Planet Fitness, Inc. earlier announced it would release its Q1 2026 results and host an earnings call before the U.S. market opened on May 7, 2026.

Institutional commentary from Baron Capital has drawn attention to Planet Fitness’s cautious 2026 guidance, even as key metrics like same-store sales, EBITDA and earnings per share improved under new leadership.

We’ll now examine how Baron Capital’s focus on cautious 2026 guidance, alongside the imminent earnings release, reshapes Planet Fitness’s investment narrative.

Invest in the nuclear renaissance through our list of 91 elite nuclear energy infrastructure plays powering the global AI revolution.

Planet Fitness Investment Narrative Recap

To own Planet Fitness, you need to believe its low cost, asset light franchise model can keep adding members and clubs while preserving profitability. The near term catalyst is how the Q1 2026 earnings and any updates to 2026 guidance reconcile cautious expectations with recent improvements in same store sales and earnings. The biggest current risk remains whether higher churn from easier online cancellations and competitive pressure will weigh on recurring membership revenue; today’s news does not materially change that.

The upcoming Q1 2026 earnings release and call on May 7 matter because they sit directly against Baron Capital’s concern about cautious 2026 guidance. Together, they frame the next checkpoint for key catalysts such as unit growth, member retention and franchisee economics, and will help investors judge whether recent gains in same store sales, EBITDA and EPS under new leadership are enough to offset worries about softer guidance and a weaker share price.

Yet even with encouraging recent metrics, the risk that higher online driven cancellations quietly reshape Planet Fitness’s revenue profile is something investors should be aware of…

Read the full narrative on Planet Fitness (it’s free!)

Planet Fitness’ narrative projects $1.8 billion revenue and $328.5 million earnings by 2029. This requires 12.7% yearly revenue growth and roughly a $109 million earnings increase from $219.1 million today.

Uncover how Planet Fitness’ forecasts yield a $112.06 fair value, a 75% upside to its current price.

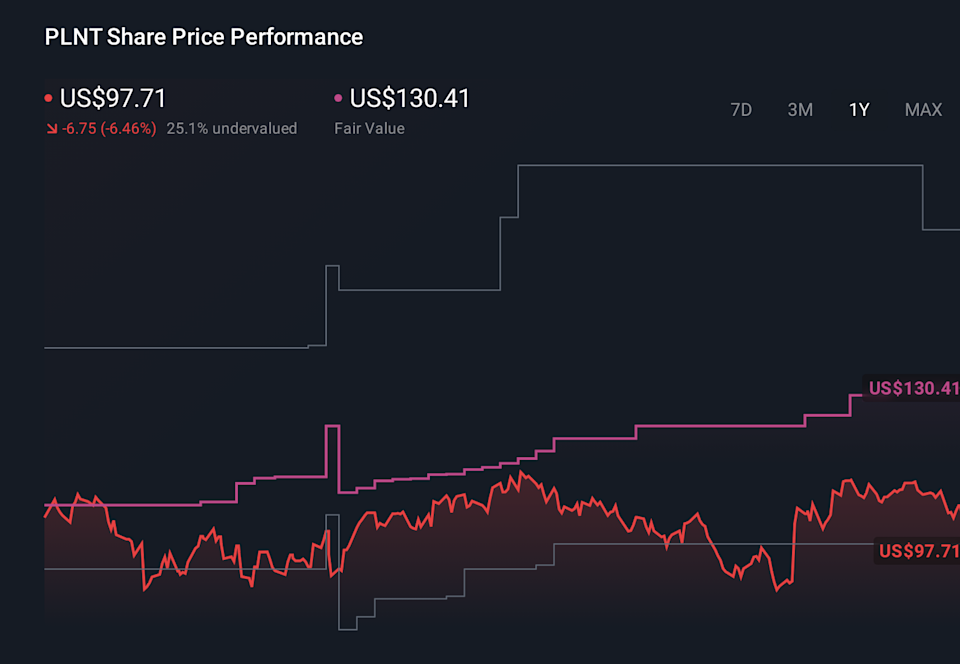

Exploring Other Perspectives  PLNT 1-Year Stock Price Chart

PLNT 1-Year Stock Price Chart

While consensus focuses on steady growth and churn risk, the most optimistic analysts were assuming revenue could reach about US$1.9 billion and earnings US$367.9 million by 2029, which is a far more upbeat path than many expect and could look different once markets digest this latest cautious guidance and earnings update.

Explore 4 other fair value estimates on Planet Fitness – why the stock might be worth as much as 75% more than the current price!

Form Your Own Verdict

Don’t just follow the ticker – dig into the data and build a conviction that’s truly your own.

Interested In Other Possibilities?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include PLNT.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com