Ulta Beauty: key recent performance signals

Ulta Beauty (ULTA) has seen its share price move in different directions over shorter and longer periods, including a small 1 day decline, a weaker past week, and a gain over the past month.

See our latest analysis for Ulta Beauty.

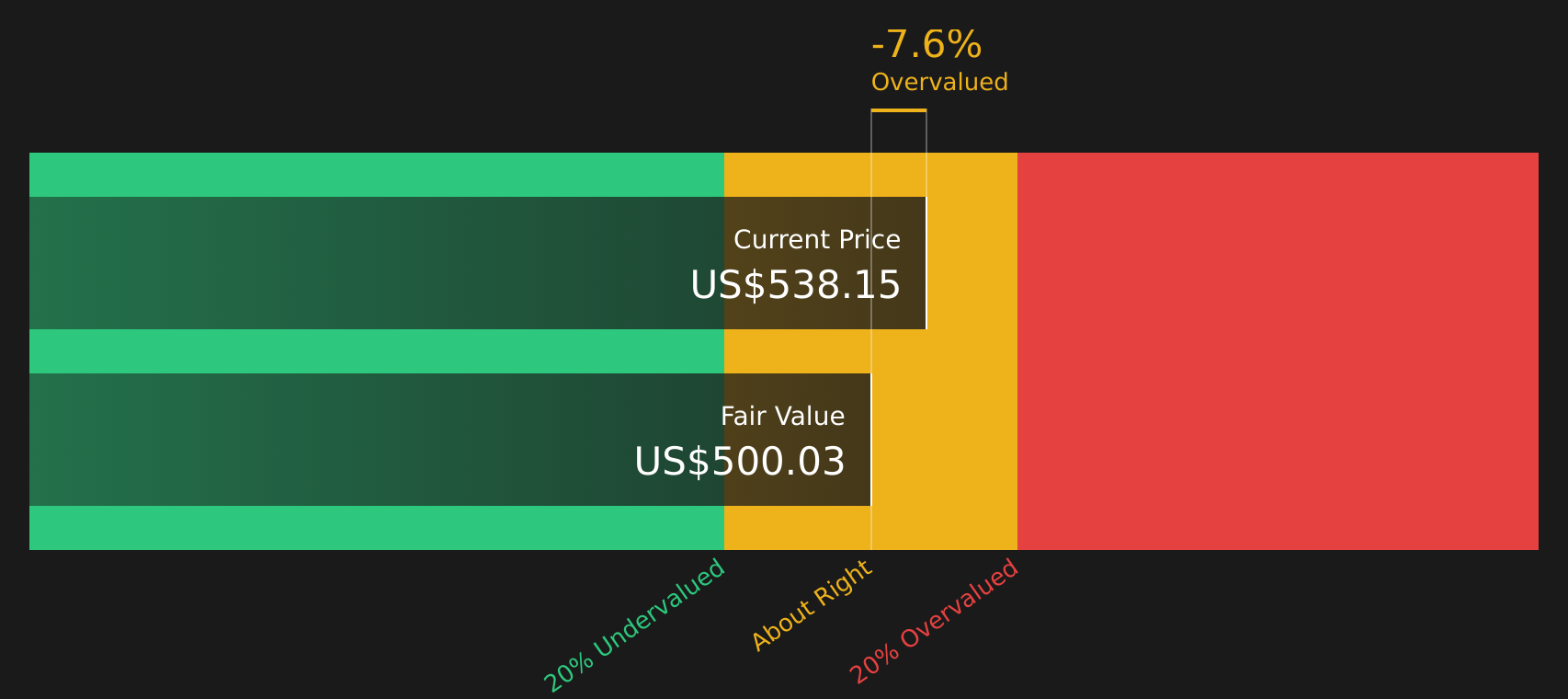

At a share price of US$538.15, Ulta Beauty has seen short term momentum cool, with a 7 day share price return of 4.57% and a 90 day share price return of 14.73%, while the 1 year total shareholder return of 36.02% points to stronger longer term gains.

If you are comparing Ulta with other retailers and consumer names, this can be a good moment to broaden your watchlist using our screener for 18 top founder-led companies

With Ulta Beauty trading at US$538.15, a value score of 3, an intrinsic value estimate suggesting a premium, and a wide gap to analyst targets, the key question is whether there is still an opportunity to invest or if the market is already pricing in future growth.

Most Popular Narrative: 25.9% Overvalued

According to a widely followed narrative for Ulta Beauty, the fair value sits at $427.41 compared with the last close at $538.15, which frames the current price as rich relative to that estimate.

Ulta, the other company I was thinking of cutting, has a surprisingly favorable relative valuation in the beauty retail space. It has decent margins and actually is able to direct decent amounts of buybacks. Beauty products in particular make a lot of sense to be sold alongside salon services in a storefront so you can actually suss out the high-end products in person. They have numerous private label brands and partnerships that attract customers, providing a small buffer to their expanding loyalty program. They are at their lowest ever P/E ratio right now at only 13, but with a high P/S and book ratio of 7, which is odd to me. They have a strong Return on Capital Employed (ROCE) and are free from debt. However, being a pure-play storefront with little room to grow aside from the untested waters of abroad leaves this company with a likely case of declining margins and earnings before only being able to grow modestly in the future. It is certainly a giant that can grow bigger, but the execution risk amid growing competition from e-commerce and other legacy storefronts in the US may take away their market share in areas that are already saturated with stores. Perceived undervaluation is mostly tangible under assumed multiple expansion, which doesn’t leave a whole lot of room for an edge.

Curious how a business with strong returns and no debt still ends up below its fair value estimate? The narrative leans heavily on future growth cooling, changing margins, and a very specific profit multiple baked into the model. The exact mix of store expansion, international ambitions, and assumed earnings power might surprise you.

Result: Fair Value of $427.41 (OVERVALUED)

Have a read of the narrative in full and understand what’s behind the forecasts.

However, a wider US$681.50 analyst target and Ulta’s expansion into Mexico could challenge the idea that the shares already reflect all the potential upside.

Find out about the key risks to this Ulta Beauty narrative.

Another way to look at Ulta’s valuation

That 25.9% premium to the US$427.41 fair value estimate paints Ulta as overvalued, but the P/E story is more nuanced. At 20.3x earnings, Ulta trades close to the US Specialty Retail average of 20.4x, yet above its own 17.1x fair ratio, which hints at some valuation stretch if the market moves toward that benchmark. With the SWS DCF model also putting fair value at US$500.03, how much comfort do you take from two methods pointing to a similar premium instead of a discount?

Look into how the SWS DCF model arrives at its fair value.

ULTA Discounted Cash Flow as at Apr 2026Next Steps

ULTA Discounted Cash Flow as at Apr 2026Next Steps

The mixed signals on valuation and growth expectations raise fair questions, so this is a good time to review the numbers yourself and decide what they really imply. To help frame that view, take a closer look at the 2 key rewards

Looking for more investment ideas?

If Ulta has sharpened your interest, do not stop here. This is the moment to widen your watchlist with other clear, data backed opportunities.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com