In April 2026, Cypress Grove, Make Time Wellness and Pure Genius Protein each announced new distribution deals with Target, bringing premium goat cheeses, women’s wellness supplements and functional protein beverages into hundreds of Target stores and onto Target.com across major U.S. markets. These partnerships deepen Target’s role as a one-stop destination for specialty food and wellness products, enriching its assortment in higher-margin, trend-focused categories that can support its broader merchandising refresh. We’ll now examine how Target’s deepening focus on differentiated wellness and specialty food offerings could influence its existing investment narrative.

Uncover the next big thing with 22 elite penny stocks that balance risk and reward.

Target Investment Narrative Recap

To own Target, you need to believe it can translate merchandising refreshes, omnichannel investments, and cost efficiencies into steadier earnings despite softer discretionary demand and stiff competition. The new wellness and specialty food partnerships are incremental to that thesis; they appear helpful for margin mix and traffic, but are unlikely to shift the most important near term catalyst, which is evidence of margin improvement, or the key risk around ongoing cost and wage pressure.

Among recent developments, the push to scale Target’s retail media arm Roundel toward US$2 billion in high margin revenue feels most relevant. As Target deepens its differentiated wellness and specialty assortments, brands like Cypress Grove, Make Time Wellness, and Pure Genius Protein could become meaningful advertisers within Roundel, intertwining merchandising initiatives with higher margin digital income that supports the broader earnings recovery story.

Yet, against these positives, investors should still watch the risk that rising labor and compliance costs keep chipping away at margins and…

Read the full narrative on Target (it’s free!)

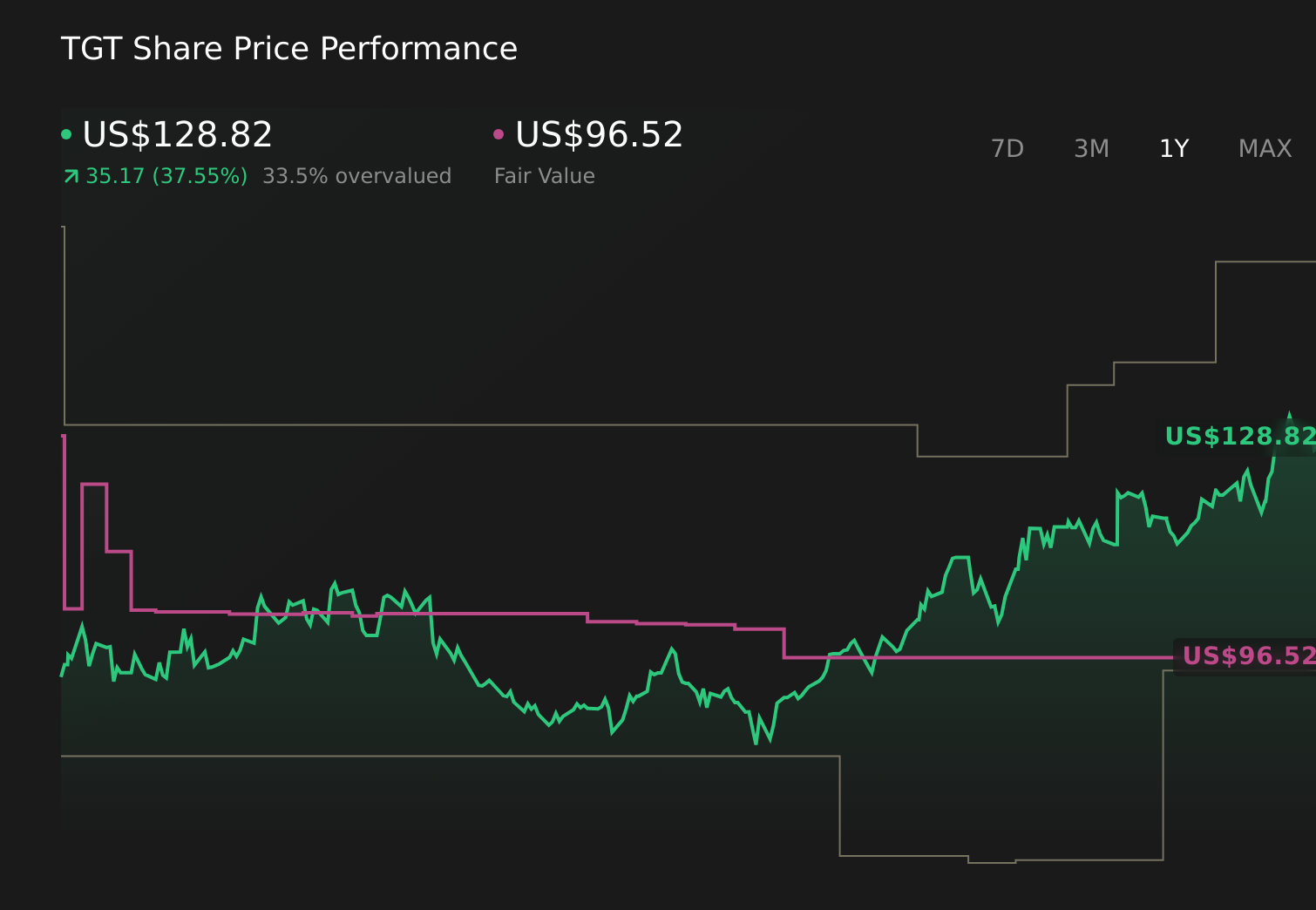

Target’s narrative projects $110.5 billion revenue and $3.7 billion earnings by 2028. This requires 1.4% yearly revenue growth and a $0.5 billion earnings decrease from $4.2 billion.

Uncover how Target’s forecasts yield a $96.52 fair value, a 25% downside to its current price.

Exploring Other Perspectives TGT 1-Year Stock Price Chart

TGT 1-Year Stock Price Chart

Some of the lowest ranked analysts paint a much harsher picture, assuming revenue grows only about 1.5 percent and earnings reach just US$3.9 billion by 2029, so you may want to compare that cautious view with how these wellness and specialty launches could eventually influence profitability and free cash flow.

Explore 18 other fair value estimates on Target – why the stock might be worth as much as 30% more than the current price!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

Seeking Other Investments?

Early movers are already taking notice. See the stocks they’re targeting before they’ve flown the coop:

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we’re here to simplify it.

Discover if Target might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com