Recent trading pressure in Planet Fitness (PLNT), with the stock showing negative returns over the past month and past 3 months, has prompted more investors to revisit the company’s fundamentals and long term business model.

See our latest analysis for Planet Fitness.

With the share price at $65.38 and a year-to-date share price return showing a 40.42% decline, the recent 1-day and 7-day pullback extends a longer period of weak momentum. The 1-year total shareholder return of a 34.01% decline also highlights pressure on sentiment around the long-term story.

If recent weakness in Planet Fitness has you reassessing your options, this can be a good moment to broaden your watchlist and check out 17 top founder-led companies

So with Planet Fitness stock down sharply over the past year, yet trading at a discount of about 29% to one intrinsic estimate and roughly 66% below analyst targets, are you seeing a mispriced opportunity here, or a market already bracing for weaker growth?

Most Popular Narrative: 41.7% Undervalued

At a last close of $65.38 versus a narrative fair value of about $112.06, Planet Fitness is framed as significantly undervalued, with that view built on a detailed long term earnings and margin story.

Ongoing format optimization, with more strength equipment, redesigned layouts, and attention to user preference, is increasing club utilization and member satisfaction, which should improve retention and provide opportunities for pricing power, positively impacting both revenue and net margins.

Curious what kind of revenue path, margin profile, and future P/E multiple are being used to support that higher fair value? The narrative leans on specific growth forecasts, gradual profitability shifts, and a premium earnings multiple that many investors usually associate with faster growing consumer names.

Result: Fair Value of $112.06 (UNDERVALUED)

Have a read of the narrative in full and understand what’s behind the forecasts.

However, the bullish story could be tested if higher member attrition from click to cancel and tougher competition in value gyms and boutiques continues to put pressure on growth assumptions.

Find out about the key risks to this Planet Fitness narrative.

Another View on Valuation

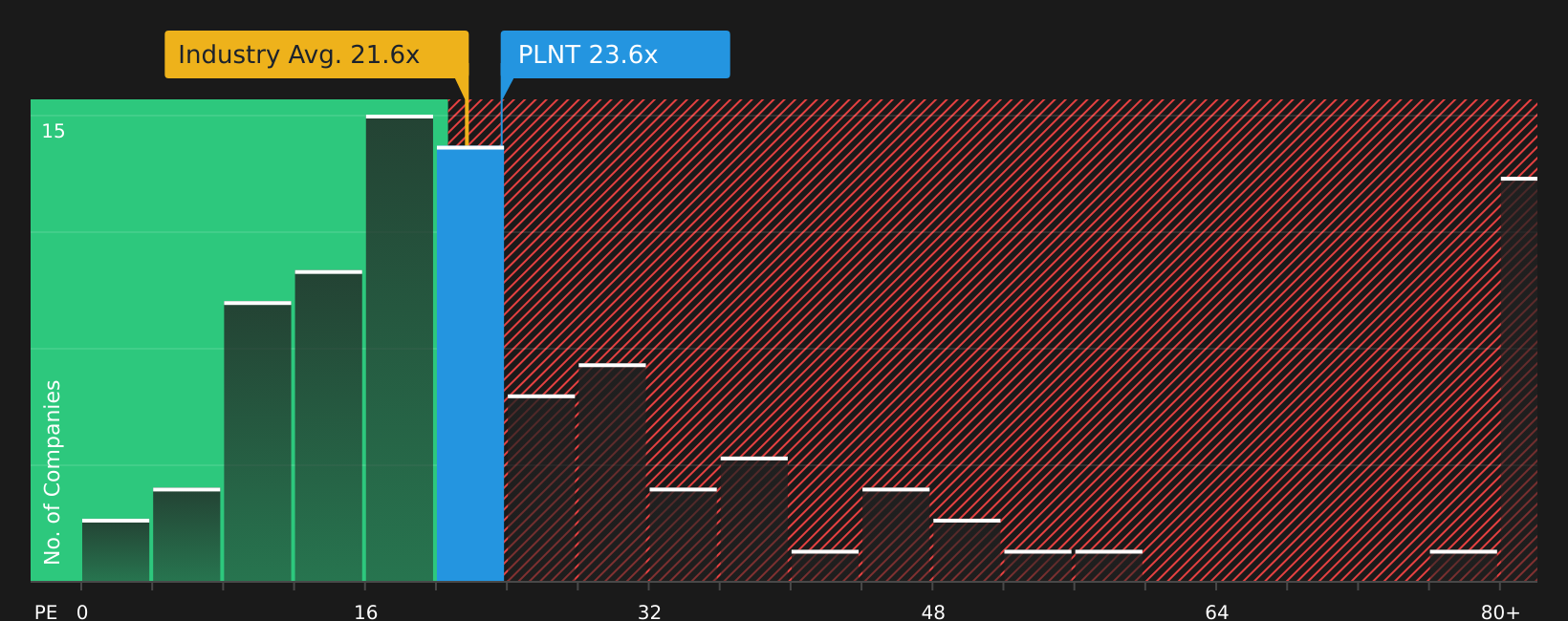

That narrative fair value of $112.06 sits alongside a more conventional check using the current P/E of 23.6x. This is slightly above both the Hospitality industry at 21.6x and the peer and fair ratio benchmarks of 23x, which hints at some valuation risk if sentiment weakens further.

So while one framework flags 41.7% undervaluation, the earnings multiple suggests the market is already paying a premium. This leaves you to decide which signal deserves more weight, or whether to wait for the two to line up.

See what the numbers say about this price — find out in our valuation breakdown.

NYSE:PLNT P/E Ratio as at May 2026Next Steps

NYSE:PLNT P/E Ratio as at May 2026Next Steps

With sentiment this mixed, it can pay to move quickly, examine the numbers yourself, and carefully weigh the 3 key rewards and 2 important warning signs

Looking for more investment ideas?

If Planet Fitness has you rethinking your next move, do not stop there. Broaden your opportunity set and let fresh ideas compete for a place in your portfolio.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We’ve created the ultimate portfolio companion for stock investors, and it’s free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com