Colgate-Palmolive (CL) stock has recently attracted attention as reports highlight expectations for first quarter 2026 revenue and earnings per share, supported by consumer demand and science based progress in Hill’s Pet Nutrition.

See our latest analysis for Colgate-Palmolive.

The recent earnings focus and upcoming shareholder votes sit alongside a share price of $85.67, with a 7 day share price return of 4.72% and year to date share price return of 10.27%. The 1 year total shareholder return of a 4.87% decline contrasts with 3 and 5 year total shareholder returns of 13.75% and 18.98%, suggesting that near term momentum has firmed even as longer term holders have seen more modest gains.

If you are weighing Colgate-Palmolive’s recent momentum against other opportunities, it can help to scan a curated set of ideas and uncover 18 top founder-led companies

So with expectations for higher sales and earnings, a share price sitting below the published price target and an indicated intrinsic discount, should you view Colgate-Palmolive as undervalued, or is the market already pricing in that future growth?

Most Popular Narrative: 11.4% Undervalued

Compared with the last close of $85.67, the most followed narrative points to a fair value of $96.68, framing Colgate-Palmolive as trading at a discount based on long term earnings and cash flow assumptions.

Emerging markets such as India, Latin America, and Southeast Asia, where rising incomes and urbanization are growing the addressable customer base, remain a focus with stepped-up innovation, brand investment, and price tiering, sustaining long-term volume and revenue growth. Productivity and restructuring initiatives ($200 to $300 million over three years) are designed to free up resources for innovation, digital, and R&D investments, enabling incremental margin expansion and additional reinvestment for growth.

Want to see what kind of revenue path and margin profile sit behind that fair value, and how future earnings and multiples are expected to line up by 2029?

Result: Fair Value of $96.68 (UNDERVALUED)

Have a read of the narrative in full and understand what’s behind the forecasts.

However, that narrative could be knocked off course if higher oil based input costs keep pressuring margins, or if private label competition further weighs on Hill’s in key markets.

Find out about the key risks to this Colgate-Palmolive narrative.

Another Way to Look at Valuation

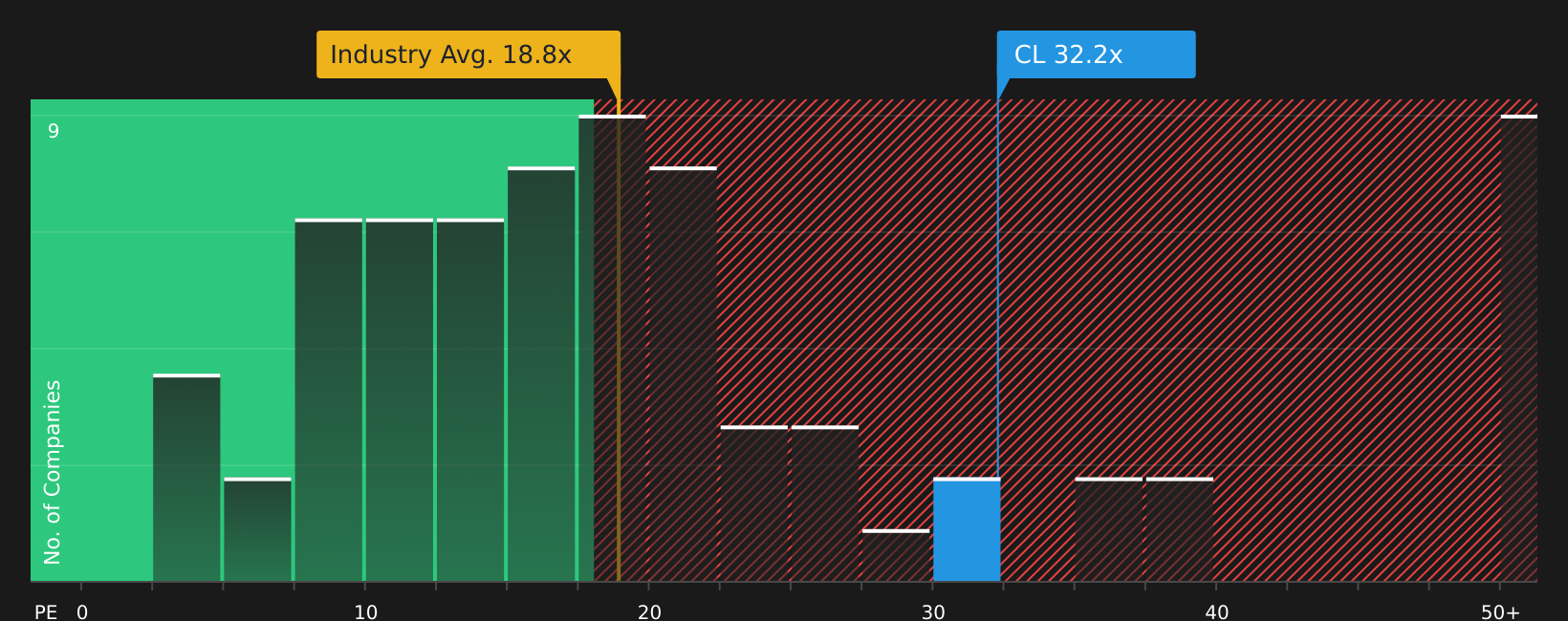

The earlier fair value of $96.68 leans on long term earnings and cash flow assumptions. Colgate-Palmolive currently trades on a P/E of 32.2x versus an estimated fair ratio of 23.5x, the global Household Products average of 18.8x and a peer average of 21.7x. That richer multiple suggests less room for error if growth or margins come in below expectations, so which signal do you put more weight on?

See what the numbers say about this price — find out in our valuation breakdown.

NYSE:CL P/E Ratio as at Apr 2026Next Steps

NYSE:CL P/E Ratio as at Apr 2026Next Steps

With mixed signals on valuation and sentiment, would you prefer to rely on the headline view, or quickly test the story yourself by weighing up the 3 key rewards and 3 important warning signs?

Ready to Hunt for Your Next Opportunity?

If Colgate-Palmolive has sharpened your thinking, now is the moment to widen the lens and line up fresh ideas before the market moves first.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com