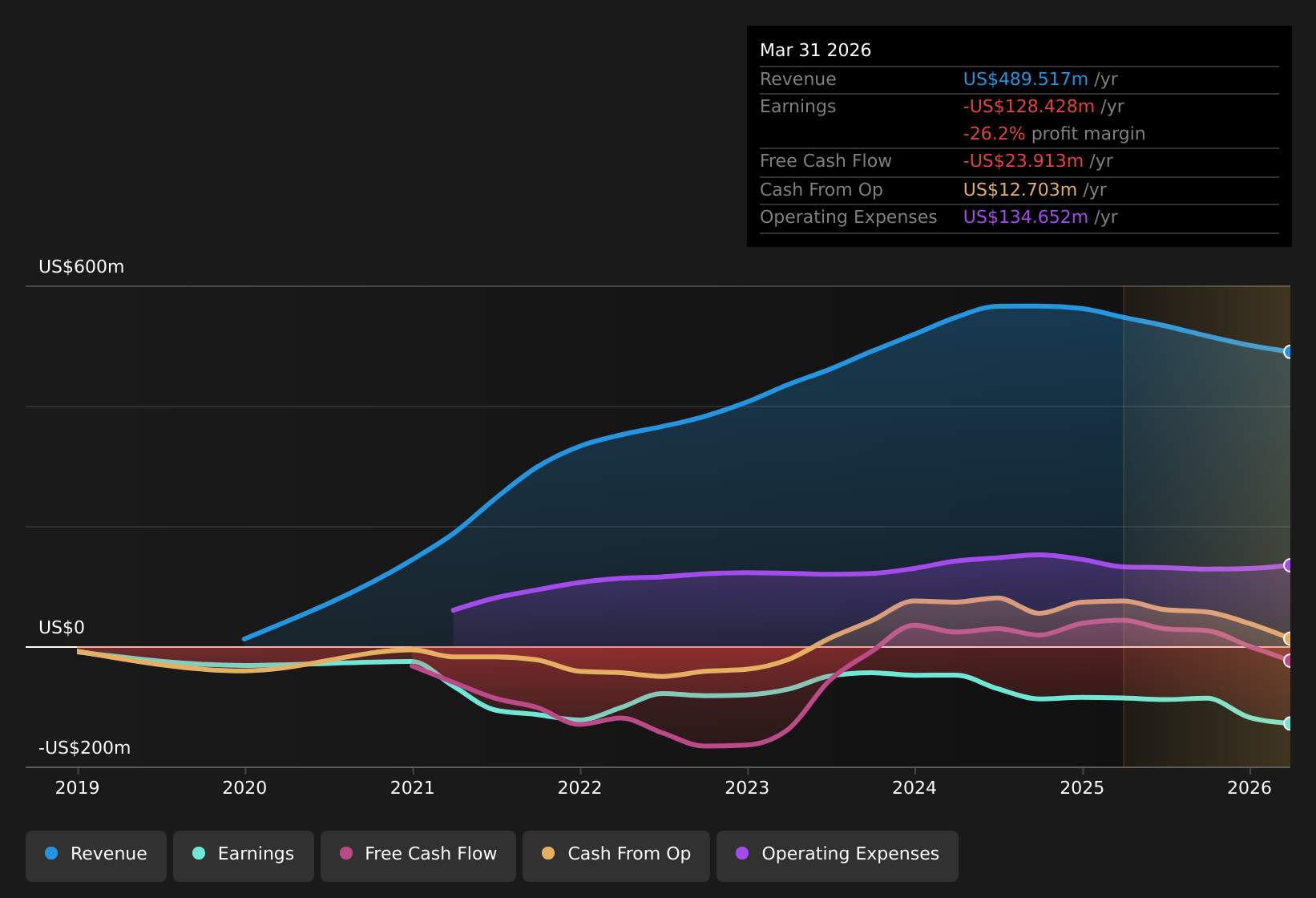

Ascend Wellness Holdings (CNSX:AAWH.U) opened Q1 2026 with revenue of US$116.9 million and a net loss of US$29.5 million, or EPS of US$0.15 loss, while the trailing 12 month figures show revenue of US$489.5 million and a net loss of US$128.4 million, or EPS of US$0.63 loss. Over recent quarters the company has reported revenue ranging from US$127.0 million to US$120.5 million, alongside quarterly EPS losses between US$0.09 and US$0.24. The latest figures therefore keep the focus on how quickly margins can be repaired and whether the current loss profile can support any improvement in profitability.

See our full analysis for Ascend Wellness Holdings.

With the headline numbers on the table, the next step is to set these results against the most common narratives around Ascend Wellness Holdings to see which views align with the data and which are starting to look out of date.

See what the community is saying about Ascend Wellness Holdings

CNSX:AAWH.U Earnings & Revenue History as at May 2026 Losses Widen On Lower TTM Revenue Over the trailing 12 months, revenue came in at US$489.5 million against a net loss of US$128.4 million and basic EPS loss of US$0.63, compared with earlier trailing data showing revenue of US$561.6 million and a net loss of US$85.0 million with an EPS loss of US$0.40. What stands out for the bullish narrative is that expectations of higher earnings power sit against trailing losses that have grown by about 0.9% per year and a current net loss of US$29.5 million in Q1 2026. This means:

CNSX:AAWH.U Earnings & Revenue History as at May 2026 Losses Widen On Lower TTM Revenue Over the trailing 12 months, revenue came in at US$489.5 million against a net loss of US$128.4 million and basic EPS loss of US$0.63, compared with earlier trailing data showing revenue of US$561.6 million and a net loss of US$85.0 million with an EPS loss of US$0.40. What stands out for the bullish narrative is that expectations of higher earnings power sit against trailing losses that have grown by about 0.9% per year and a current net loss of US$29.5 million in Q1 2026. This means:

Bulls point to densification, automation and branded products as future earnings drivers, yet the latest quarter still shows a loss of US$29.5 million on revenue of US$116.9 million and no profit forecast within three years. Analysts in the optimistic camp reference potential earnings of around US$79.6 million to US$81.1 million several years out, while the trailing figures still show cumulative losses of US$128.4 million, so the current data is not yet aligning with that earnings ramp.

Supporters who want to see how bullish arguments stack up against these trailing losses can go deeper into the detailed thesis in the 🐂 Ascend Wellness Holdings Bull Case

Persistent Unprofitability And Negative Equity Across the last six reported quarters, Ascend Wellness Holdings has reported net losses in every period, ranging from US$16.8 million in Q4 2024 to US$48.7 million in Q4 2025, and the analysis also flags negative shareholders’ equity as a major balance sheet risk. Critics arguing the bearish case focus on this string of losses and negative equity, and the trailing figures give that view some clear support, because:

The company is described as unprofitable over the trailing 12 months and not forecast to reach profitability in the next three years, which lines up with quarterly EPS losses between US$0.08 and US$0.24 in the recent history provided. Negative shareholders’ equity on top of US$128.4 million in trailing net losses means any future earnings recovery in the bearish scenario has to overcome both current operating losses and an already weak capital base.

If you are weighing these risks, it is worth reading how more cautious investors frame the downside in the 🐻 Ascend Wellness Holdings Bear Case

Low P/S Multiple Versus DCF Fair Value With the share price at US$0.56, the stock is trading at a P/S of about 0.2x compared with the referenced industry at roughly 1.1x and peers at about 2.4x, and sits well below a cited DCF fair value of roughly US$1.05 as well as an analyst target of US$2.35. Supporters of the bullish view see this valuation gap as a potential opportunity, while the bearish narrative treats it as compensation for risk, and the current numbers highlight that tension:

On one hand, trading about 46.5% below the DCF fair value and at a discount to industry and peer P/S multiples fits a story that the market is heavily discounting the stock relative to its sales base. On the other hand, revenue growth of about 3.9% per year versus a 5.2% market comparator and continued losses in every quarter suggest the discount is also tied to slower growth and ongoing unprofitability rather than only mispricing. Next Steps

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for Ascend Wellness Holdings on Simply Wall St. Add the company to your watchlist or portfolio so you’ll be alerted when the story evolves.

If this mix of risks and potential rewards feels finely balanced, step in quickly, review the numbers yourself, and weigh up the 2 key rewards and 3 important warning signs.

See What Else Is Out There

Ascend Wellness Holdings is still reporting recurring losses, negative shareholders’ equity and slower revenue growth than its market comparator, which leaves a clear question mark over resilience.

If you want stocks where the balance sheet already does more of the heavy lifting, check out the solid balance sheet and fundamentals stocks screener (8 results) today and compare how they handle risk.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We’ve created the ultimate portfolio companion for stock investors, and it’s free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com