e.l.f. Beauty (NYSE:ELF) has launched a first-of-its-kind partnership with the SURVIVOR series, introducing the “e.l.f.ie Advantage” vignette series. The collaboration includes a limited-edition product drop tied to the show’s milestone live finale. This entertainment-led initiative uses creator-driven content and popular culture to reach fans beyond traditional beauty marketing.

For investors following NYSE:ELF, this move highlights how the company is using entertainment and creator content alongside its core mass-market cosmetics and skincare business. The SURVIVOR partnership follows its recent step into high-profile sports sponsorships and complements its existing portfolio of beauty products, giving the brand more touchpoints with consumers who engage heavily with media and pop culture.

Looking ahead, this kind of crossover into TV and live events may shape how you view e.l.f.’s brand strength, customer reach, and marketing spend. The key questions will be how effectively these partnerships translate into sustained engagement, and how they fit with the broader mix of channels that support the company’s overall strategy over time.

Stay updated on the most important news stories for e.l.f. Beauty by adding it to your watchlist or portfolio. Alternatively, explore our Community to discover new perspectives on e.l.f. Beauty.

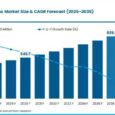

NYSE:ELF Earnings & Revenue Growth as at May 2026

NYSE:ELF Earnings & Revenue Growth as at May 2026

2 things going right for e.l.f. Beauty that this headline doesn’t cover.

Quick Assessment ✅ Price vs Analyst Target: At US$50.72, e.l.f. is about 43% below the US$88.33 analyst price target. ❌ Simply Wall St Valuation: Shares are flagged as trading about 280.8% above estimated fair value. ❌ Recent Momentum: The stock has fallen 25.9% over the past 30 days.

There is only one way to know the right time to buy, sell or hold e.l.f. Beauty. Head to Simply Wall St’s

company report for the latest analysis of e.l.f. Beauty’s fair value.

Key Considerations 📊 The SURVIVOR tie-in highlights e.l.f.’s push to deepen cultural relevance, which may matter if you care about long-term brand strength and consumer mindshare. 📊 Given the recent share price decline and current P/E of 28.8 against an industry average of 16.1, it can be useful to track how future revenue and earnings figures line up with this higher multiple. ⚠️ With the stock flagged as significantly above estimated fair value, the key risk is that sentiment around high-profile marketing spend changes faster than the fundamentals. Dig Deeper

For the full picture including more risks and rewards, check out the

complete e.l.f. Beauty analysis. Alternatively, you can visit the

community page for e.l.f. Beauty to see how other investors believe this latest news will impact the company’s narrative.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We’ve created the ultimate portfolio companion for stock investors, and it’s free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com