In recent weeks, e.l.f. Beauty has faced heightened scrutiny as analysts projected a year-over-year earnings-per-share decline ahead of its now-past May 20, 2026 earnings release, even while revenue was expected to rise and the company continued expanding internationally and integrating the Rhode acquisition.

This tension between sustained top-line momentum, evolving marketing partnerships such as the International Dance League tie-up, and profit-pressure concerns has sharpened investor focus on how efficiently e.l.f. converts its growing brand reach into durable cash generation.

We’ll now examine how concerns over an anticipated earnings-per-share decline, despite continued revenue growth, may shift e.l.f. Beauty’s investment narrative.

AI is about to change healthcare. These 32 stocks are working on everything from early diagnostics to drug discovery. The best part – they are all under $10b in market cap – there’s still time to get in early.

e.l.f. Beauty Investment Narrative Recap

To own e.l.f. Beauty, you need to believe its strong brand, digital reach, and expanding global footprint can translate steady revenue growth into sustainable cash generation, even as margins come under pressure from tariffs, higher costs, and heavier marketing spend. The sharp share price pullback and concerns about an anticipated EPS decline put the near term spotlight on execution around the May 20 results, but do not fundamentally change the core debate around growth versus profitability.

Against this backdrop, the International Dance League partnership stands out because it directly connects e.l.f. to a large, young streaming audience, reinforcing its social media and content driven marketing edge. How effectively initiatives like this, alongside viral franchises such as Halo Glow and the Rhode rollout, translate into profitable growth is likely to shape whether the current earnings worries prove temporary or signal a more persistent reset in expectations.

Yet while the brand keeps gaining cultural traction, investors should also be aware of rising legal and regulatory scrutiny, especially around…

Read the full narrative on e.l.f. Beauty (it’s free!)

e.l.f. Beauty’s narrative projects $2.2 billion revenue and $204.0 million earnings by 2029. This requires 12.7% yearly revenue growth and about a $100 million earnings increase from $103.9 million today.

Uncover how e.l.f. Beauty’s forecasts yield a $103.40 fair value, a 87% upside to its current price.

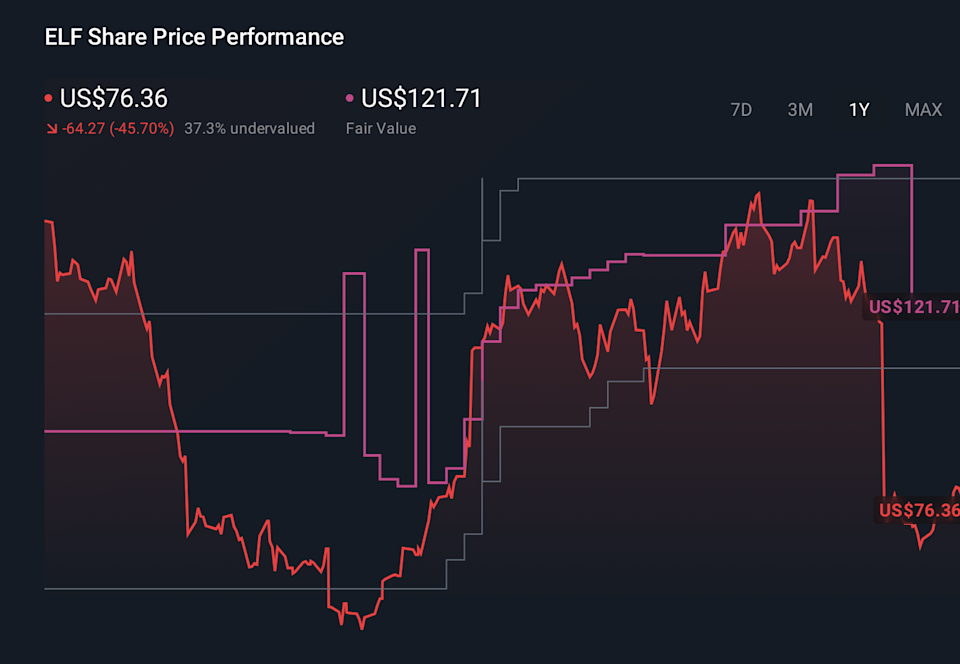

Exploring Other Perspectives  ELF 1-Year Stock Price Chart

ELF 1-Year Stock Price Chart

Some of the lowest estimate analysts were already cautious, even while assuming revenue could reach about US$2.2 billion and earnings about US$288 million by 2028, which shows just how differently you and other shareholders might weigh the recent earnings worries versus long term expansion risks.

Explore 11 other fair value estimates on e.l.f. Beauty – why the stock might be worth over 2x more than the current price!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

No Opportunity In e.l.f. Beauty?

Opportunities like this don’t last. These are today’s most promising picks. Check them out now:

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include ELF.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com