In the first quarter of 2026, Herbalife Ltd. reported net sales of US$1,317.2 million and net income of US$61.9 million, while also refinancing its capital structure with US$800 million of new senior secured notes and updated bank facilities.

The company coupled this earnings beat with guidance for second-quarter and full-year 2026 net sales growth of 1.5% to 5.5% year over year, underscoring its push into personalized nutrition and reinforcing progress on balance sheet reshaping through lower-cost debt.

We will now examine how Herbalife’s stronger first-quarter performance and refreshed debt structure affect the existing investment narrative for the company.

The future of work is here. Discover the 30 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

Herbalife Investment Narrative Recap

To own Herbalife, you need to believe its shift toward personalized nutrition and digital engagement can offset pressures on its multi-level marketing model and supplement demand. The key short term catalyst is whether modest guided net sales growth translates into firmer volumes across more regions, while the biggest current risk remains regulatory and reputational pressure on MLM practices. The latest earnings beat and refinancing help, but do not fundamentally change those near term dynamics.

The most relevant recent development is the US$800.0 million senior secured notes and new bank facilities that refinanced higher cost 12.250% notes and term debt. This matters because Herbalife’s investment case increasingly hinges on its ability to fund technology, personalization, and product initiatives while keeping leverage and interest costs under control, so this balance sheet reshaping directly ties into the near term execution catalyst around its wellness transformation.

Yet behind Herbalife’s improving metrics, the ongoing risk of stricter global scrutiny of MLM models is something investors should be aware of…

Read the full narrative on Herbalife (it’s free!)

Herbalife’s narrative projects $5.6 billion revenue and $320.8 million earnings by 2029. This requires 3.8% yearly revenue growth and a $92.5 million earnings increase from $228.3 million.

Uncover how Herbalife’s forecasts yield a $17.50 fair value, a 28% upside to its current price.

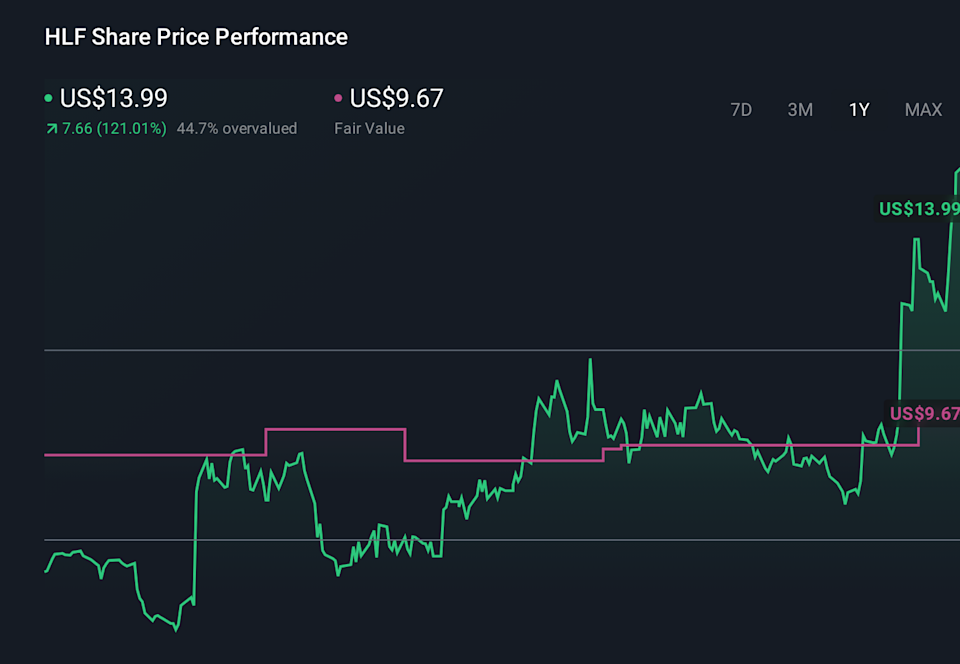

Exploring Other Perspectives  HLF 1-Year Stock Price Chart

HLF 1-Year Stock Price Chart

Some of the most optimistic analysts were assuming Herbalife could lift revenue to about US$5.8 billion and earnings to roughly US$339.0 million by 2029, which is far more upbeat than the consensus narrative. When you compare that to fresh Q1 results and new guidance, it shows how differently you might weigh upside from data driven distributor tools versus regulatory and MLM model risks, and why it can help to explore several viewpoints before deciding what you believe.

Explore 6 other fair value estimates on Herbalife – why the stock might be worth over 5x more than the current price!

Reach Your Own Conclusion

Don’t just follow the ticker – dig into the data and build a conviction that’s truly your own.

Ready For A Different Approach?

Opportunities like this don’t last. These are today’s most promising picks. Check them out now:

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include HLF.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com