Target (NYSE:TGT) is expanding its wellness and fresh food assortment with new national brand partnerships, including Barker Wellness, Pure Genius, TruHeight Vitamins, Make Time Wellness, and Cypress Grove. The company is opening a $265 million Houston receive center, its first upstream supply chain facility, aimed at supporting automation and faster product distribution. These moves reflect a broader push to make health focused and specialty products more accessible across Target stores and digital channels.

Target, trading at $128.89, has seen a 28.2% gain year to date and a 38.4% return over the past year, while its 3 year and 5 year returns are negative. This mix of recent strength and longer term weakness provides context for the company as it focuses further on wellness and fresh food.

For investors tracking NYSE:TGT, the combination of expanded health oriented assortment and new supply chain capacity may influence how the business competes and serves customers. The impact of these changes on Target’s traffic, margins, and overall brand perception will be key areas to monitor over time.

Stay updated on the most important news stories for Target by adding it to your watchlist or portfolio. Alternatively, explore our Community to discover new perspectives on Target.

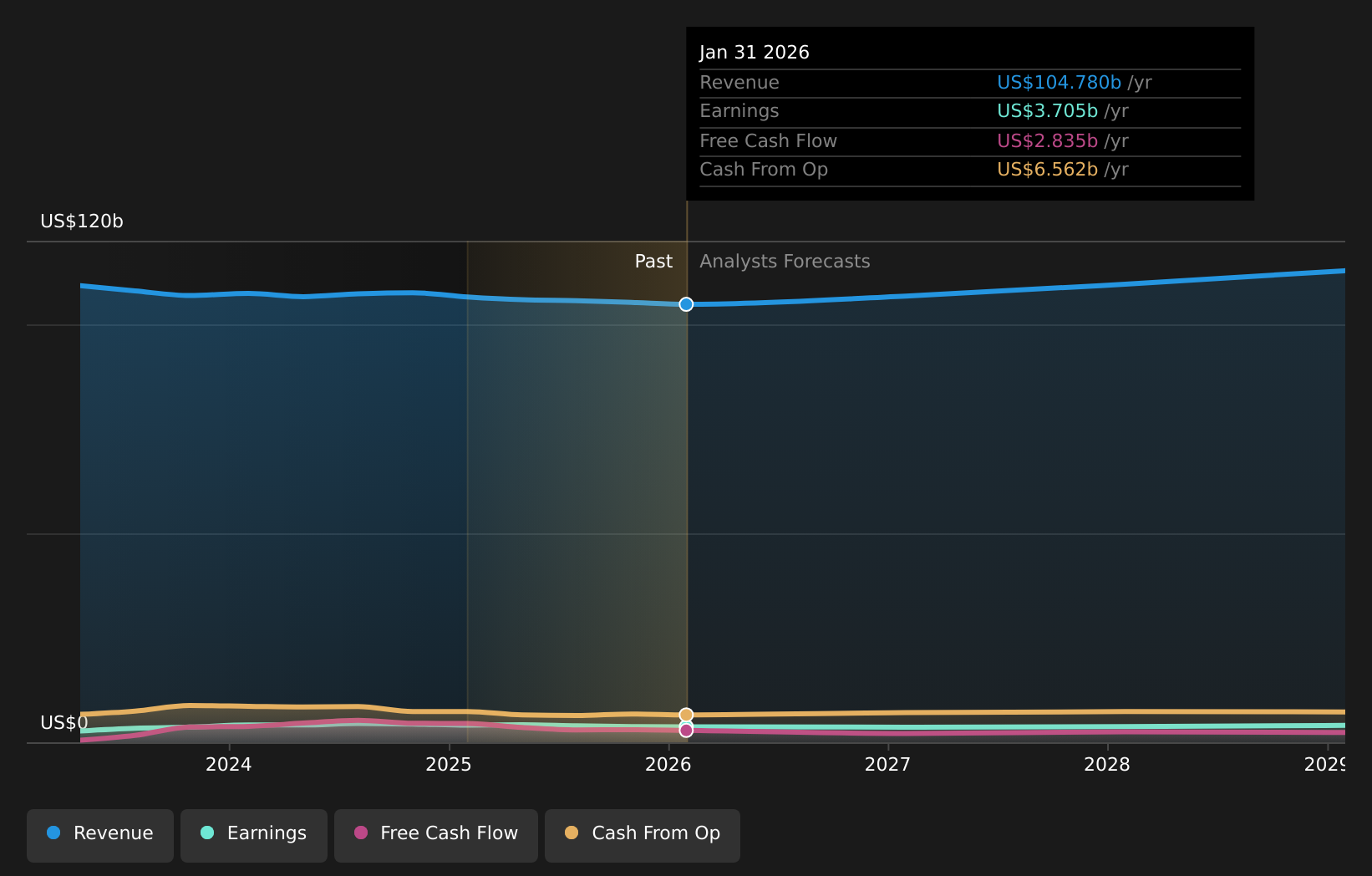

NYSE:TGT Earnings & Revenue Growth as at May 2026

NYSE:TGT Earnings & Revenue Growth as at May 2026

📰 Beyond the headline: 2 risks and 4 things going right for Target that every investor should see.

Quick Assessment ⚖️ Price vs Analyst Target: At US$128.89, Target trades about 2.7% above the US$125.53 analyst price target, within the 10% band that suggests no clear signal. ✅ Simply Wall St Valuation: Simply Wall St estimates the shares are trading 22.2% below fair value, which screens as undervalued. ✅ Recent Momentum: The 30 day return of 7.0% shows positive short term momentum as this wellness and supply chain news develops.

There is only one way to know the right time to buy, sell or hold Target. Head to Simply Wall St’s

company report for the latest analysis of Target’s fair value.

Key Considerations 📊 The wellness partnerships and Houston facility expansion tie directly into Target’s efforts to compete on health focused assortment and fresher food. 📊 Watch how these changes affect store and digital traffic, inventory speed, and whether margins hold up as the new facility and brands scale. ⚠️ With two identified minor risks including significant insider selling and a high level of debt, position sizing and balance sheet trends are important to track alongside this expansion. Dig Deeper

For the full picture including more risks and rewards, check out the

complete Target analysis. Alternatively, you can visit the

community page for Target to see how other investors believe this latest news will impact the company’s narrative.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we’re here to simplify it.

Discover if Target might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com