Find your next quality investment with Simply Wall St’s easy and powerful screener, trusted by over 7 million individual investors worldwide.

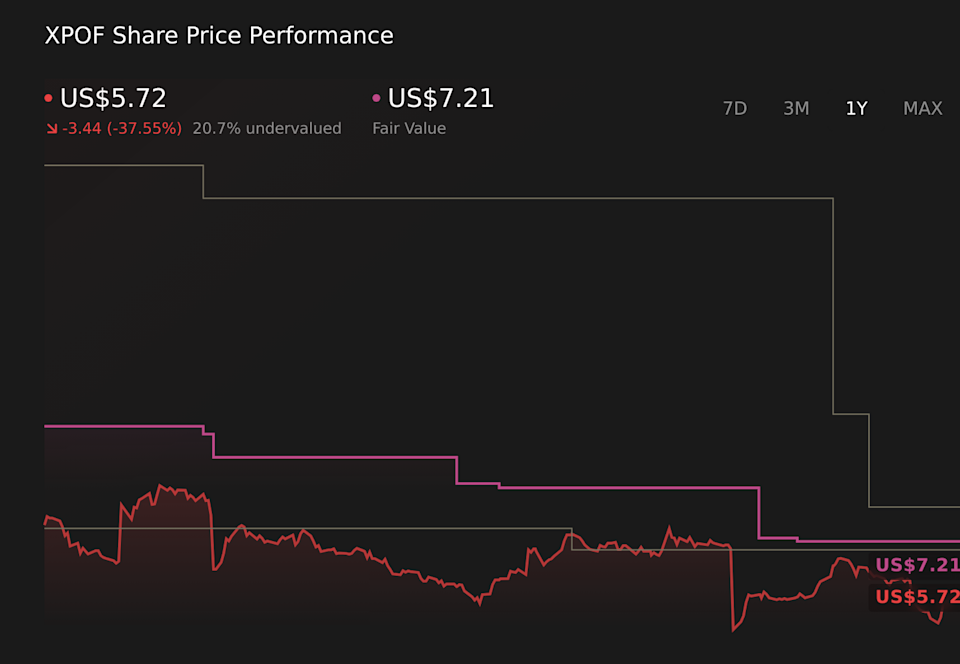

The latest update on Xponential Fitness trims the fair value estimate from US$8.39 to US$7.21, signaling a more measured view of the stock’s potential upside. That shift lines up with a split analyst debate, where some focus on corporate actions and upside from a possible transaction, while others point to execution risk, softer operating trends and slower franchise conversion. As you read on, you will see how these moving pieces shape the evolving narrative around the stock and what to watch next.

What Wall Street Has Been Saying 🐂 Bullish Takeaways

Northland upgraded Xponential Fitness to Outperform with a US$8 price target, pointing to the potential for a near term transaction after recent incentive plan changes.

Northland highlights that current executives could see immediate value realization in a change of control scenario, which the firm views as aligning management incentives with a possible deal outcome.

🐻 Bearish Takeaways

KeyBanc initiated coverage at Sector Weight with no price target, citing moderation in same store sales and slower conversion of the franchise backlog as sources of uncertainty for growth and execution.

Raymond James moved the stock to Market Perform from Strong Buy, signaling a more cautious stance on risk and reward, even as other firms focus on potential corporate actions.

Do your thoughts align with the Bull or Bear Analysts? Perhaps you think there’s more to the story. Head to the Simply Wall St Community to discover more perspectives!

NYSE:XPOF 1-Year Stock Price Chart

NYSE:XPOF 1-Year Stock Price Chart

We’ve flagged 1 risk for Xponential Fitness. See which could impact your investment.

What’s in the News

The Board of Directors began a review of multiple strategic alternatives for Xponential Fitness, including a possible sale or merger, and hired Jefferies as financial advisor to support the process.

The Federal Trade Commission reached a settlement with Xponential Fitness over alleged Franchise Rule violations, including a US$17 million monetary judgment for franchisee redress and new requirements on disclosures and marketing practices.

Riser Fitness signed the largest multi unit deal in Xponential’s history, agreeing to open 127 Club Pilates studios over five years, which would take its global footprint to more than 340 licenses.

Activist investors Voss Capital and Kanen Wealth Management urged the Board to run a formal alternatives review and appoint independent advisors and committees focused on maximizing shareholder value. The company reiterated 2026 revenue guidance of US$260.0 million to US$270.0 million, which it said is 16% lower at the midpoint than its prior reference point.

Story Continues

How This Changes the Fair Value For Xponential Fitness

Fair value trimmed from US$8.39 to US$7.21.

Projected revenue trend now shows a steeper decline, moving from a 1.52% fall to a 1.98% fall.

Net profit margin in the model moves from 10.54% to 18.25%.

Future P/E multiple adjusted from 16.88x to 10.20x.

Discount rate increased slightly from 12.33% to 12.46%.

Never Miss an Update: Follow The Narrative

Narratives link a company’s story to a financial forecast and fair value, so you can see how business decisions and industry changes flow through to the numbers. They update as new data, guidance, and risks come through.

Head over to the Simply Wall St Community and follow the Narrative on Xponential Fitness to stay up to date on:

How investment in core brands, omni channel offerings, and digital tools ties into expectations for higher unit volumes, customer retention, and margins.

What international expansion, retail partnerships such as Fit Commerce, and new marketing campaigns could mean for recurring royalties and overhead costs.

Key risk factors around slower same store sales, delayed and closed franchises, reduced brand diversification, and higher leverage that may pressure growth and financial flexibility.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include XPOF.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com