world’s most ambitious changemakers to create a great impact. The company provides a comprehensive suite of market entry and expansion services. IMARC’s offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, and networking facilitation, among others.

The company has done projects in over 135 countries and has helped more than 2,500 clients across the globe. IMARC currently works from 11 offices across the world, including its headquarters in Noida, India. It has a team of over 600 people, including former industry executives, subject matter experts, and management professionals. IMARC is among the top 10 management consulting firms based in India.

This release was published on openPR.