Q1 2026 earnings snapshot

Natural Grocers by Vitamin Cottage (NGVC) opened fiscal 2026 with Q1 revenue of US$335.6 million and basic EPS of US$0.49, setting the tone for its latest earnings update. The company reported revenue of US$330.2 million and EPS of US$0.43 in Q1 2025, compared with US$335.6 million and EPS of US$0.49 in Q1 2026. Trailing twelve month EPS stands at US$2.08 on revenue of about US$1.3 billion, with higher net profit margins and earnings growth framing the quarter as one where profitability is a key focus for investors.

See our full analysis for Natural Grocers by Vitamin Cottage.

With the headline numbers on the table, the next step is to see how this profitability story lines up against the widely held narratives around Natural Grocers by Vitamin Cottage, and where the latest results might challenge them.

Curious how numbers become stories that shape markets? Explore Community Narratives

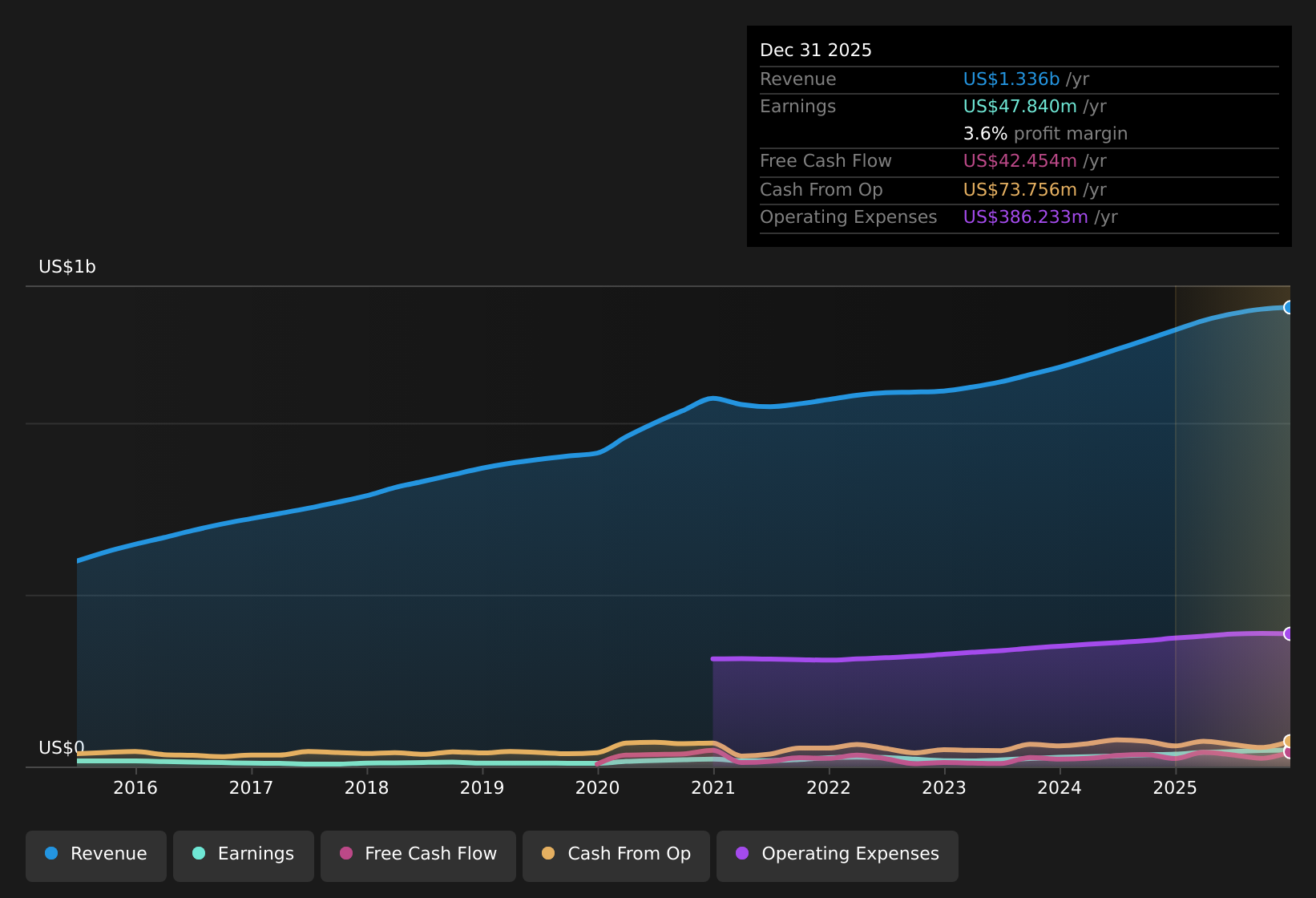

NYSE:NGVC Earnings & Revenue History as at May 2026 Margins and EPS strengthen over 12 months Trailing twelve month net profit margin is 3.6% versus 2.8% a year ago, with Basic EPS at US$2.08 over US$1.34b of revenue for the same period. What stands out for a bullish view is that trailing twelve month earnings grew 32.5% year over year while the five year compound growth rate is 19.4% per year. This supports the idea of a business with earnings that have been growing faster than the long term average, even as recent quarterly same store sales growth of 1.7% in Q1 2026 contrasts with earlier figures of 7.4% and 8.9% in 2025, suggesting bulls need to weigh stronger profitability against a softer top line trend. Same store sales slow from 8.9% to 1.7% Same store sales growth was 1.7% in Q1 2026 compared with 8.9% in Q1 2025 and 7.4% in Q3 2025, while quarterly revenue in the last four reported periods has stayed in a tight range around US$328.7 million to US$336.1 million. Bears argue that slower top line momentum can cap enthusiasm, and the forecast that revenue is expected to grow at 5.1% per year versus an 11.4% per year US market forecast leans toward that cautious view. Yet trailing twelve month EPS at US$2.08 and net income of US$47.84 million still reflect profitability that challenges a purely bearish stance focused only on moderating same store sales and relative revenue growth. Skeptics focusing on the sales slowdown may be missing how the earnings trend and margin profile fit into the broader debate about Natural Grocers by Vitamin Cottage, so it can help to see the structured arguments in the 📊 Read the what the Community is saying about Natural Grocers by Vitamin Cottage.. P/E of 13.4x and DCF fair value of US$47.64 Natural Grocers by Vitamin Cottage trades on a trailing P/E of 13.4x, compared with 17.9x for the US Consumer Retailing industry and 15.6x for peers, and the provided DCF fair value of US$47.64 is above the current share price of US$27.76. What is relevant for investors weighing the bullish angle is that the stock is priced below both sector P/E averages while also sitting about 41.7% below the cited DCF fair value. At the same time, revenue is forecast to grow at 5.1% per year versus an 11.4% per year US market forecast, so the valuation gap that supports a positive view is partly held back by more modest revenue growth expectations compared with the broader market. Next Steps

NYSE:NGVC Earnings & Revenue History as at May 2026 Margins and EPS strengthen over 12 months Trailing twelve month net profit margin is 3.6% versus 2.8% a year ago, with Basic EPS at US$2.08 over US$1.34b of revenue for the same period. What stands out for a bullish view is that trailing twelve month earnings grew 32.5% year over year while the five year compound growth rate is 19.4% per year. This supports the idea of a business with earnings that have been growing faster than the long term average, even as recent quarterly same store sales growth of 1.7% in Q1 2026 contrasts with earlier figures of 7.4% and 8.9% in 2025, suggesting bulls need to weigh stronger profitability against a softer top line trend. Same store sales slow from 8.9% to 1.7% Same store sales growth was 1.7% in Q1 2026 compared with 8.9% in Q1 2025 and 7.4% in Q3 2025, while quarterly revenue in the last four reported periods has stayed in a tight range around US$328.7 million to US$336.1 million. Bears argue that slower top line momentum can cap enthusiasm, and the forecast that revenue is expected to grow at 5.1% per year versus an 11.4% per year US market forecast leans toward that cautious view. Yet trailing twelve month EPS at US$2.08 and net income of US$47.84 million still reflect profitability that challenges a purely bearish stance focused only on moderating same store sales and relative revenue growth. Skeptics focusing on the sales slowdown may be missing how the earnings trend and margin profile fit into the broader debate about Natural Grocers by Vitamin Cottage, so it can help to see the structured arguments in the 📊 Read the what the Community is saying about Natural Grocers by Vitamin Cottage.. P/E of 13.4x and DCF fair value of US$47.64 Natural Grocers by Vitamin Cottage trades on a trailing P/E of 13.4x, compared with 17.9x for the US Consumer Retailing industry and 15.6x for peers, and the provided DCF fair value of US$47.64 is above the current share price of US$27.76. What is relevant for investors weighing the bullish angle is that the stock is priced below both sector P/E averages while also sitting about 41.7% below the cited DCF fair value. At the same time, revenue is forecast to grow at 5.1% per year versus an 11.4% per year US market forecast, so the valuation gap that supports a positive view is partly held back by more modest revenue growth expectations compared with the broader market. Next Steps

Don’t just look at this quarter; the real story is in the long-term trend. We’ve done an in-depth analysis on Natural Grocers by Vitamin Cottage’s growth and its valuation to see if today’s price is a bargain. Add the company to your watchlist or portfolio now so you don’t miss the next big move.

If the mix of earnings strength and slower sales leaves you on the fence, it helps to move quickly and test the data yourself. To see exactly what those optimists are focusing on, start with the 2 key rewards.

Explore Alternatives

Natural Grocers by Vitamin Cottage is growing earnings and margins, but slower same store sales and more modest revenue growth expectations limit the overall growth story.

If that softer top line trend gives you pause, it is worth checking stocks expected to grow faster by starting with the 51 high quality undervalued stocks.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we’re here to simplify it.

Discover if Natural Grocers by Vitamin Cottage might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com